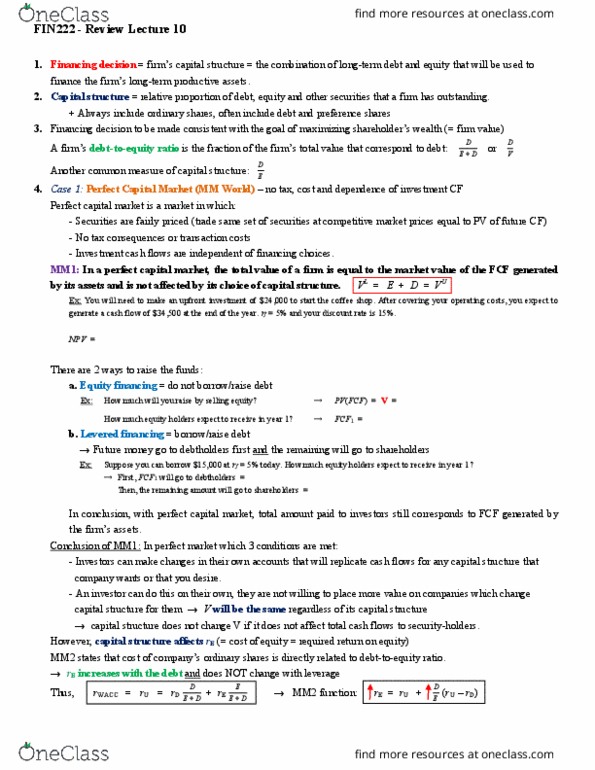

Franco Modigliani and Merton Miller (M & M) are two very famous financial economists that both won the Nobel Prize in Economics for their work in the finance area, particularly in capital structure theories (see the Description of this in the box on page 504 of your text). In their famous 1958 article (see footnote on page 490), they argued that with perfect capital markets, the total value of a firm should not depend on its capital structure. In other words, the total value of a firm would be the same with all equity, or financing with 100% debt. This is the basic MM Proposition I stated on p.493. But, as you should see, the "perfect capital markets" assumes 3 key assumptions, including no taxes or transactions costs dealing with equity or debt. Additionally, a key assumption is that individuals and firms can trade the same set of securities at competitive market prices equal to the present value of their future cash flows. These assumptions are necessary for the M&M theory on capital structure. For the Proposition M&M II beginning on page 498, still in a perfect capital market which includes no taxes, M&M state that the cost of capital of EQUITY increases with the firm's market value debt-equity ratio. But, when you examine this Proposition more closely, for a new investment the cost of capital will equal the weighted average of the firm's equity and debt costs. What does this mean in practical terms? It means that M&M "loosens" a part of the Proposition I, and admit that the cost of equity does increase as the debt-equity ratio increases. But, if you examine this closely, it means that the OVERALL cost of capital, captured in the WACC stays constant. And, the pre-tax WACC is the same as the after-tax WACC, since there is no tax! If the WACC stays constant while the equity cost increases, the figure also shows that the debt costs are also going up; similarly, if the equity costs are going down, then the debt costs are going down also as the debt-to-value decreases. This is shown on page 500 in Figure 14.1. And, of course, the weights of debt and equity (0/100, 25/75, 50/50, 75/25, 100/0) count. But, in the real-world, the M&M Propositions do not hold....corporations and individuals do have taxes, and do have transactions costs for debt and equity...buying bonds and stocks, for example. So, as we have learned, the Beta coefficient for equity does increase as the amount of debt level increases (due to increasing risks of default of interest payments or repayment of the bonds at maturity)...and the costs of debt increase, but as we weight those, the WACC actually varies, based on the real-world that includes taxes....we normally see the WACC being a U-shaped curved that varies as a function of the debt to equity ratio.

Questions:

1. Discuss the MM Proposition I and MM Proposition II (definition, assumptions, results and implications)? Remember, at the MBA level, more is better. But, to the point, and no "hot air."

2. Assume you are doing a financial analysis for Kroger Inc. Here is one of the income statements that you analyze (all figures in $ Millions):

Which year does Kroger Incorporation have the highest tax shield and why? Be very specific.

Year

2006

2005

2004

Total Sales

60,553

56,434

53,791

Cost of goods sold

45,565

42,140

39,637

Selling, general & admin expenses

11,688

12,191

11,575

Depreciation

1265

1256

1209

Operating Income

2035

847

1370

Other Income

0

0

0

EBIT

2035

847

1370

Interest expense

510

557

604

Earnings before tax

1525

290

766

Taxes (35%)

534

102

268

Net Income

991

189

498

Franco Modigliani and Merton Miller (M & M) are two very famous financial economists that both won the Nobel Prize in Economics for their work in the finance area, particularly in capital structure theories (see the Description of this in the box on page 504 of your text). In their famous 1958 article (see footnote on page 490), they argued that with perfect capital markets, the total value of a firm should not depend on its capital structure. In other words, the total value of a firm would be the same with all equity, or financing with 100% debt. This is the basic MM Proposition I stated on p.493. But, as you should see, the "perfect capital markets" assumes 3 key assumptions, including no taxes or transactions costs dealing with equity or debt. Additionally, a key assumption is that individuals and firms can trade the same set of securities at competitive market prices equal to the present value of their future cash flows. These assumptions are necessary for the M&M theory on capital structure. For the Proposition M&M II beginning on page 498, still in a perfect capital market which includes no taxes, M&M state that the cost of capital of EQUITY increases with the firm's market value debt-equity ratio. But, when you examine this Proposition more closely, for a new investment the cost of capital will equal the weighted average of the firm's equity and debt costs. What does this mean in practical terms? It means that M&M "loosens" a part of the Proposition I, and admit that the cost of equity does increase as the debt-equity ratio increases. But, if you examine this closely, it means that the OVERALL cost of capital, captured in the WACC stays constant. And, the pre-tax WACC is the same as the after-tax WACC, since there is no tax! If the WACC stays constant while the equity cost increases, the figure also shows that the debt costs are also going up; similarly, if the equity costs are going down, then the debt costs are going down also as the debt-to-value decreases. This is shown on page 500 in Figure 14.1. And, of course, the weights of debt and equity (0/100, 25/75, 50/50, 75/25, 100/0) count. But, in the real-world, the M&M Propositions do not hold....corporations and individuals do have taxes, and do have transactions costs for debt and equity...buying bonds and stocks, for example. So, as we have learned, the Beta coefficient for equity does increase as the amount of debt level increases (due to increasing risks of default of interest payments or repayment of the bonds at maturity)...and the costs of debt increase, but as we weight those, the WACC actually varies, based on the real-world that includes taxes....we normally see the WACC being a U-shaped curved that varies as a function of the debt to equity ratio.

Questions:

1. Discuss the MM Proposition I and MM Proposition II (definition, assumptions, results and implications)? Remember, at the MBA level, more is better. But, to the point, and no "hot air."

2. Assume you are doing a financial analysis for Kroger Inc. Here is one of the income statements that you analyze (all figures in $ Millions):

Which year does Kroger Incorporation have the highest tax shield and why? Be very specific.

| Year | 2006 | 2005 | 2004 |

| Total Sales | 60,553 | 56,434 | 53,791 |

| Cost of goods sold | 45,565 | 42,140 | 39,637 |

| Selling, general & admin expenses | 11,688 | 12,191 | 11,575 |

| Depreciation | 1265 | 1256 | 1209 |

| Operating Income | 2035 | 847 | 1370 |

| Other Income | 0 | 0 | 0 |

| EBIT | 2035 | 847 | 1370 |

| Interest expense | 510 | 557 | 604 |

| Earnings before tax | 1525 | 290 | 766 |

| Taxes (35%) | 534 | 102 | 268 |

| Net Income | 991 | 189 | 498 |