FINS1613 Study Guide - Quiz Guide: The Australian Financial Review, Yield Curve, United States Treasury Security

Get access

Related Documents

Related Questions

1.) Suppose Oppenheimer Bank is offering a 30-year mortgage with an EAR of 6.800%. If you plan to borrow $150,000, what will be your monthly payment? (Note: Be careful not to round any intermediate steps less than six decimal places.) Your monthly payment will be $______

2.) You are looking to buy a car and you have been offered a loan with an APR of 6%, compounded monthly.

a. What is the true monthly rate of interest? 0.5%

b. What is the EAR?

3.) You have just sold your house for $1,000,000 in cash. Your mortgage was originally a 30-year mortgage with monthly payments and an initial balance of $800,000.The mortgage is currently exactly 18½ years old, and you have just made a payment. If the interest rate on the mortgage is 5.25% (APR), how much cash will you have from the sale once you pay off the mortgage? (Note: Be careful not to round any intermediate steps less than six decimal places.)

Cash that remains after payoff of mortgage is __________

4.) If the rate of inflation is 4.5%, what nominal interest rate is necessary for you to earn a 2.3% real interest rate on your investment? (Note: Be careful not to round any intermediate steps less than six decimal places.)

The nominal interest rate is ___%

5.) Use the table for the question(s) below.

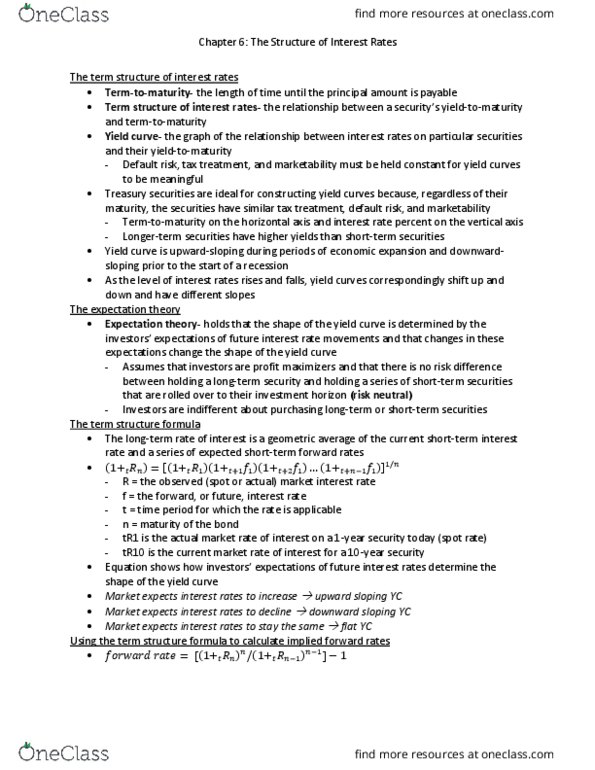

Suppose the term structure of interest rates is shown below:

|

Term |

1 year |

2 years |

3 years |

5 years |

10 years |

20 years |

|

Rate (EAR%) |

5.00% |

4.80% |

4.60% |

4.50% |

4.25% |

4.15% |

What is the shape of the yield curve and what expectations are investors likely to have about future interest rates?

A. inverted; higher

B. inverted; lower

C. normal; higher

D. normal; lower

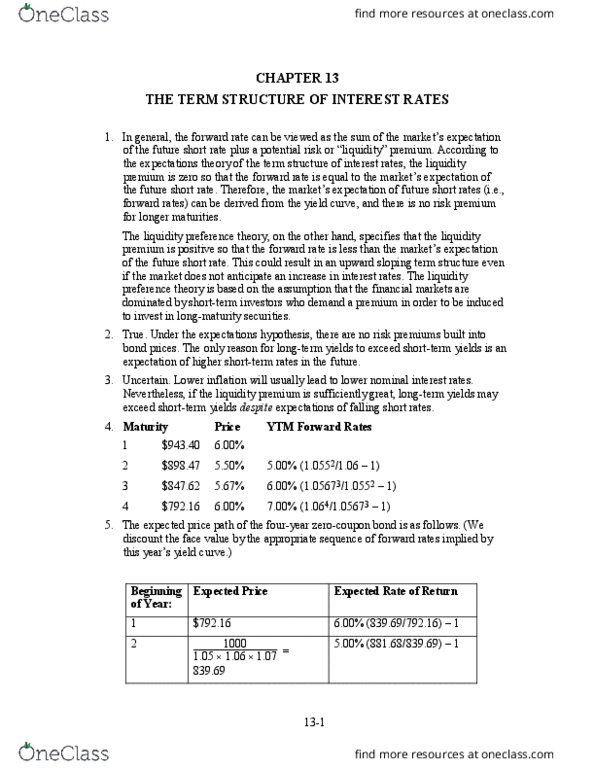

The current yield curve for default-free zero-coupon bonds is as follows:

| Maturity (years) | YTM | |

| 1 | 11.0 | % |

| 2 | 12.0 | |

| 3 | 13.0 | |

a. What are the implied one-year forward rates? (Do not round intermediate calculations. Round your answers to 2 decimal places.)

| Maturity (years) | YTM | Forward Rate | ||

| 1 | 11.0 | % | ||

| 2 | 12.0 | % | % | |

| 3 | 13.0 | % | % | |

b. Assume that the pure expectations hypothesis of the term structure is correct. If market expectations are accurate, what will the pure yield curve (that is, the yields to maturity on one- and two-year zero-coupon bonds) be next year?

| There will be a shift upwards in next year's curve. | |

| There will be a shift downwards in next year's curve. | |

| There will be no change in next year's curve. |

c-1. If you purchase a two-year zero-coupon bond now, what is the expected total rate of return over the next year? (Hint: Compute the current and expected future prices.) Ignore taxes. (Do not round intermediate calculations. Round your answer to 2 decimal places.)

Expected total rate of return %

c-2. If you purchase a three-year zero-coupon bond now, what is the expected total rate of return over the next year? (Hint: Compute the current and expected future prices.) Ignore taxes. (Do not round intermediate calculations. Round your answer to 2 decimal places.)

Expected total rate of return %