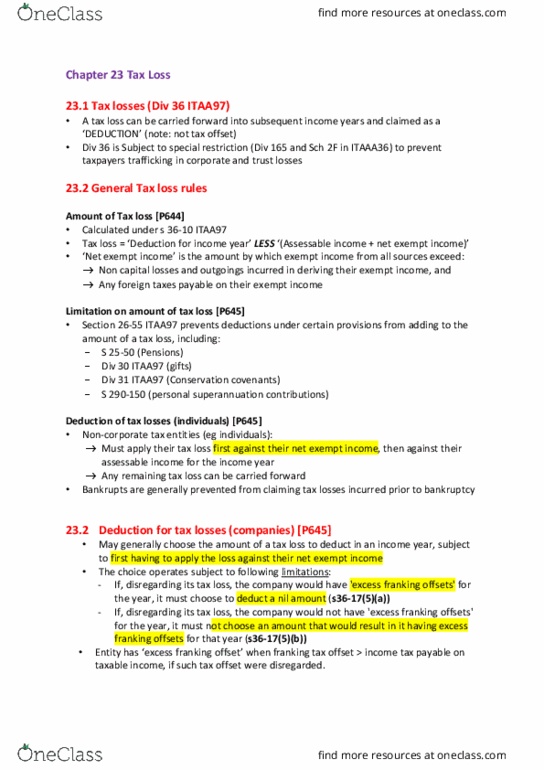

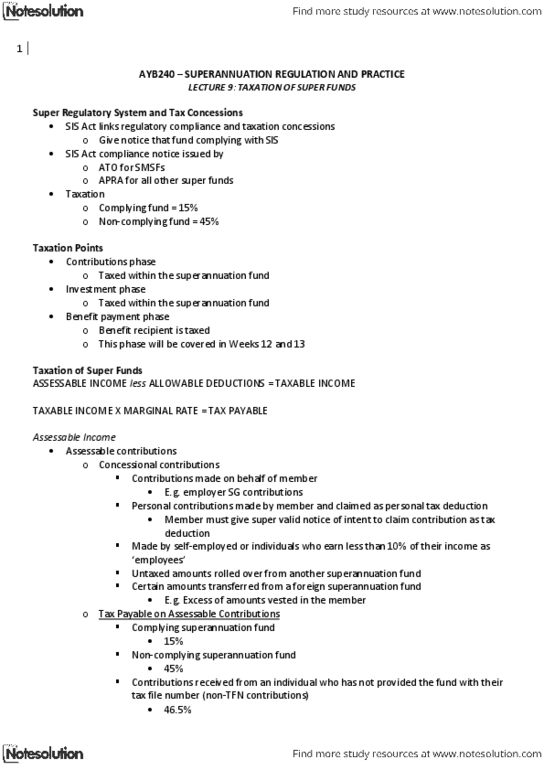

AYB320 Lecture Notes - Lecture 8: Answering Machine, Independent Contractor, Personal Services

Document Summary

Lecture 8 tax planning and anti-avoidance provisions. Outline of the provisions (part 2-42 (divisions 84 to 87) apply from 1 july 2000) Only assessable section the alienation of psi (ie the diversion of income generated by personal services through an interposed entity); and. The over-claiming of income tax deductions by individual contractors and interposed entities providing personal services. Alienation of psi occurs when the services of an individual are provided through an interposed entity rather than directly by the individual who performs the services. When alienation occurs, income may be retained in the entity and either taxed at the lower rate available to the entity and/or diverted to various associates, allowing a lower rate of tax to be paid on that income. The use of interposed entities is also perceived as a means to obtain tax deductions that would not be available to an individual providing the same services as an employee.