MGT120H5 Chapter Notes - Chapter 3: Trial Balance, Accrual, Income Statement

12

MGT120H5 Full Course Notes

Verified Note

12 documents

Document Summary

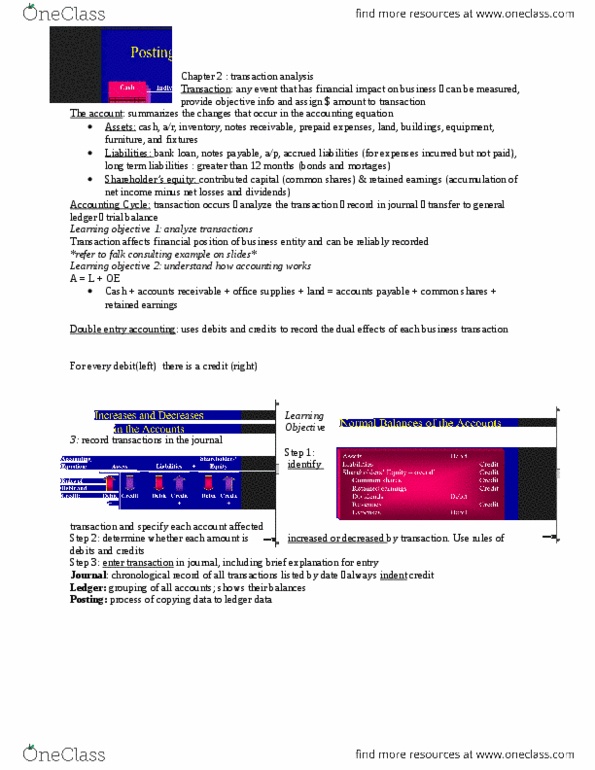

Learning objective 1: relate accrual accounting and cash flows. The business cycle: entity 1 has cash: purchase inventory, entity 2 holds inventory: sale of inventory on account, entity 3 has a receivable: collection of receivable. Accrual basis of accounting (non cash transactions): revenue recorded when earned, expenses recorded when incurred regardless when cash received: e. g. purchase of inventory on account, depreciation expense, usage of prepaid rent. Cash basis of accounting: transactions recorded when cash received/paid. Time period concept: business need regular progress reports, so accountants prepare financial statements for specific periods and at regular intervals (monthly, quarterly and yearly) Learning objective 2: recognize revenue and record expenses. Revenue principle: governs when to record revenue and amount of revenue to record. Recording expenses: as revenue earned, firm incurs expenses identify all expenses incurred during the period and measure the expenses and record.