Many Fedwatchers are convinced the central bank is just hours away from announcing the first increase to its benchmark federal-funds rate in nearly a decade. If that happens, there will be repercussions for stocks and bonds, on Main Street and Wall Street, and for economies in all corners of the world. For some, the impact could be felt right away, and for others, the shakeout may be felt more acutely over time, especially if the Fed follows the first rate hike with sustained tightening.

Hereâs a roundup from Journal staffers about who wins and who loses when rates rise.

Banks. Banks have been yearning for the Federal Reserve to start raising rates for years to stem the decline in their net interest margin, an important measure of banksâ profitability. The interest rates banks charge on many loans are directly tied to the Fedâs target rate, meaning they immediately earn more interest on those items, while deposit rates move more gradually. Goldman Sachs Group Inc. analysts recommends owning the stocks of banks whose depositors are likely to stick around: Bank of America Corp., J.P. Morgan Chase & Co., Wells Fargo & Co., PNC Financial Services Group, Inc. and E*Trade Financial Corp. âPeter Rudegeair

Corporate bonds. Corporate bonds could take a hit if the Fed raises rates, but should outperform benchmark U.S. Treasury debt, analysts say. Part of the reason is bond math: When rates rise, prices fall. But corporate bonds carry higher interest rates than Treasurys, to compensate investors for the added risk of default, so these bonds have more cushion to absorb a rate increase. After a major selloff in the market for higher-yielding junk debt in recent weeks, some analysts now expect that junk bondsâexcluding the hardest hit energy and commodity sectorsâwill perform better than investment-grade debt should the Fed make a move. âAs long as weâre selective about credits, [high-yield bonds] probably offers us a better opportunity in a rising-rate environment,â said Priscilla Hancock, global fixed income strategist at J.P. Morgan Asset Management. âWhen the Fed raises rates, itâs supposed to suggest the economy is strengthening.â âMike Cherney

Dollar. Most investors and analysts say the dollarâs nearing the end of its bull run, even if the Federal Reserve raises rates Wednesday or early in 2016. The greenbackâs risen ahead of past tightening cycles, and then sold off before interest rates reached their apex. âThe European Central Bank probably has to step up and ease policy again in 2016, and the Fed will likely have more than one interest-rate move next year; add those up and yield spreads still are generally moving in the dollarâs favor,â said Westpac Bankâs Richard Franulovich. âThe dollarâs rally is hitting its mature phase, but itâs definitely got further to run.â The dollar has already strengthened 24% against other currencies since June 2014. Many investors predict that uneven U.S. growth or volatile global markets would discourage the Fed from raising rates as rapidly as in previous tightening cycles, limiting further upside. âJames Ramage

Emerging markets. A rise in U.S. interest rates could provide a litmus test for many emerging economies and show how prepared they are to withstand the potential capital outflows triggered by higher U.S. yields and a stronger dollar. Retaining foreign capital has already been challenging for emerging countries, many of which are struggling with slowing growth and substantial debt. So far, emerging-market currencies have absorbed most of the pains, losing 18% against the dollar this year through last week. Stocks, which are priced in local currencies, were down 17%, but dollar-denominated EM bonds have fared better, still managing to hold on to single-digit gains this year. âGiven how much EM currencies have already fallen this year, we donât expect much turmoil in the near term,â if the Fed begins to tighten as expected, said Jorge Mariscal, chief investment officer of emerging markets at UBS Wealth Management, which oversees $1.9 trillion in invested assets. âWhat matters is the path of the interest rates in the U.S. going forward.â UBS expects four more rate increases next year, which will be problematic for a number of vulnerable emerging countries, including Brazil, Turkey, South Africa and Indonesia. âCarolyn Cui

Euro. Expectations for higher U.S. interest rates and easier monetary policy in the eurozone drove the euro down 22% against the dollar since May 2014. In theory, a Fed rate increase should push the euro even lower. But the common currencyâs future has been complicated by investorsâ penchant for using euros to fund trades for higher-yielding assets. Thus, the euro stands to gain whenever investors grow risk-averse and trim or exit those bets. In addition, euro-bears have proven particularly sensitive to central-bank expectations. The euro isnât likely to reach parity with the dollar anytime soon, says Mizuho Bankâs Sireen Harajli. âFundamentals would call for a weaker euro,â she says. âBut unless the ECB asks for more stimulus, it would be difficult for the euro to weaken significantly from here.â However, few investors foresee a substantial euro rally in the coming weeks, either. âJames Ramage

Gold. Prices slumped to five-year lows in recent weeks as expectations of higher rates from the Fed hit fever-pitch. Bets that benefit if gold prices fall outpaced wagers that gold will rally by a record margin of 17,949 contracts on Dec. 1, according to CFTC data. Tighter monetary policy is likely to make it harder for gold, which doesnât pay interest, to compete with yield-bearing assets like Treasury bonds. However, some market watchers say the policy shift is already reflected in low gold prices, and the market could pop higher if the Fed reiterates that subsequent rate increases will be spread out. âTatyana Shumsky

High-quality stocks. Stocks with healthy balance sheets, high returns on capital, muted volatility, elevated margins and track records of stable sales and earnings growth stand to benefit when rates are rising. Per data compiled by Goldman Sachs Group Inc., these names have a history of outperforming their lesser-quality counterparts in the three months following an initial rate rise. Companies with strong balance sheets, for instance, typically outperform those with weak ones by an average 5% three months after liftoff, according to Goldman. âKristen Scholer

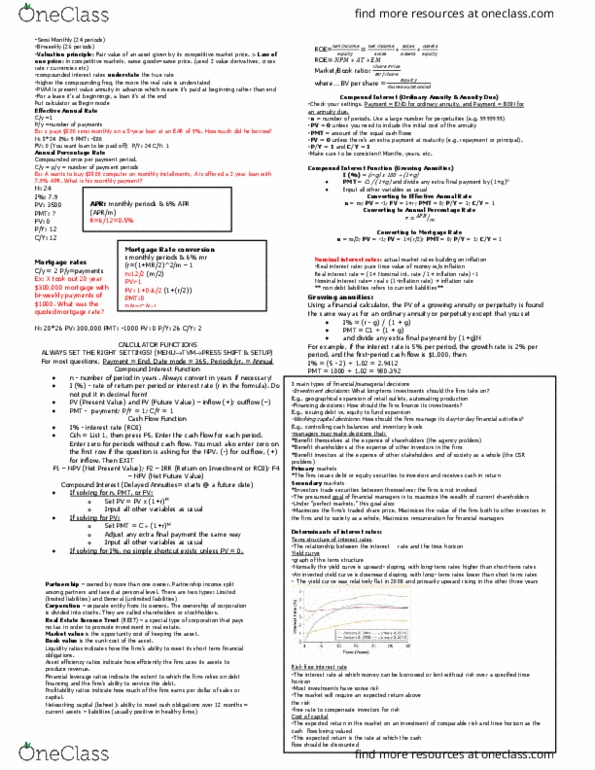

Housing market. Higher short-term interest rates wonât wreck housing, and in the near-term might have hardly any impact at all. For one, the rate of mortgages, as with those of other long-term loans, have only an indirect relationship with short-term rates and are influenced more heavily by factors such as inflation expectations and economic growth. The rate on a 30-year fixed-rate mortgageâwhich last week was at 3.95% according to Freddie Macâalmost surely is already pricing in expectations of a Fed move on Wednesday. That said, over the next year, some economists expect mortgage rates to rise about half a percentage point. All else being equal, that would hurt home prices as borrowers would need to buy a cheaper house to keep the same monthly payment. A recent poll of home buyers by real-estate broker Redfin Corp. said that higher mortgage rates would have the biggest impact on the lower-end of the housing market. âJoe Light

Life insurers. Few companies are rooting for a sustained rise in interest rates as loudly as U.S. insurers are, and life insurers are leading the cheers. Most insurers earn substantial income from investing premiums, and they typically favor high-quality bonds, whose yields have plummeted in recent years amid the sustained low interest-rate environment. Life insurers depend more heavily on investment income than do car, home and some sorts of business insurers. Thatâs because life insurers can collect premiums for decades before paying out a claim, and rely on that investment income to make a policy profitable. For many older policies on life insurersâ books, the companies expected to earn far-higher yields than newly invested cash fetches today. MetLife Inc. Chief Executive Steve Kandarian argues that life-insurance buyers will benefit too, as low rates make the cost of the coverage âmuch more expensive than it needs to be.â Low rates also raise the cost of running risk-management programs. Such hedging programs are important for those life insurers selling certain types of income-stream guarantees. âLeslie Scism

Money-market funds. The Fedâs 0.25% interest-rate increase will begin showing up in the yields of money-market mutual funds within days, welcome news for investors. Funds for individual investors that invest in both corporate and government debt currently yield just 0.01% on average, according to researcher iMoneyNet Inc. The higher rates should be fully reflected in just over a month, but investors in some money funds may not see the full increase, says Peter Crane, president of Crane Data LLC. Fund managers have temporarily trimmed fees to keep expenses from eating up the fundsâ paltry yields and taking a bite out of investorsâ principal. As interest rates rise, some part of the increase is likely to go toward increasing fundsâ fee charges, Mr. Crane says. Across the industry, âmy wild guess is that half of the first rate hike might flow through to investors, but it could be more,â he says. âDaisy Maxey

Oil. The latest plunge in oil prices has pummeled the stock and bond prices of some U.S. energy producers and raised fears of a spate of defaults across the sector. Increased interest rates could hurt producers that are already struggling to pay debts amid sharply lower cash flow. That could be positive for oil prices in the long run, if U.S. producers are forced out of business and domestic production declines as a result, reducing the global glut of crude. But in the near-term, the most direct effect on oil prices would probably come from the dollar. If the dollar still has room to run in the wake of a rate hike, the rising dollar could weigh on oil prices by making dollar-traded oil more expensive for buyers using foreign currencies. âNicole Friedman

Rate-sensitive stocks. Companies considered rate-sensitive are those that have high dividend yields. Consumer staples, telecoms and utilities fall into this category, as all three sectors yield more than the S&P 500. They have been attractive investments amid the low-yield environment the past several years. But, as rates rise, bonds are poised to become more attractive than their current state, which could steal some of the thunder away from high-dividend yielding shares. âKristen Scholer

Stocks with a large portion of floating-rate debt. Firms that have a decent amount of variable debtâwhere interest payments adjust as market rates rise or fallâstand to take a hit. As rates rise, so too will the cost of floating-rate debt. âWhen the tightening cycle finally starts, the immediate impact will be felt by firms with high proportions of variable rate borrowing,â wrote Goldman. Among the 10 S&P 500 sectors, financials and industrials have the greatest portion of floating-rate debt with it accounting for 16% and 10%, respectively, of all debt for those sectors. âKristen Scholer

Treasurys. The Fedâs policy has a more direct impact on short-term government debt whose yields are highly sensitive to changes in the fed-fund rate. The yield on the two-year note recently traded near 1%, headed for the highest closing since May 2010. Many investors expect the yield to rise if the Fed raises interest rates on Wednesday. But some argue the yield has nearly doubled in the past two months and if the Fed signals that further tightening will happen at a very slow pace, some may book profit from their short bets on the two-year notes.

The Fedâs impact on long-term bonds is more subdued. The value of those bonds are influenced by a broad basket of factors, including the global growth and inflation outlook. A rate increase by the Fed may drive some investors to sell long-term bonds. But given concerns about the global economic outlook, there likely plenty of investors who could seek safety in long-term Treasury debt, especially with many focusing on the recent stress from the junk debt market. Any signal of a slow tightening path would keep a lid on long-term bond yields.

One way an interest-rate increase could weigh on the U.S. government debt market is by making newly-minted bonds more attractive to buy, thus dragging down the value of outstanding bonds. âMin Zeng

In the discussion of "housing market," if we keep the same monthly payment (note: these are future cash outflows), will mortgage borrowers be able to buy a cheaper or more expansive house with the rate hike (note: the mortgage loan the borrower takes out to buy the house is the present value)? Explain briefly please.

Many Fedwatchers are convinced the central bank is just hours away from announcing the first increase to its benchmark federal-funds rate in nearly a decade. If that happens, there will be repercussions for stocks and bonds, on Main Street and Wall Street, and for economies in all corners of the world. For some, the impact could be felt right away, and for others, the shakeout may be felt more acutely over time, especially if the Fed follows the first rate hike with sustained tightening.

Hereâs a roundup from Journal staffers about who wins and who loses when rates rise.

Banks. Banks have been yearning for the Federal Reserve to start raising rates for years to stem the decline in their net interest margin, an important measure of banksâ profitability. The interest rates banks charge on many loans are directly tied to the Fedâs target rate, meaning they immediately earn more interest on those items, while deposit rates move more gradually. Goldman Sachs Group Inc. analysts recommends owning the stocks of banks whose depositors are likely to stick around: Bank of America Corp., J.P. Morgan Chase & Co., Wells Fargo & Co., PNC Financial Services Group, Inc. and E*Trade Financial Corp. âPeter Rudegeair

Corporate bonds. Corporate bonds could take a hit if the Fed raises rates, but should outperform benchmark U.S. Treasury debt, analysts say. Part of the reason is bond math: When rates rise, prices fall. But corporate bonds carry higher interest rates than Treasurys, to compensate investors for the added risk of default, so these bonds have more cushion to absorb a rate increase. After a major selloff in the market for higher-yielding junk debt in recent weeks, some analysts now expect that junk bondsâexcluding the hardest hit energy and commodity sectorsâwill perform better than investment-grade debt should the Fed make a move. âAs long as weâre selective about credits, [high-yield bonds] probably offers us a better opportunity in a rising-rate environment,â said Priscilla Hancock, global fixed income strategist at J.P. Morgan Asset Management. âWhen the Fed raises rates, itâs supposed to suggest the economy is strengthening.â âMike Cherney

Dollar. Most investors and analysts say the dollarâs nearing the end of its bull run, even if the Federal Reserve raises rates Wednesday or early in 2016. The greenbackâs risen ahead of past tightening cycles, and then sold off before interest rates reached their apex. âThe European Central Bank probably has to step up and ease policy again in 2016, and the Fed will likely have more than one interest-rate move next year; add those up and yield spreads still are generally moving in the dollarâs favor,â said Westpac Bankâs Richard Franulovich. âThe dollarâs rally is hitting its mature phase, but itâs definitely got further to run.â The dollar has already strengthened 24% against other currencies since June 2014. Many investors predict that uneven U.S. growth or volatile global markets would discourage the Fed from raising rates as rapidly as in previous tightening cycles, limiting further upside. âJames Ramage

Emerging markets. A rise in U.S. interest rates could provide a litmus test for many emerging economies and show how prepared they are to withstand the potential capital outflows triggered by higher U.S. yields and a stronger dollar. Retaining foreign capital has already been challenging for emerging countries, many of which are struggling with slowing growth and substantial debt. So far, emerging-market currencies have absorbed most of the pains, losing 18% against the dollar this year through last week. Stocks, which are priced in local currencies, were down 17%, but dollar-denominated EM bonds have fared better, still managing to hold on to single-digit gains this year. âGiven how much EM currencies have already fallen this year, we donât expect much turmoil in the near term,â if the Fed begins to tighten as expected, said Jorge Mariscal, chief investment officer of emerging markets at UBS Wealth Management, which oversees $1.9 trillion in invested assets. âWhat matters is the path of the interest rates in the U.S. going forward.â UBS expects four more rate increases next year, which will be problematic for a number of vulnerable emerging countries, including Brazil, Turkey, South Africa and Indonesia. âCarolyn Cui

Euro. Expectations for higher U.S. interest rates and easier monetary policy in the eurozone drove the euro down 22% against the dollar since May 2014. In theory, a Fed rate increase should push the euro even lower. But the common currencyâs future has been complicated by investorsâ penchant for using euros to fund trades for higher-yielding assets. Thus, the euro stands to gain whenever investors grow risk-averse and trim or exit those bets. In addition, euro-bears have proven particularly sensitive to central-bank expectations. The euro isnât likely to reach parity with the dollar anytime soon, says Mizuho Bankâs Sireen Harajli. âFundamentals would call for a weaker euro,â she says. âBut unless the ECB asks for more stimulus, it would be difficult for the euro to weaken significantly from here.â However, few investors foresee a substantial euro rally in the coming weeks, either. âJames Ramage

Gold. Prices slumped to five-year lows in recent weeks as expectations of higher rates from the Fed hit fever-pitch. Bets that benefit if gold prices fall outpaced wagers that gold will rally by a record margin of 17,949 contracts on Dec. 1, according to CFTC data. Tighter monetary policy is likely to make it harder for gold, which doesnât pay interest, to compete with yield-bearing assets like Treasury bonds. However, some market watchers say the policy shift is already reflected in low gold prices, and the market could pop higher if the Fed reiterates that subsequent rate increases will be spread out. âTatyana Shumsky

High-quality stocks. Stocks with healthy balance sheets, high returns on capital, muted volatility, elevated margins and track records of stable sales and earnings growth stand to benefit when rates are rising. Per data compiled by Goldman Sachs Group Inc., these names have a history of outperforming their lesser-quality counterparts in the three months following an initial rate rise. Companies with strong balance sheets, for instance, typically outperform those with weak ones by an average 5% three months after liftoff, according to Goldman. âKristen Scholer

Housing market. Higher short-term interest rates wonât wreck housing, and in the near-term might have hardly any impact at all. For one, the rate of mortgages, as with those of other long-term loans, have only an indirect relationship with short-term rates and are influenced more heavily by factors such as inflation expectations and economic growth. The rate on a 30-year fixed-rate mortgageâwhich last week was at 3.95% according to Freddie Macâalmost surely is already pricing in expectations of a Fed move on Wednesday. That said, over the next year, some economists expect mortgage rates to rise about half a percentage point. All else being equal, that would hurt home prices as borrowers would need to buy a cheaper house to keep the same monthly payment. A recent poll of home buyers by real-estate broker Redfin Corp. said that higher mortgage rates would have the biggest impact on the lower-end of the housing market. âJoe Light

Life insurers. Few companies are rooting for a sustained rise in interest rates as loudly as U.S. insurers are, and life insurers are leading the cheers. Most insurers earn substantial income from investing premiums, and they typically favor high-quality bonds, whose yields have plummeted in recent years amid the sustained low interest-rate environment. Life insurers depend more heavily on investment income than do car, home and some sorts of business insurers. Thatâs because life insurers can collect premiums for decades before paying out a claim, and rely on that investment income to make a policy profitable. For many older policies on life insurersâ books, the companies expected to earn far-higher yields than newly invested cash fetches today. MetLife Inc. Chief Executive Steve Kandarian argues that life-insurance buyers will benefit too, as low rates make the cost of the coverage âmuch more expensive than it needs to be.â Low rates also raise the cost of running risk-management programs. Such hedging programs are important for those life insurers selling certain types of income-stream guarantees. âLeslie Scism

Money-market funds. The Fedâs 0.25% interest-rate increase will begin showing up in the yields of money-market mutual funds within days, welcome news for investors. Funds for individual investors that invest in both corporate and government debt currently yield just 0.01% on average, according to researcher iMoneyNet Inc. The higher rates should be fully reflected in just over a month, but investors in some money funds may not see the full increase, says Peter Crane, president of Crane Data LLC. Fund managers have temporarily trimmed fees to keep expenses from eating up the fundsâ paltry yields and taking a bite out of investorsâ principal. As interest rates rise, some part of the increase is likely to go toward increasing fundsâ fee charges, Mr. Crane says. Across the industry, âmy wild guess is that half of the first rate hike might flow through to investors, but it could be more,â he says. âDaisy Maxey

Oil. The latest plunge in oil prices has pummeled the stock and bond prices of some U.S. energy producers and raised fears of a spate of defaults across the sector. Increased interest rates could hurt producers that are already struggling to pay debts amid sharply lower cash flow. That could be positive for oil prices in the long run, if U.S. producers are forced out of business and domestic production declines as a result, reducing the global glut of crude. But in the near-term, the most direct effect on oil prices would probably come from the dollar. If the dollar still has room to run in the wake of a rate hike, the rising dollar could weigh on oil prices by making dollar-traded oil more expensive for buyers using foreign currencies. âNicole Friedman

Rate-sensitive stocks. Companies considered rate-sensitive are those that have high dividend yields. Consumer staples, telecoms and utilities fall into this category, as all three sectors yield more than the S&P 500. They have been attractive investments amid the low-yield environment the past several years. But, as rates rise, bonds are poised to become more attractive than their current state, which could steal some of the thunder away from high-dividend yielding shares. âKristen Scholer

Stocks with a large portion of floating-rate debt. Firms that have a decent amount of variable debtâwhere interest payments adjust as market rates rise or fallâstand to take a hit. As rates rise, so too will the cost of floating-rate debt. âWhen the tightening cycle finally starts, the immediate impact will be felt by firms with high proportions of variable rate borrowing,â wrote Goldman. Among the 10 S&P 500 sectors, financials and industrials have the greatest portion of floating-rate debt with it accounting for 16% and 10%, respectively, of all debt for those sectors. âKristen Scholer

Treasurys. The Fedâs policy has a more direct impact on short-term government debt whose yields are highly sensitive to changes in the fed-fund rate. The yield on the two-year note recently traded near 1%, headed for the highest closing since May 2010. Many investors expect the yield to rise if the Fed raises interest rates on Wednesday. But some argue the yield has nearly doubled in the past two months and if the Fed signals that further tightening will happen at a very slow pace, some may book profit from their short bets on the two-year notes.

The Fedâs impact on long-term bonds is more subdued. The value of those bonds are influenced by a broad basket of factors, including the global growth and inflation outlook. A rate increase by the Fed may drive some investors to sell long-term bonds. But given concerns about the global economic outlook, there likely plenty of investors who could seek safety in long-term Treasury debt, especially with many focusing on the recent stress from the junk debt market. Any signal of a slow tightening path would keep a lid on long-term bond yields.

One way an interest-rate increase could weigh on the U.S. government debt market is by making newly-minted bonds more attractive to buy, thus dragging down the value of outstanding bonds. âMin Zeng

In the discussion of "housing market," if we keep the same monthly payment (note: these are future cash outflows), will mortgage borrowers be able to buy a cheaper or more expansive house with the rate hike (note: the mortgage loan the borrower takes out to buy the house is the present value)? Explain briefly please.