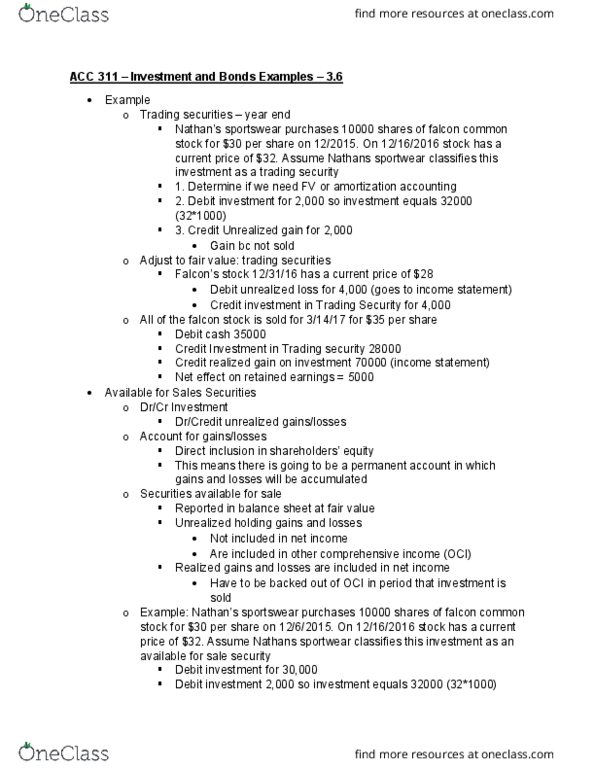

Hurricane Inc. purchased a portfolio of available-for-sale securities in 2016, its first year of operations. The cost and fair value of this portfolio on December 31, 2016, was as follows:

1

Name

Number of Shares

Total Cost

Total Fair Value

2

Tornado Inc.

830.00

$14,857.00

$16,185.00

3

Tsunami Corp.

1,230.00

31,488.00

34,809.00

4

Typhoon Corp.

2,170.00

44,268.00

43,834.00

5

Total

$90,613.00

$94,828.00

On June 12, 2017, Hurricane purchased 1,400 shares of Rogue Wave Inc. at $50 per share plus a $80 brokerage commission.

Required:

A. Provide the journal entries to record the following (refer to the Chart of Accounts for exact wording of account titles and be sure to enter the year as part of the date): 1. The adjustment of the available-for-sale security portfolio to fair value on December 31, 2016. 2. The June 12, 2017, purchase of Rogue Wave Inc. stock.

B. How are unrealized gains and losses treated differently for available-for-sale securities than for trading securities?

Chart of Accounts

CHART OF ACCOUNTS Hurricane Inc. General Ledger ASSETS 110 Cash 111 Petty Cash 120 Accounts Receivable 121 Allowance for Doubtful Accounts 131 Notes Receivable 132 Interest Receivable 141 Merchandise Inventory 145 Office Supplies 146 Store Supplies 151 Prepaid Insurance 161 Investments-Rogue Wave Inc. Stock 165 Valuation Allowance for Trading Investments 166 Valuation Allowance for Available-for-Sale Investments 181 Land 191 Store Equipment 192 Accumulated Depreciation-Store Equipment 193 Office Equipment 194 Accumulated Depreciation-Office Equipment

LIABILITIES 210 Accounts Payable 221 Notes Payable 231 Interest Payable 241 Salaries Payable 251 Sales Tax Payable

EQUITY 311 Common Stock 312 Paid-In Capital in Excess of Par-Common Stock 321 Preferred Stock 322 Paid-In Capital in Excess of Par-Preferred Stock 331 Treasury Stock 332 Paid-In Capital from Sale of Treasury Stock 340 Retained Earnings 350 Unrealized Gain (Loss) on Available-for-Sale Investments 351 Cash Dividends 352 Stock Dividends 390 Income Summary

REVENUE 410 Sales 611 Interest Revenue 612 Dividend Revenue 621 Income of Rogue Wave Inc. 631 Gain on Sale of Investments 641 Unrealized Gain on Trading Investments

EXPENSES 511 Cost of Merchandise Sold 512 Bad Debt Expense 515 Credit Card Expense 516 Cash Short and Over 520 Salaries Expense 531 Advertising Expense 532 Delivery Expense 533 Repairs Expense 534 Selling Expenses 535 Rent Expense 536 Insurance Expense 537 Office Supplies Expense 538 Store Supplies Expense 561 Depreciation Expense-Store Equipment 562 Depreciation Expense-Office Equipment 590 Miscellaneous Expense 710 Interest Expense 721 Loss of Rogue Wave Inc. 731 Loss on Sale of Investments 741 Unrealized Loss on Trading Investments

Journal

Shaded cells have feedback.

A. Provide the journal entries. Refer to the Chart of Accounts for exact wording of account titles. Be sure to enter the year as part of the date.

How does grading work?

PAGE 10

JOURNAL

Score: 33/51

DATE DESCRIPTION POST. REF. DEBIT CREDIT 1

?

?

2

?

3

?

?

4

?

Points:

6.47 / 10

Feedback

Check My Work

1. The gain or loss is the difference between the portfolio cost and its fair value. The offset account for the gain or loss entry is the valuation allowance account.

2. Increase the investment and decrease Cash for the purchase price (Shares x Per share amount) plus brokerage fee.

Final Question

Shaded cells have feedback.

B. How are unrealized gains and losses treated differently for available-for-sale securities than for trading securities?

Unrealized gains and losses for available-for-sale securities are accumulated over time and reported as a credit (positive) or debit (negative) balance in the Stockholdersâ Equity section. As a result, the changes in fair valueare not reflected on the income statement, as is the case with trading securities. Bypassing the income statement issupported on the grounds that available-for-sale securities will be held for alonger time than trading securities; thus, fluctuations in market prices havea greater opportunity to âcancel outâ over time.

Points:

5 / 5

Hurricane Inc. purchased a portfolio of available-for-sale securities in 2016, its first year of operations. The cost and fair value of this portfolio on December 31, 2016, was as follows:

| 1 | Name | Number of Shares | Total Cost | Total Fair Value |

| 2 | Tornado Inc. | 830.00 | $14,857.00 | $16,185.00 |

| 3 | Tsunami Corp. | 1,230.00 | 31,488.00 | 34,809.00 |

| 4 | Typhoon Corp. | 2,170.00 | 44,268.00 | 43,834.00 |

| 5 | Total | $90,613.00 | $94,828.00 |

On June 12, 2017, Hurricane purchased 1,400 shares of Rogue Wave Inc. at $50 per share plus a $80 brokerage commission.

Required:

| A. | Provide the journal entries to record the following (refer to the Chart of Accounts for exact wording of account titles and be sure to enter the year as part of the date):

| ||||

| B. | How are unrealized gains and losses treated differently for available-for-sale securities than for trading securities? |

Chart of Accounts

| CHART OF ACCOUNTS | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Hurricane Inc. | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| General Ledger | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

| ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Journal

Shaded cells have feedback.

A. Provide the journal entries. Refer to the Chart of Accounts for exact wording of account titles. Be sure to enter the year as part of the date.

How does grading work?

PAGE 10

JOURNAL

Score: 33/51

| DATE | DESCRIPTION | POST. REF. | DEBIT | CREDIT | |

|---|---|---|---|---|---|

| 1 | ? | ? | |||

| 2 | ? | ||||

| 3 | ? | ? | |||

| 4 | ? |

Points:

6.47 / 10

Feedback

Check My Work

1. The gain or loss is the difference between the portfolio cost and its fair value. The offset account for the gain or loss entry is the valuation allowance account.

2. Increase the investment and decrease Cash for the purchase price (Shares x Per share amount) plus brokerage fee.

Final Question

Shaded cells have feedback.

B. How are unrealized gains and losses treated differently for available-for-sale securities than for trading securities?

Unrealized gains and losses for available-for-sale securities are accumulated over time and reported as a credit (positive) or debit (negative) balance in the Stockholdersâ Equity section. As a result, the changes in fair valueare not reflected on the income statement, as is the case with trading securities. Bypassing the income statement issupported on the grounds that available-for-sale securities will be held for alonger time than trading securities; thus, fluctuations in market prices havea greater opportunity to âcancel outâ over time.

Points:

5 / 5

Related questions

Fair Value Journal Entries, Available-for-Sale Investments

Lipscomb Inc. purchased a portfolio of available-for-sale securities in 2014, its first year of operations. The cost and fair value of this portfolio on December 31, 2014, was as follows:

| Name | Number of Shares | Total Cost | Total Fair Value | ||||

| Jasper, Inc. | 1,200 | $16,080 | $17,850 | ||||

| Parker Corp. | 700 | 22,960 | 25,030 | ||||

| Smithfield Corp. | 350 | 10,850 | 10,310 | ||||

| Total | $49,890 | $53,190 | |||||

On May 10, 2015, Lipscomb purchased 500 shares of Violet Inc. stock at $31 per share plus a $130 brokerage fee.

Provide the journal entries to record the following: The adjustment of the available-for-sale security portfolio to fair value on December 31, 2014. The May 10, 2015, purchase of Violet Inc. stock.

| |||||||||||||||||||||||||||||||||||||||||||||||||||

Storm, Inc. purchased the following available-for-salesecurities during 2016, its first year of operations:

| Name | Number of Shares | Cost | |||

| Dust Devil, Inc. | 1,900 | $81,700 | |||

| Gale Co. | 850 | 68,000 | |||

| Whirlwind Co. | 2,850 | 114,000 | |||

| Total | $263,700 | ||||

The market price per share for the available-for-sale securityportfolio on December 31, 2016, was as follows:

| Market Price per Share, | ||||

| Dec. 31, 2016 | ||||

| Dust Devil, Inc. | $40 | |||

| Gale Co. | 75 | |||

| Whirlwind Co. | 42 | |||

a. Provide the journal entry to adjust theavailable-for-sale security portfolio to fair value on December 31,2016.

| 2016 Dec. 31 | Valuation Allowance forAvailable-for-Sale Investments | ||

b. Is there any impact of December 31, 2016journal entry on the income statement?

, any unrealized gain/loss is reported of the

Coronado Company has the following portfolio of investment securities at September 30, 2017, its last reporting date.

| Trading Securities | Cost | Fair Value | ||

| Horton, Inc. common (5,180 shares) | $217,560 | $204,010 | ||

| Monty, Inc. preferred (3,200 shares) | 115,200 | 121,760 | ||

| Oakwood Corp. common (930 shares) | 171,120 | 170,150 |

On October 10, 2017, the Horton shares were sold at a price of $51 per share. In addition, 3,150 shares of Patriot common stock were acquired at $53 per share on November 2, 2017. The December 31, 2017, fair values were Monty $87,420, Patriot $136,340, and the Oakwood $183,240.

Prepare the journal entries to record the sale, purchase, and adjusting entries related to the equity securities in the last quarter of 2017.