AFM101 Study Guide - Midterm Guide: Current Asset, Current Liability, Financial Statement

34 views3 pages

15 Oct 2013

School

Department

Course

Professor

30

AFM101 Full Course Notes

Verified Note

30 documents

Document Summary

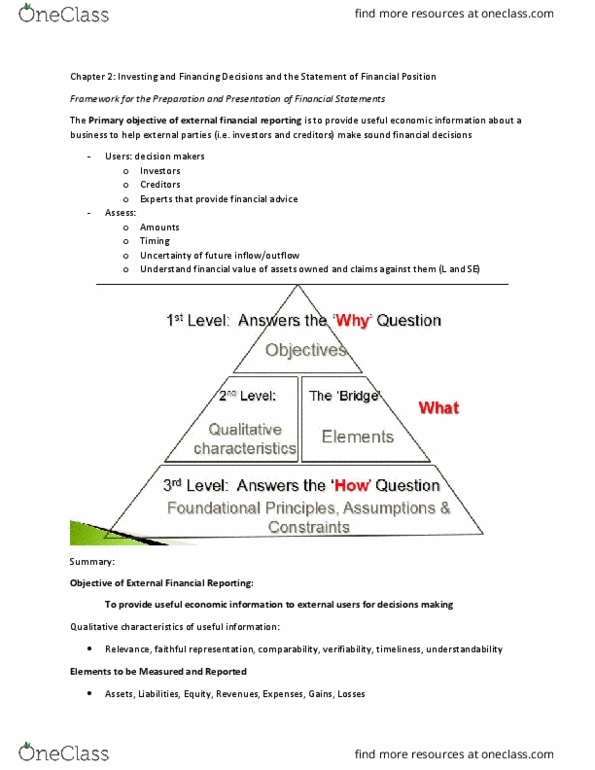

Primary objective of external financial reporting: provides useful economic info about a business to help external parties make sound financial decisions. Summary of financial accounting and reporting: page 48 exhibit2. 1. Basic accounting principle: cost principle: requires assets to be recorded at the historical cash-equivalent cost, which is cash paid plus the current monetary value of all non-cash considerations also given in the exchange, on the date of the transaction. Assets: economic resources controlled by an entity as a result of past transactions or events and from which future economic benefits may be concerned. Current assets: assets that will be used or turned into cash, normally within one year. Inventory is always considered to be a current asset. List assets in order of liquidity, which means how soon they can be transformed into cash. Non-current assets: they will be used or turned into cash over a period longer than the next year.

Get access

Grade+20% off

$8 USD/m$10 USD/m

Billed $96 USD annually

Homework Help

Study Guides

Textbook Solutions

Class Notes

Textbook Notes

Booster Class

40 Verified Answers

Related Documents

Related Questions

Listed below are several information, characteristics, andaccounting principles and assumptions. Match the term with theappropriate phrase that states its application.

(Points : 30)

| Potential Matches: |

| 1 : Application of the same accounting principles as in thepreceding year |

| 2 : Earning process completed and realized or realizable |

| 3 : Notes as part of necessary information to a fairpresentation |

| 4 : Valuing assets at amounts originally paid for them |

| 5 : Yearly financial reports |

| 6 : Stable dollar assumption |

| 7 : Affairs of the business distinguished from those of itsowners |

| 8 : Presentation of error-free information withrepresentational faithfulness |

| 9 : Business enterprise assumed to have a long life |

| 10 : Accruals and deferrals in adjusting and closingprocess |

| Answer |

| : Monetary unit assumption |

| : Revenue recognition principle |

| : Reliability characteristic |

| : Periodicity assumption |

| : Matching principle |

| : Full disclosure principle |

| : Economic entity assumption |

| : Going concern assumption |

| : Historical cost principle |

| : Consistency characteristic |