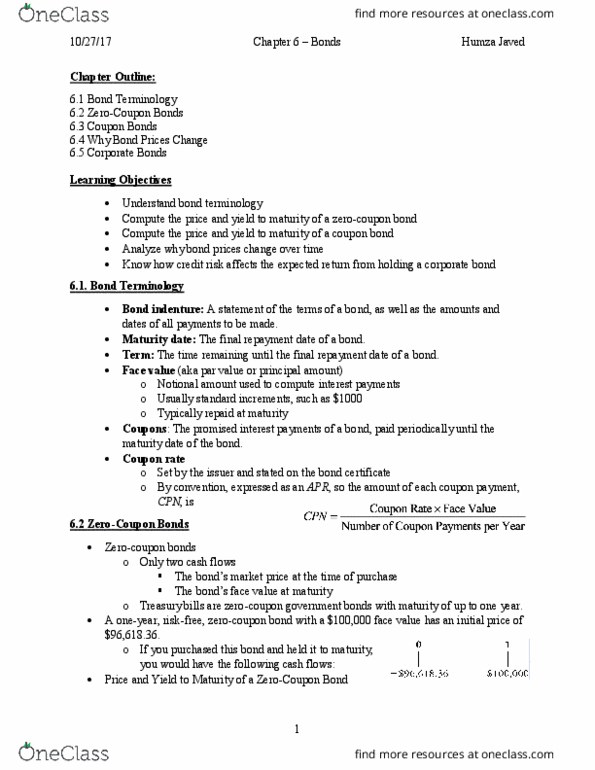

Using the SML Asset W has an expected return of 11.3 percent and a beta of 1.20. If the risk-free rate is 2.4 percent, complete the following table for portfolios of Asset W and a risk-free asset. Illustrate the relationship between portfolio expected return and portfolio beta by plotting the expected returns against the betas. What is the slope of the line that results? Bond 1: Bonds outstanding Years to Maturity Annual coupon rate Coupons per year Bond price (% of par) Bond 2: Bonds outstanding Years to Maturity Annual coupon rate Coupons per year Bond price (% of par) Common stock Shares outstanding Beta Share price Preferred stock outstanding Shares outstanding Coupon rate Share price Market Market risk premium Risk-free rate Tax rate Output Area: Capital Market Value Structure Cost Bond 1 before tax Bond 1 Bond 1 after tax Bond 2 before tax Bond 2 Bond 2 after tax Common stock Common Preferred stock Preferred Total firm $- 0.00% WACC Need the answer in an excel format

Using the SML Asset W has an expected return of 11.3 percent and a beta of 1.20. If the risk-free rate is 2.4 percent, complete the following table for portfolios of Asset W and a risk-free asset. Illustrate the relationship between portfolio expected return and portfolio beta by plotting the expected returns against the betas. What is the slope of the line that results? Bond 1: Bonds outstanding Years to Maturity Annual coupon rate Coupons per year Bond price (% of par) Bond 2: Bonds outstanding Years to Maturity Annual coupon rate Coupons per year Bond price (% of par) Common stock Shares outstanding Beta Share price Preferred stock outstanding Shares outstanding Coupon rate Share price Market Market risk premium Risk-free rate Tax rate Output Area: Capital Market Value Structure Cost Bond 1 before tax Bond 1 Bond 1 after tax Bond 2 before tax Bond 2 Bond 2 after tax Common stock Common Preferred stock Preferred Total firm $- 0.00% WACC Need the answer in an excel format

Related questions

Information on Gerken Power Co., is shown below. Assume the companyâs tax rate is 35 percent.

| Debt: | 9,500 9 percent coupon bonds outstanding, $1,000 par value, 25 years to maturity, selling for 99 percent of par; the bonds make semiannual payments. | |

| Common stock: | 220,000 shares outstanding, selling for $84.00 per share; beta is 1.25. | |

| Preferred stock: | 13,000 shares of 5.75 percent preferred stock outstanding, currently selling for $97.00 per share. | |

| Market: | 7 percent market risk premium and 4.8 percent risk-free rate. |