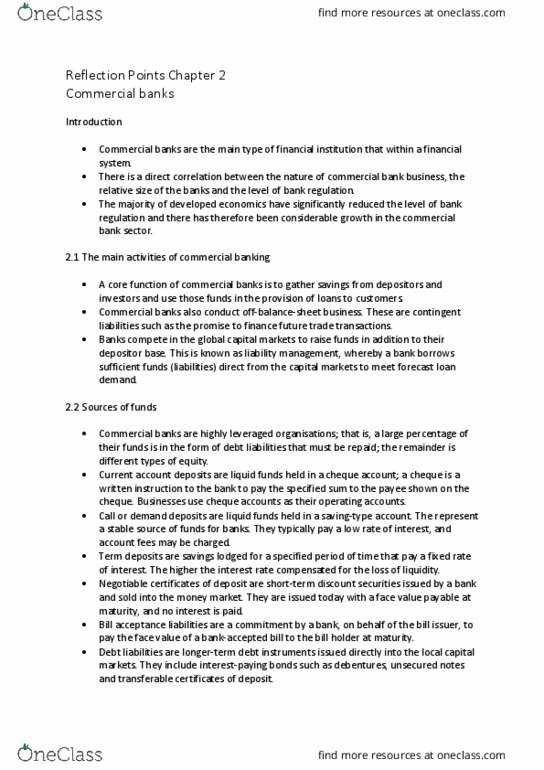

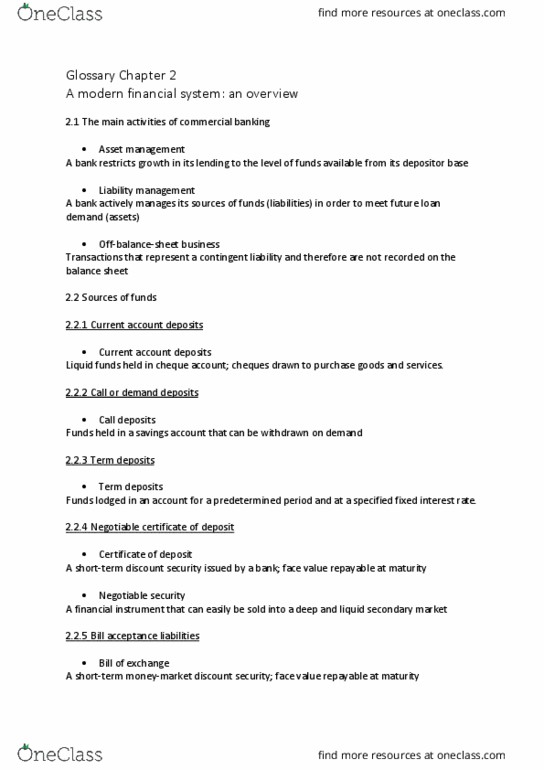

1

answer

12

watching

1,502

views

27 Feb 2018

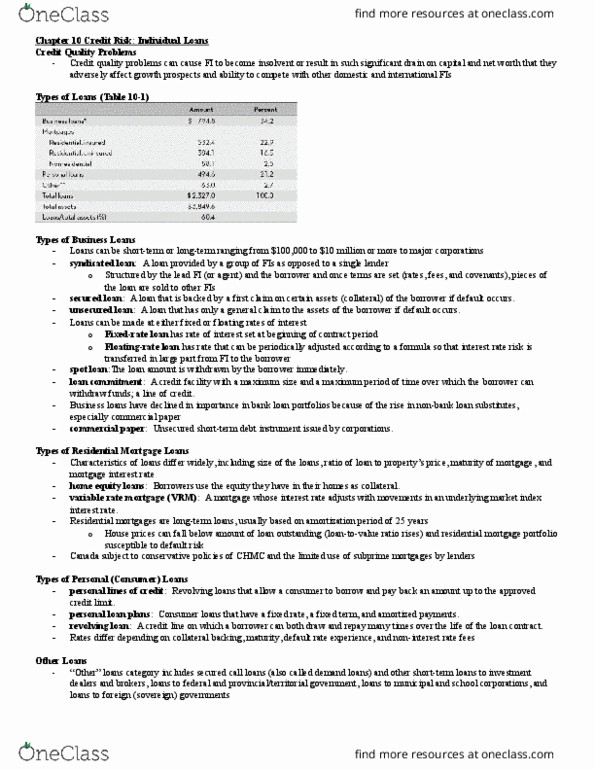

Why do you think a debt instrument whose interest rate is charged periodically based on some market interest rate would be more suitable for a depository institution than a long-term debt instrument with a fixed interest rate?

In the long run, which is more advantageous to a firm? Should a firm take a risk with the floating rate or go with the known fixed rate and why?

Why do you think a debt instrument whose interest rate is charged periodically based on some market interest rate would be more suitable for a depository institution than a long-term debt instrument with a fixed interest rate?

In the long run, which is more advantageous to a firm? Should a firm take a risk with the floating rate or go with the known fixed rate and why?

Why do you think a debt instrument whose interest rate is charged periodically based on some market interest rate would be more suitable for a depository institution than a long-term debt instrument with a fixed interest rate?

In the long run, which is more advantageous to a firm? Should a firm take a risk with the floating rate or go with the known fixed rate and why?

Why do you think a debt instrument whose interest rate is charged periodically based on some market interest rate would be more suitable for a depository institution than a long-term debt instrument with a fixed interest rate?

In the long run, which is more advantageous to a firm? Should a firm take a risk with the floating rate or go with the known fixed rate and why?

Liked by loriefabon22

Lelia LubowitzLv2

2 Mar 2018