ACCG340 Study Guide - Final Guide: Audit Evidence, Wu Xing, Australia Iv

19 Jun 2018

School

Department

Course

Professor

1"

"

WK 1

Auditing & Assurance

1. Differences

Accounting

• provides

financial information

for

§ decision making

§ control

§ accountability

Assurance

• Provides confidence as to

reliability

of provided information

• Various levels (reasonable, limited) depending on nature and extent of

procedures and objectivity of evidence

Auditing

•

Provides (reasonable, never absolute level) assurance

that accounting

information is

§ relevant

§ reliable

§ comparable

§ understandable

§ conveys a true and fair view

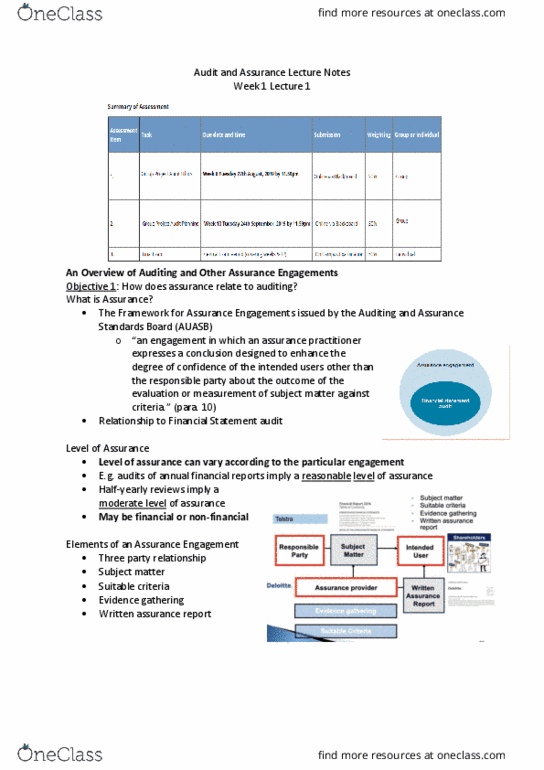

2. Definition & elements of an assurance engagement (audit engagement)

a) ‘engagement in which an assurance practitioner expresses a conclusion designed to

enhance the degree of confidence of the intended users, other than the responsible

party, about the outcome of the evaluation or measurement of a subject matter against

criteria’

b)

Five elements

1.

Three-party

relationship involving assurance practitioner, responsible party

= client, and intended users

2. Subject matter – financial information itself

3. Suitable criteria

4. Sufficient appropriate evidence – quantity & quality of information

5. Written assurance report – auditor report

3. Definition of Auditing

a) Service to provide

reasonable

(i.e. high level) assurance through issue of an opinion

about an accountability matter (such as a financial report).

b) The focus of this unit is predominantly on the audit of the general purpose financial

report, although we will examine other assurance services in the latter portion of

the course.

2"

"

4. Assurance Framework

5. Australian Auditing Standards (ASAs)

)