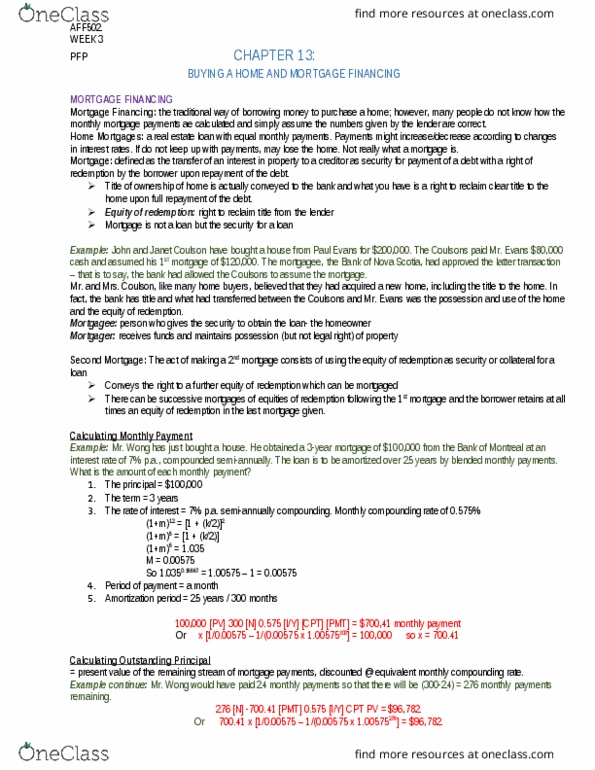

1

answer

0

watching

1,420

views

16 Jun 2018

Five years ago you took out a 5/1 adjustable rate mortgage and the five-year fixed rate period has just expired. The loan was originally for $300,000 with 360 payments at 4.2% APR, compounded monthly.

a. Now that you have made 60 payments, what is the remaining balance on the loan?

b. If the interest rate increases by 1%, to 5.2% APR, compounded monthly, what will your new payments be?

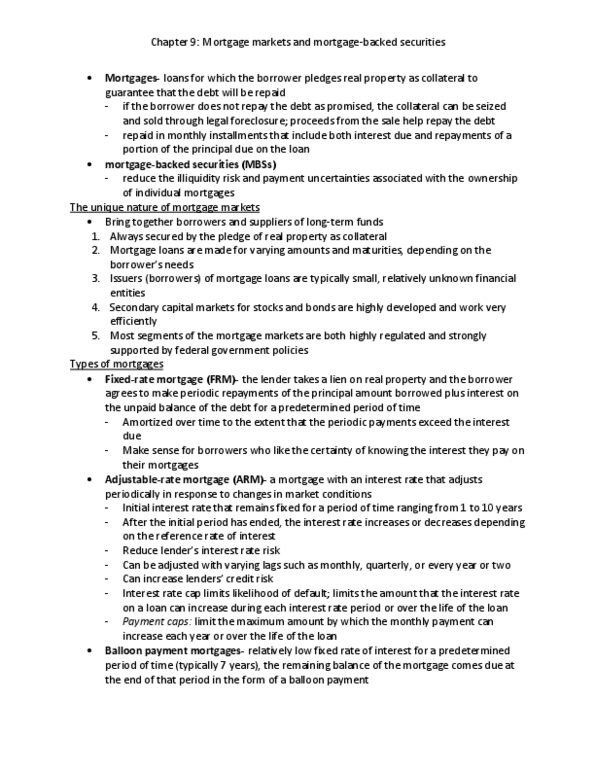

Five years ago you took out a 5/1 adjustable rate mortgage and the five-year fixed rate period has just expired. The loan was originally for $300,000 with 360 payments at 4.2% APR, compounded monthly.

a. Now that you have made 60 payments, what is the remaining balance on the loan?

b. If the interest rate increases by 1%, to 5.2% APR, compounded monthly, what will your new payments be?

Keith LeannonLv2

16 Jun 2018