ACCT3011 Study Guide - Quiz Guide: Retained Earnings, Book Value, Share Capital

This preview shows half of the first page of the document.

Unlock all 2 pages and 3 million more documents.

Document Summary

Get access

Related Documents

Related Questions

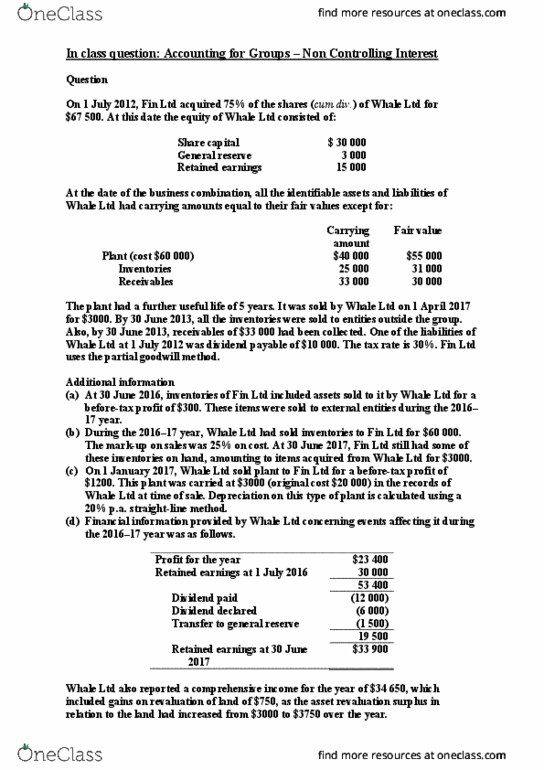

On 1 July 2017, Panda Ltd acquired all the issued shares ofSmarty Ltd. Panda Ltd paid $250,000 more than the equity itacquired in the fair value of Smarty Ltdâs net assets. At the dateof acquisition, the shareholderâs equity of S

On 1 July 2017, Panda Ltd acquired all the issued shares ofSmarty Ltd. Panda Ltd paid $250,000 more than the equity itacquired in the fair value of Smarty Ltdâs net assets. At the dateof acquisition, the shareholderâs equity of Smarty Ltd was asfollows.

$

Share capital

100,000

Retained earnings

175,000

Total

275,000

All the assets and liabilities of Smarty Ltd were recorded atamounts equal to their fair values at the acquisition date, exceptfor some assets detailed below.

Remaining useful life

Cost

Carrying amount

Fair value

$

$

$

Plant

5 years

180,000

90,000

120,000

Computer equipment

5 years

90,000

40,000

60,000

Required:

Prepare the acquisition analysis at 1 July 2017.

Prepare the consolidation worksheet entries for Panda Ltdâs groupat 1 July 2017.

Prepare the consolidation worksheet entries for Panda Ltdâs groupat 30 June 2018.

Question 1

Max. marks allocated

Acquisition analysis

3

Consolidation entries at 1 July 2017

6

Consolidation entries at 30 June 2018

10

Presentation

1

Total

20

Question 2 [35 marks]

Topic 2: Consolidation: Intra-group transactions

On 1 July 2015, Ping Pong Ltd acquired all the issued shares ofSing Song Ltd. At the date of acquisition, the shareholdersâ equityof Sing Song Ltd consisted of share capital $120,000; generalreserve $25,000 and retained earnings $55,000. The identifiable netassets of Sing Song Ltd were recorded at amounts equal to theirfair values, except for the following assets:

Carrying amount

Fair value

$

$

Land

100,000

130,000

Inventories

78,500

86,100

Machinery (cost $86,000)

52,000

56,000

Vehicles (cost $58,000)

47,000

53,000

The assets of Sing Song Ltd at acquisition date includedgoodwill recorded at $15,000 arising from a business combinationtransaction in 2011. As at the date of acquisition, the vehiclesand machinery were expected to have a further useful life of 6 and8 years respectively, with benefits to be received evenly overthose periods. Inventories on hand on 1 July 2015 was all sold by31 January 2016. The land owned at 1 July 2015 was sold inSeptember 2016 for $150,000. The machinery on hand at 1 July 2015was sold on 1 January 2018 for $38,000.

Adjustments for the differences between carrying amount and fairvalues of assets and liabilities on hand at acquisition date arerecognised on consolidation. When assets are sold or derecognised,any related valuation reserves are transferred to retainedearnings.

At 1 July 2015, Sing Song Ltd owned but had not recorded aninternally generated brand name, an identifiable asset included aspart of the business combination transaction. This brand name wasconsidered by Ping Pong Ltd to have a fair value of $29,000 and anindefinite useful life. An impairment test conducted with respectto the brand name on 30 June 2018 concluded that its recoverableamount at that date was $2,000 less than its carrying amount.

In June 2017, Sing Song Ltd paid a share dividend worth $20,000from the general reserve on hand at 1 July 2015.

The trial balances of both companies at 30 June 2018 showed thefollowing balances:

Ping Pong Ltd

Sing Song Ltd

Dr ($)

Cr ($)

Dr ($)

Cr ($)

Sales revenue

450,000

320,000

Dividend revenue

17,000

-

Other income

11,400

17,000

Proceeds on sale of equipment

18,000

-

Proceeds on sale of machinery

-

38,000

Cost of sales

210,000

192,550

Income tax expense

30,000

32,000

Depreciation and other expenses

39,000

36,000

Carrying amount of equipment sold

21,000

-

Carrying amount of machinery sold

-

30,500

Dividend paid

10,000

5,000

Dividend declared

20,000

12,000

Transfer to general reserve

10,000

5,000

Share capital

200,000

140,000

General reserve

35,000

10,000

Retained earnings (1 July 2017)

51,300

67,500

Accounts payable

69,500

36,000

Loan payable (due 30 June 2022)

25,000

15,000

Dividend payable

20,000

12,000

Provisions

12,500

9,300

Current tax liability

43,000

34,000

Deferred tax liability

11,800

5,000

Accumulated depreciation-vehicles

16,400

60,000

Accumulated depreciation-equipment

-

34,500

8%Debentures (matures 30 June 2021)

25,000

-

Cash

2,500

1,250

Receivables

27,000

13,000

Inventories

39,700

24,500

Other current assets

15,200

8,200

Deferred tax assets

7,500

3,500

Vehicles

88,000

158,000

Equipment

-

42,000

Land

140,000

180,000

Financial assets

68,000

14,800

Goodwill

28,000

15,000

Shares in Sing Song Ltd

250,000

-

Debentures in Ping Pong Ltd

-

25,000

1,005,900

1,005,900

798,300

798,300

Additional information:

On 1 January 2018, Ping Pong Ltd sold an item of equipment toSing Song Ltd for $18,000. The equipment had a carrying amount atthe date of sale of $21,000. Both companies depreciate equipment at20% on a straight line basis.

On 1 May 2017, Sing Song Ltd sold a machine to Ping Pong Ltd for$7,800. The machine had a carrying amount of $7,000 at the date ofsale. Ping Pong Ltd recorded the machine as inventories. Theinventories item was sold to an external party in November 2017 for$8,200.

All interests on the 8% debentures has been paid and brought toaccount in the records of both companies.

During the 2017-2018 financial year, Ping Pong Ltd sold inventoriesto Sing Song Ltd for $75,000. The cost of these inventories to SingSong Ltd was $70,000. Of these inventories, 25% is still on hand at30 June 2018.

The transfer to the general reserve recorded by Sing Song Ltd inthe current year was from retained earnings recorded at 1 July2015.

The tax rate is 30%.

Required:

Prepare an acquisition analysis.

Prepare the consolidation worksheet entries necessary to preparethe consolidated financial statements for the year ending 30 June2018 for the group comprising Ping Pong Ltd and Sing Song Ltd.

Note: you are not required to prepare the consolidationworksheet and the consolidated financial statements.

marty Ltd was as follows.

$ | |

Share capital | 100,000 |

Retained earnings | 175,000 |

Total | 275,000 |

All the assets and liabilities of Smarty Ltd were recorded atamounts equal to their fair values at the acquisition date, exceptfor some assets detailed below.

Remaining useful life | Cost | Carrying amount | Fair value | |

$ | $ | $ | ||

Plant | 5 years | 180,000 | 90,000 | 120,000 |

Computer equipment | 5 years | 90,000 | 40,000 | 60,000 |

Required:

Prepare the acquisition analysis at 1 July 2017.

Prepare the consolidation worksheet entries for Panda Ltdâsgroup at 1 July 2017.

Prepare the consolidation worksheet entries for Panda Ltdâsgroup at 30 June 2018.

Question 1 | Max. marks allocated |

Acquisition analysis | 3 |

Consolidation entries at 1 July 2017 | 6 |

Consolidation entries at 30 June 2018 | 10 |

Presentation | 1 |

Total | 20 |

Question 2 [35 marks]

Topic 2: Consolidation: Intra-grouptransactions

On 1 July 2015, Ping Pong Ltd acquired all the issued shares ofSing Song Ltd. At the date of acquisition, the shareholdersâ equityof Sing Song Ltd consisted of share capital $120,000; generalreserve $25,000 and retained earnings $55,000. The identifiable netassets of Sing Song Ltd were recorded at amounts equal to theirfair values, except for the following assets:

Carrying amount | Fair value | |

$ | $ | |

Land | 100,000 | 130,000 |

Inventories | 78,500 | 86,100 |

Machinery (cost $86,000) | 52,000 | 56,000 |

Vehicles (cost $58,000) | 47,000 | 53,000 |

The assets of Sing Song Ltd at acquisition date includedgoodwill recorded at $15,000 arising from a business combinationtransaction in 2011. As at the date of acquisition, the vehiclesand machinery were expected to have a further useful life of 6 and8 years respectively, with benefits to be received evenly overthose periods. Inventories on hand on 1 July 2015 was all sold by31 January 2016. The land owned at 1 July 2015 was sold inSeptember 2016 for $150,000. The machinery on hand at 1 July 2015was sold on 1 January 2018 for $38,000.

Adjustments for the differences between carrying amount and fairvalues of assets and liabilities on hand at acquisition date arerecognised on consolidation. When assets are sold or derecognised,any related valuation reserves are transferred to retainedearnings.

At 1 July 2015, Sing Song Ltd owned but had not recorded aninternally generated brand name, an identifiable asset included aspart of the business combination transaction. This brand name wasconsidered by Ping Pong Ltd to have a fair value of $29,000 and anindefinite useful life. An impairment test conducted with respectto the brand name on 30 June 2018 concluded that its recoverableamount at that date was $2,000 less than its carrying amount.

In June 2017, Sing Song Ltd paid a share dividend worth $20,000from the general reserve on hand at 1 July 2015.

The trial balances of both companies at 30 June 2018 showed thefollowing balances:

Ping Pong Ltd | Sing Song Ltd | |||

Dr ($) | Cr ($) | Dr ($) | Cr ($) | |

Sales revenue | 450,000 | 320,000 | ||

Dividend revenue | 17,000 | - | ||

Other income | 11,400 | 17,000 | ||

Proceeds on sale of equipment | 18,000 | - | ||

Proceeds on sale of machinery | - | 38,000 | ||

Cost of sales | 210,000 | 192,550 | ||

Income tax expense | 30,000 | 32,000 | ||

Depreciation and other expenses | 39,000 | 36,000 | ||

Carrying amount of equipment sold | 21,000 | - | ||

Carrying amount of machinery sold | - | 30,500 | ||

Dividend paid | 10,000 | 5,000 | ||

Dividend declared | 20,000 | 12,000 | ||

Transfer to general reserve | 10,000 | 5,000 | ||

Share capital | 200,000 | 140,000 | ||

General reserve | 35,000 | 10,000 | ||

Retained earnings (1 July 2017) | 51,300 | 67,500 | ||

Accounts payable | 69,500 | 36,000 | ||

Loan payable (due 30 June 2022) | 25,000 | 15,000 | ||

Dividend payable | 20,000 | 12,000 | ||

Provisions | 12,500 | 9,300 | ||

Current tax liability | 43,000 | 34,000 | ||

Deferred tax liability | 11,800 | 5,000 | ||

Accumulated depreciation-vehicles | 16,400 | 60,000 | ||

Accumulated depreciation-equipment | - | 34,500 | ||

8%Debentures (matures 30 June 2021) | 25,000 | - | ||

Cash | 2,500 | 1,250 | ||

Receivables | 27,000 | 13,000 | ||

Inventories | 39,700 | 24,500 | ||

Other current assets | 15,200 | 8,200 | ||

Deferred tax assets | 7,500 | 3,500 | ||

Vehicles | 88,000 | 158,000 | ||

Equipment | - | 42,000 | ||

Land | 140,000 | 180,000 | ||

Financial assets | 68,000 | 14,800 | ||

Goodwill | 28,000 | 15,000 | ||

Shares in Sing Song Ltd | 250,000 | - | ||

Debentures in Ping Pong Ltd | - | 25,000 | ||

1,005,900 | 1,005,900 | 798,300 | 798,300 | |

Additional information:

On 1 January 2018, Ping Pong Ltd sold an item of equipment toSing Song Ltd for $18,000. The equipment had a carrying amount atthe date of sale of $21,000. Both companies depreciate equipment at20% on a straight line basis.

On 1 May 2017, Sing Song Ltd sold a machine to Ping Pong Ltd for$7,800. The machine had a carrying amount of $7,000 at the date ofsale. Ping Pong Ltd recorded the machine as inventories. Theinventories item was sold to an external party in November 2017 for$8,200.

All interests on the 8% debentures has been paid and brought toaccount in the records of both companies.

During the 2017-2018 financial year, Ping Pong Ltd soldinventories to Sing Song Ltd for $75,000. The cost of theseinventories to Sing Song Ltd was $70,000. Of these inventories, 25%is still on hand at 30 June 2018.

The transfer to the general reserve recorded by Sing Song Ltd inthe current year was from retained earnings recorded at 1 July2015.

The tax rate is 30%.

Required:

Prepare an acquisition analysis.

Prepare the consolidation worksheet entries necessary to preparethe consolidated financial statements for the year ending 30 June2018 for the group comprising Ping Pong Ltd and Sing Song Ltd.

Note: you are not required to prepare the consolidationworksheet and the consolidated financial statements.

Topic 2: Consolidation: Intra-grouptransactions

On 1 July 2015, Ping Pong Ltd acquired all the issued shares ofSing Song Ltd. At the date of acquisition, the shareholdersâ equityof Sing Song Ltd consisted of share capital $120,000; generalreserve $25,000 and retained earnings $55,000. The identifiable netassets of Sing Song Ltd were recorded at amounts equal to theirfair values, except for the following assets:

Carrying amount | Fair value | |

$ | $ | |

Land | 100,000 | 130,000 |

Inventories | 78,500 | 86,100 |

Machinery (cost $86,000) | 52,000 | 56,000 |

Vehicles (cost $58,000) | 47,000 | 53,000 |

The assets of Sing Song Ltd at acquisition date includedgoodwill recorded at $15,000 arising from a business combinationtransaction in 2011. As at the date of acquisition, the vehiclesand machinery were expected to have a further useful life of 6 and8 years respectively, with benefits to be received evenly overthose periods. Inventories on hand on 1 July 2015 was all sold by31 January 2016. The land owned at 1 July 2015 was sold inSeptember 2016 for $150,000. The machinery on hand at 1 July 2015was sold on 1 January 2018 for $38,000.

Adjustments for the differences between carrying amount and fairvalues of assets and liabilities on hand at acquisition date arerecognised on consolidation. When assets are sold or derecognised,any related valuation reserves are transferred to retainedearnings.

At 1 July 2015, Sing Song Ltd owned but had not recorded aninternally generated brand name, an identifiable asset included aspart of the business combination transaction. This brand name wasconsidered by Ping Pong Ltd to have a fair value of $29,000 and anindefinite useful life. An impairment test conducted with respectto the brand name on 30 June 2018 concluded that its recoverableamount at that date was $2,000 less than its carrying amount.

In June 2017, Sing Song Ltd paid a share dividend worth $20,000from the general reserve on hand at 1 July 2015.

The trial balances of both companies at 30 June 2018 showed thefollowing balances:

Ping Pong Ltd | Sing Song Ltd | |||

Dr ($) | Cr ($) | Dr ($) | Cr ($) | |

Sales revenue | 450,000 | 320,000 | ||

Dividend revenue | 17,000 | - | ||

Other income | 11,400 | 17,000 | ||

Proceeds on sale of equipment | 18,000 | - | ||

Proceeds on sale of machinery | - | 38,000 | ||

Cost of sales | 210,000 | 192,550 | ||

Income tax expense | 30,000 | 32,000 | ||

Depreciation and other expenses | 39,000 | 36,000 | ||

Carrying amount of equipment sold | 21,000 | - | ||

Carrying amount of machinery sold | - | 30,500 | ||

Dividend paid | 10,000 | 5,000 | ||

Dividend declared | 20,000 | 12,000 | ||

Transfer to general reserve | 10,000 | 5,000 | ||

Share capital | 200,000 | 140,000 | ||

General reserve | 35,000 | 10,000 | ||

Retained earnings (1 July 2017) | 51,300 | 67,500 | ||

Accounts payable | 69,500 | 36,000 | ||

Loan payable (due 30 June 2022) | 25,000 | 15,000 | ||

Dividend payable | 20,000 | 12,000 | ||

Provisions | 12,500 | 9,300 | ||

Current tax liability | 43,000 | 34,000 | ||

Deferred tax liability | 11,800 | 5,000 | ||

Accumulated depreciation-vehicles | 16,400 | 60,000 | ||

Accumulated depreciation-equipment | - | 34,500 | ||

8%Debentures (matures 30 June 2021) | 25,000 | - | ||

Cash | 2,500 | 1,250 | ||

Receivables | 27,000 | 13,000 | ||

Inventories | 39,700 | 24,500 | ||

Other current assets | 15,200 | 8,200 | ||

Deferred tax assets | 7,500 | 3,500 | ||

Vehicles | 88,000 | 158,000 | ||

Equipment | - | 42,000 | ||

Land | 140,000 | 180,000 | ||

Financial assets | 68,000 | 14,800 | ||

Goodwill | 28,000 | 15,000 | ||

Shares in Sing Song Ltd | 250,000 | - | ||

Debentures in Ping Pong Ltd | - | 25,000 | ||

1,005,900 | 1,005,900 | 798,300 | 798,300 | |

Additional information:

On 1 January 2018, Ping Pong Ltd sold an item of equipment toSing Song Ltd for $18,000. The equipment had a carrying amount atthe date of sale of $21,000. Both companies depreciate equipment at20% on a straight line basis.

On 1 May 2017, Sing Song Ltd sold a machine to Ping Pong Ltd for$7,800. The machine had a carrying amount of $7,000 at the date ofsale. Ping Pong Ltd recorded the machine as inventories. Theinventories item was sold to an external party in November 2017 for$8,200.

All interests on the 8% debentures has been paid and brought toaccount in the records of both companies.

During the 2017-2018 financial year, Ping Pong Ltd soldinventories to Sing Song Ltd for $75,000. The cost of theseinventories to Sing Song Ltd was $70,000. Of these inventories, 25%is still on hand at 30 June 2018.

The transfer to the general reserve recorded by Sing Song Ltd inthe current year was from retained earnings recorded at 1 July2015.

The tax rate is 30%.

Required:

Prepare an acquisition analysis.

Prepare the consolidation worksheet entries necessary to preparethe consolidated financial statements for the year ending 30 June2018 for the group comprising Ping Pong Ltd and Sing Song Ltd.

Note: you are not required to prepare the consolidationworksheet and the consolidated financial statements.

Topics 1 to 3 - Consolidation: Principles, accounting requirements, intra-group transactions and non-controlling interests

Parent Ltd acquired 80% of the issued shares of Subsidiary Ltd on 1 July 2014. At the acquisition date, the equity of Subsidiary Ltd consisted of Share Capital of $200,000; Retained Earnings of $ 74,000 and General Reserve of $6,000.

Parent Ltd uses the full goodwill method. The fair value of non-controlling interest at 1 July 2014 was $63,000.

All the identifiable net assets of Subsidiary Ltd were recorded at fair value at the date of acquisition, except for the following assets:4

| Carrying amount | Fair value | |

| $ | $ | |

| Plant (cost $150,000) | 100,000 | 110,000 |

| Land | 60,000 | 76,000 |

The plant has a further 10-year life, with benefits expected to be received evenly over that period. The land was sold on 1 February 2015 for $80,000. Any valuation reserve in relation to the land is transferred to retained earnings on consolidation.

Three years after acquisition, the financial information at 30 June 2017 of the two companies appears as follows:

|

| Parent Ltd | Subsidiary Ltd |

| $ | $ | |

| Sales | 632,000 | 440,000 |

| Other revenue: | ||

| Debenture interest | 10,000 | - |

| Management and consulting fees | 10,000 | - |

| Dividends from Subsidiary Ltd | 24,000 | - |

| Total revenue | 676,000 | 440,000 |

| Cost of sales | 260,000 | 170,000 |

| Manufacturing expenses | 180,000 | 120,000 |

| Depreciation on plant | 30,000 | 30,000 |

| Administrative expenses | 30,000 | 16,000 |

| Financial expenses | 22,000 | 10,000 |

| Other expenses | 28,000 | 24,000 |

| Total expenses | 550,000 | 370,000 |

| Profit before tax | 126,000 | 70,000 |

| Income tax expense | (50,000) | (34,000) |

| Operating profit after tax | 76,000 | 36,000 |

| Retained earnings 1 July 2016 | 100,000 | 90,000 |

| 176,000 | 126,000 | |

| Transfer to general reserve | 6,000 | - |

| Interim dividend paid | 20,000 | 20,000 |

| Final dividends declared | 20,000 | 10,000 |

| 46,000 | 30,000 | |

| Retained earnings 30 June 2017 | 130,000 | 96,000 |

| General reserve | 100,000 | 20,000 |

| Other components of equity | 26,000 | 20,000 |

| Share capital | 600,000 | 200,000 |

| Debentures | 400,000 | 200,000 |

| Current tax liability | 50,000 | 34,000 |

| Dividend payable | 20,000 | 10,000 |

| Deferred tax liability | - | 14,000 |

| Other liabilities | 180,000 | 24,000 |

| 1,506,000 | 618,000 | |

| Assets | ||

| Financial assets | 100,000 | 120,000 |

| Debentures in Subsidiary Ltd | 200,000 | - |

| Shares in Subsidiary Ltd | 263,200 | - |

| Plant (cost) | 240,000 | 204,000 |

| Accumulated depreciation â plant | (130,000) | (110,000) |

| Other depreciable assets | 152,000 | 110,000 |

| Accumulated depreciation | (80,000) | (50,000) |

| Inventory | 180,000 | 170,000 |

| Deferred tax asset | 170,800 | 60,000 |

| Land | 402,000 | 114,000 |

| Dividend receivable | 8,000 | - |

| 1,506,000 | 618,000 |

Additional information:

(a) The inventory on hand of Subsidiary Ltd on 1 July 2016 included a quantity priced at $20,000 that was transferred from Parent Ltd during the prior financial year. This inventory had cost Parent Ltd $15,000. This entire inventory was sold by Subsidiary Ltd to parties external to the group during the current financial year.

(b) Subsidiary Ltd sold inventory to Parent Ltd for $120,000 during the year. This inventory had an original cost to Subsidiary Ltd of $110,000. This entire inventory was held by Parent Ltd during the year.

(c) On 1 January 2016, Subsidiary Ltd sold an item from its inventory to Parent Ltd for $40,000. Parent Ltd had treated this item as an addition to its plant. The item was put into service as soon as received by Parent Ltd and depreciation charged at 20% p.a. The cost of that item to Subsidiary Ltd was $30,000.

(d) The management and consulting fees of Parent Ltd were all paid by Subsidiary Ltd and represented charges made for administration $4,400 and technical services $5,600. The latter were recognised as manufacturing expenses by Subsidiary Ltd.

(e) All debentures issued by Subsidiary Ltd are held by Parent Ltd. The related interest has been recorded by Parent Ltd accordingly and Subsidiary Ltd recorded the interest paid in financial expenses.

(f) Other components of equity relate to movements in the fair values of the financial assets. The balance of these accounts on 1 July 2016 was $20,000 for Parent Ltd and $16,000 for Subsidiary Ltd.

(g) The tax rate is 30%.

Required:

Prepare an acquisition analysis and the consolidation journal entries necessary for preparation of the consolidated financial statements for the year ending 30 June 2017 for the group comprising Parent Ltd and Subsidiary Ltd.

Note: show all necessary workings and narrations.

| Question 1 | Max. marks allocated |

| Acquisition analysis | 5 |

| Consolidation entries - accuracy | 35 |

| Total | 40 |