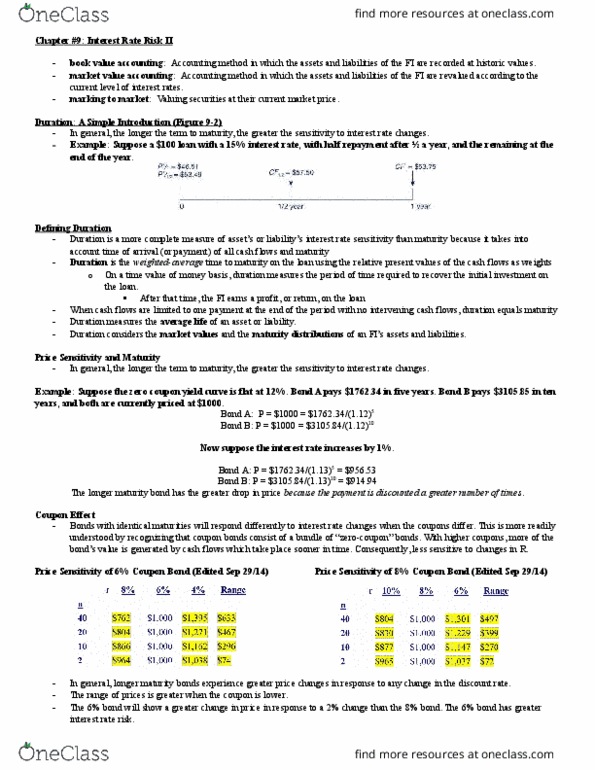

You will be paying $10,300 a year in tuition expenses at the end of the next two years. Bonds currently yield 8%.

a. What is the present value and duration of your obligation? (Do not round intermediate calculations. Round "Present value" to 2 decimal places and "Duration" to 4 decimal places.)

Present value $ Duration years

b. What is the duration of a zero-coupon bond that would immunize your obligation and its future redemption value? (Do not round intermediate calculations. Round "Duration" to 4 decimal places and "Future redemption value" to 2 decimal places.)

Duration years Future redemption value $

You buy a zero-coupon bond with value and duration equal to your obligation.

c-1. Now suppose that rates immediately increase to 9%. What happens to your net position, that is, to the difference between the value of the bond and that of your tuition obligation? (Do not round intermediate calculations. Round your answer to 2 decimal places.)

Net position changes by $

c-2. What if rates fall to 7%? (Do not round intermediate calculations. Round your answer to 2 decimal places.)

Net position changes by $

| You will be paying $10,300 a year in tuition expenses at the end of the next two years. Bonds currently yield 8%. |

| a. | What is the present value and duration of your obligation? (Do not round intermediate calculations. Round "Present value" to 2 decimal places and "Duration" to 4 decimal places.) |

| Present value | $ |

| Duration | years |

| b. | What is the duration of a zero-coupon bond that would immunize your obligation and its future redemption value? (Do not round intermediate calculations. Round "Duration" to 4 decimal places and "Future redemption value" to 2 decimal places.) |

| Duration | years |

| Future redemption value | $ |

| You buy a zero-coupon bond with value and duration equal to your obligation. |

| c-1. | Now suppose that rates immediately increase to 9%. What happens to your net position, that is, to the difference between the value of the bond and that of your tuition obligation? (Do not round intermediate calculations. Round your answer to 2 decimal places.) |

| Net position changes by | $ |

| c-2. | What if rates fall to 7%? (Do not round intermediate calculations. Round your answer to 2 decimal places.) |

| Net position changes by | $ |

Related questions

You will be paying $11,500 a year in tuition expenses at the end of the next 2 years. Bonds currently yield 10%.

| a. | What is the present value and duration of your obligation? (Do not round intermediate calculations. Round "Present value" to 2 decimal places and "Duration" to 4 decimal places. Omit the "$" sign in your response.) |

| Present value | $ |

| Duration | years |

| b. | What maturity zero-coupon bond would immunize your obligation? (Do not round intermediate calculations. Round "Duration" to 4 decimal places and "Face value" to 2 decimal places.Omit the "$" sign in your response.) |

| Duration | years |

| Face value | $ |

| Suppose you buy a zero-coupon bond with value and duration equal to your obligation. |

| c-1. | Now suppose that rates immediately increase to 12%. What happens to your net position, that is, to the difference between the value of the bond and that of your tuition obligation? (Do not round intermediate calculations. Input the amount as a positive value. Round your answer to 2 decimal places. Omit the "$" sign in your response.) |

| Net position (Click to select)increasesdecreases in value by | $ |

| c-2. | Now suppose that rates immediately falls to 8%. What happens to your net position, that is, to the difference between the value of the bond and that of your tuition obligation? (Do not round intermediate calculations. Input the amount as a positive value. Round your answer to 2 decimal places. Omit the "$" sign in your response.) |

| Net position (Click to select)increasesdecreases in value by | $ |

| You will be paying $10,400 a year in tuition expenses at the end of the next 2 years. Bonds currently yield 6%. |

| a. | What is the present value and duration of your obligation? (Do not round intermediate calculations. Round "Present value" to 2 decimal places and "Duration" to 4 decimal places. Omit the "$" sign in your response.) |

| Present value | $ |

| Duration | years |

| b. | What maturity zero-coupon bond would immunize your obligation? (Do not round intermediate calculations. Round "Duration" to 4 decimal places and "Face value" to 2 decimal places.Omit the "$" sign in your response.) |

| Duration | years |

| Face value | $ |

| Suppose you buy a zero-coupon bond with value and duration equal to your obligation. |

| c-1. | Now suppose that rates immediately increase to 7%. What happens to your net position, that is, to the difference between the value of the bond and that of your tuition obligation? (Do not round intermediate calculations. Input the amount as a positive value. Round your answer to 2 decimal places. Omit the "$" sign in your response.) |

| Net position (Click to select)decreasesincreases in value by | $ |

| c-2. | Now suppose that rates immediately falls to 5%. What happens to your net position, that is, to the difference between the value of the bond and that of your tuition obligation? (Do not round intermediate calculations. Input the amount as a positive value. Round your answer to 2 decimal places. Omit the "$" sign in your response.) |

| Net position (Click to select)increasesdecreases in value by | $ |

A 30-year maturity bond making annual coupon payments with a coupon rate of 14.5% has duration of 11.32 years and convexity of 185.2. The bond currently sells at a yield to maturity of 8%.

a. Find the exact price of the bond if its yield to maturity falls to 7%. (Do not round intermediate calculations. Round your answer to 2 decimal places.)

Price of the bond $ _________

b. Assume that you need to make a quick approximation using the duration rule (instead of the exact calculation in part a above). What price would be predicted by the duration rule? (Do not round intermediate calculations. Round your answer to 2 decimal places.)

Predicted price $ _________

c. Assume that you need to make a quick approximation using the duration-with-convexity rule (instead of the exact calculation in part a above). What price would be predicted by the duration-with-convexity rule? (Do not round intermediate calculations. Round your answer to 2 decimal places.)

Predicted price $ _________

d-1. What is the percent error for each rule? [Hint: percent error is the deviation from the exact price, divided by the exact price. It indicates the extent to which the approximated price differs from the exact price. A smaller percent error indicates more precise approximation.] (Enter your answer as a positive value. Do not round intermediate calculations. Round "Duration Rule" to 2 decimal places and "Duration-with-Convexity Rule" to 3 decimal places.)

| Percent Error | ||

| YTM | Duration Rule | Duration-With-Convexity Rule |

| 7% | ________% | ________% |

e-1. Find the exact price of the bond if it's yield to maturity rises to 9%. (Do not round intermediate calculations. Round your answer to 2 decimal places.)

Price of the bond $ _________

e-2. What price would be predicted by the duration rule? (Do not round intermediate calculations. Round your answer to 2 decimal places.)

Predicted price $ _________

e-3. What price would be predicted by the duration-with-convexity rule? (Do not round intermediate calculations. Round your answer to 2 decimal places.)

Predicted price $ _________

e-4. What is the percent error for each rule? (Do not round intermediate calculations. Round "Duration Rule" to 2 decimal places and "Duration-with-Convexity Rule" to 3 decimal places.)

| Percent Error | ||

| YTM | Duration Rule | Duration-With-Convexity Rule |

| 9% | ________% | ________% |