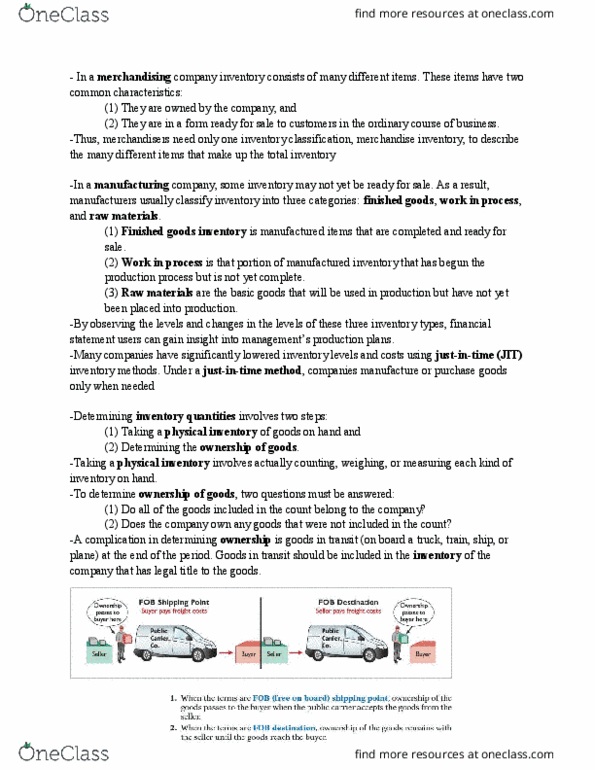

ACCT 1220 Study Guide - Midterm Guide: Internal Control, Profit Margin, General Ledger

Document Summary

Get access

Related Documents

Related Questions

1) Which of the following items would be reported net of taxesafter income from continuing operations?

Select one:

a. Gain or loss on the sale of property.

b. Loss due to a factory strike.

c. Interest expense.

d. Gain or loss on the sale of a major segment of theentity.

2)

Given the following list of accounts, calculate TotalAssets:

Accounts Receivable | $ 5,000 |

Capital Stock | 20,000 |

Cash | 14,300 |

Equipment | 15,400 |

Fees Earned | 44,400 |

Miscellaneous Expense | 18,200 |

Rent Expense | 4,150 |

Retained Earnings | 6,550 |

Wages Expense | 13,900 |

Select one:

a. $54,700

b. $26,550

c. $79,100

d. $34,700

3)

Which of the following is NOT associated with accrual basisaccounting?

Select one:

a. Income statement.

b. Matching principle.

c. Statement of cash flows.

d. Revenue recognition principle.

4)

Which of the following is an example of an intangible asset?

Select one:

a. Trademark

b. Timber

c. Equipment

d. Marketable securities

5)

Which of the following would be shown under the financingactivities section on the statement of cash flows?

Select one:

a. Cash received from customers.

b. The payment of cash to retire a long-term note.

c. Depreciation expense.

d. The proceeds from the sale of a building.

6)

A machine was purchased for $32,000 on April 1st. It has auseful life of 5 years and a residual value of $4,000. What is thedepreciation expense for the first fiscal year ending on December31st under the straight-line method?

Select one:

a. $1,400

b. $6,400

c. $4,200

d. $5,600

7)

The entry to record the signing of a contract to receiveinventory and make payment at a future date includes

Select one:

a. No debits or creditsâjust a memorandum.

b. A debit to cost of goods sold.

c. A credit to cash.

d. A debit to inventory.

8)

An inventory cost flow assumption is NOT needed for a productline

Select one:

a. If all of the inventory available for sale was purchased atthe same unit cost.

b. If all of the inventory looks the same.

c. If there is still some inventory on hand at the end of theyear.

d. If there is no beginning inventory carried over from theprevious accounting period.

9)

Fees received this period from customers for services to beperformed in the next accounting period, would be a(n)

Select one:

a. Expense disclosed on the statement of cash flows.

b. Revenue disclosed on the income statement.

c. Liability disclosed on the balance sheet.

d. Item not included on the financial statements until the nextaccounting period.

10)

Which of the following is TRUE of a corporation?

Select one:

a. They are incorporated with a national agency.

b. At least one owner has unlimited liability.

c. They are a separate taxable entity.

d. More than 70% of businesses are organized this way.

11)

The effects on the accounts of recording the cost of merchandisesold for cash using a perpetual inventory system include an

Select one:

a. Increase in Accounts Payable.

b. Increase in Merchandise Inventory.

c. Increase in Sales.

d. Increase in Cost of Goods Sold;

12)

Which of the following is NOT a limitation of externallyreported accounting information?

Select one:

a. The income statement contains atypical data due to the timingof the fiscal year end.

b. Accounting information relies on estimates.

c. Management has some discretion regarding the reportingclassification and choice of accounting measurement methods.

d. There is a hodge-podge of valuation techniques used on thefinancial statements.

13)

Given the following information regarding merchandise inventoryat the end of the fiscal year:

Ending inventory at cost $34,000

Ending inventory at market $33,400

Which of the following is correct?

Select one:

a. No journal entry should be made based upon the informationgiven.

b. Inventory should be reported on the balance sheet at$34,000.

c. Inventory should be reported on the balance sheet at$33,400.

d. A journal entry should be made to recognize a gain of$600.

14)

Which of the following describes the closing process when acompany has net earnings for the period?

Select one:

a. The Dividends account is debited for its balance.

b. The individual asset accounts are credited for theirbalances.

c. The individual expense accounts are debited for theirbalances.

d. The Income Summary account is debited for its balance.

| . Make all 16 adjustments to journal entries. Remember to include a description under each journal entry. |

| 1 | On March 1, ABC purchased a one-year liability insurance policy for $98,400. | ||||||||

| Upon purchase, the following journal entry was made: | |||||||||

| Dr Prepaid insurance | 98,400 | ||||||||

| Cr Cash | 98,400 | ||||||||

| The expired portion of insurance must be recorded as of 12/31/14. | |||||||||

| Notice that the expired portion from March through November has been recorded already. | |||||||||

| Make sure that the Prepaid Insurance balance after the adjusting entry is correct. | |||||||||

| 2 | Depreciation expense must be recorded for the month of December. | ||||||||

| The building was purchased with cash on February 1, 2014, for $150,000 with a remaining useful life of 30 years and a salvage value of $6,000. | |||||||||

| The method of depreciation for the building is straight-line. | |||||||||

| The equipment was purchased with cash on February 1, 2014, for $60,000 with a remaining useful life of 5 years and a salvage value of $3,000. | |||||||||

| The method of depreciation for the equipment is double-declining balance. | |||||||||

| Depreciation has been recorded for the building and equipment for months February through November. | |||||||||

| 3 | On December 1, XYZ Co. agreed to rent space in ABC's building for $12,000 per month, | ||||||||

| and XYZ paid ABC on December 1 in advance for the first three months' rent. | |||||||||

| The entry made on December 1 was as follows: | |||||||||

| Dr Cash | 36,000 | ||||||||

| Cr Unearned rent revenue | 36,000 | ||||||||

| The unearned revenue account must be adjusted to reflect the amount earned as of 12/31/14. | |||||||||

| 4 | Per timecards, from the last payroll date through December 31, 2014, ABC's employees have worked a total of 250 hours. | ||||||||

| Including payroll taxes, ABC's wage expense averages about $51 per hour. The next payroll date is January 5, 2015. | |||||||||

| The liability for wages payable must be recorded as of 12/31/14. | |||||||||

| 5 | On November 30, 2014, ABC borrowed $235,000 from American National Bank by issuing an interest-bearing note payable. | ||||||||

| This loan is to be repaid in three months (on February 28, 2015), along with interest computed at an annual rate of 6%. | |||||||||

| The entry made on November 30 to record the borrowing was: (for Statement of Cash Flow purposes, consider a financing item) | |||||||||

| Dr Cash | 235,000 | ||||||||

| Cr Notes payable | 235,000 | ||||||||

| On February 28, 2015 ABC must pay the bank the amount borrowed plus interest. | |||||||||

| Assume the beginning balance for Notes Payable is correct. | |||||||||

| Interest through 12/31/14 must be accrued on the $235,000 note. | |||||||||

| 6 | ABC uses a periodic inventory system, and the ending inventory for each year is determined by taking a complete | ||||||||

| physical inventory at year-end. A physical count was taken on December 31, 2014, and the inventory on-hand at | |||||||||

| that time totaled $75,000, which reflects historical cost. | |||||||||

| Record the 2014 Cost of Goods Sold and the 12/31/14 Inventory adjustment. | |||||||||

| Additionally, ABC adheres to GAAP by recording ending inventory at the lower of cost and net realizable value at a total inventory level. | |||||||||

| A review of inventory data further indicated that the current retail sales value of the ending inventory is $110,000 and estimated costs of | |||||||||

| completion and shipping is 15% of retail. Be sure to make an additional adjustment, if necessary, to properly value ending inventory | |||||||||

| using the Loss and Allowance methodology. For Income Statement presentation purposes, be sure to use the Loss Method for accounting | |||||||||

| for adjustments of inventory to market value. | |||||||||

| 7 | It would be unusual for a company to have an asset impairment in Year 1, but for the sake of this example, ABC realized | ||||||||

| that their intangible asset might be impaired on December 31, 2014. Record the impairment if any. | |||||||||

| The expected future net cash flows for this intangible asset totals $30,000, and the fair value of the asset is $27,500. | |||||||||

| 8 | On 7/1/14, ABC purchased 7,000 shares of its own stock from existing stockholders as treasury stock. The cost of the treasury | ||||||||

| stock was $7 per share, or $49,000 in total. The effects of this transaction are already shown in the unadjusted trial balance. On 12/31/14, | |||||||||

| ABC reissued these 7,000 shares of treasury stock at $10 per share. Record the journal entry required for the reissuance of the treasury stock. | |||||||||

| 9 | On 12/31/14, ABC issued 5,000 shares of $3 par value common stock at the closing market price of $7 per share. Prepare ABC's journal entry | ||||||||

| to reflect the issuance of the stock on 12/31/14. | |||||||||

| 10 | On 7/1/14, ABC sold 12% bonds having a maturity value of $800,000 for $861,771, resulting in an effective yield of 10%. The bonds are | ||||||||

| dated 7/1/14, and mature 7/1/19. Interest is payable semiannually on July 1 and January 1. ABC uses the effective interest method of | |||||||||

| amortization for bond premium or discount. Record the adjusting entry for the accrual of interest and the related amortization on 12/31/14. | |||||||||

| Hint: Develop an abbreviated amortization schedule to accurately determine the interest expense. | |||||||||

| 11 | The following information is available for ABC Corporation at 12/31/14 regarding its investments in stocks of other companies. | ||||||||

| Securities | Cost | Fair Value | |||||||

| 2,200 shares of Toyota Corporation Common Stock | $ 100,000 | $ 125,000 | |||||||

| 1,100 shares of G.M. Corporation Common Stock | $ 67,000 | $ 34,000 | |||||||

| $ 167,000 | $ 159,000 | ||||||||

| Prepare the adjusting entry (if any) for 2014, assuming the securities are classified as trading. | |||||||||

| 12 | On 1/1/14, ABC Corporation purchased, as a held-to-maturity investment, $200,000 of the 8%, 5-year bonds of Intuit Corporation for $177,824, | ||||||||

| which provides an 11% return. Prepare ABC's 12/31/14 journal entry to reflect the receipt of annual interest and discount amortization. | |||||||||

| Assume the bond investment pays interest annually on 12/31 each year and that effective interest amortization is used. | |||||||||

| Note: Notice that a discount account is not used for this investment. Therefore, for purposes of this adjusting entry, amortize the discount directly to the | |||||||||

| investment account. | |||||||||

| 13 | ABC Corporation prepares an aging schedule on 12/31/14 that estimates total uncollectible accounts at $25,000. Assuming that the allowance method is used, | ||||||||

| prepare the entry to record bad debt expense. | |||||||||

| 14 | On 1/1/14, ABC Corporation signed a 5-year noncancelable lease for a delivery vehicle. The terms of the lease called for ABC to Corporation to make | ||||||||

| annual payments of $10,503 at the beginning of each year, starting January 1, 2014. The delivery vehicle has an estimated useful life of 6 years and a $7,000 | |||||||||

| unguaranteed residual value. The delivery vehicle reverts back to the lessor at the end of the lease term. ABC Corporation uses the straight-line method | |||||||||

| of depreciation for the delivery vehicle. ABC Corporation's incremental borrowing rate is 10%, and the Lessor's implicit rate is unknown. No entries have yet | |||||||||

| been made concerning this lease arrangement. After determining the type of lease arrangement (capital or operating), prepare the necessary multiple-part journal | |||||||||

| entry for 2014 for ABC Corporation. (Hints: You will need to compute the present value of the minimum lease payments and 4 separate sub-entries for | |||||||||

| this lease transaction. Also, for Statement of Cash Flow purposes, the principal portion of lease payments are correctly categorized as a financing activity.) | |||||||||

| 15 | ABC Corporation provides a defined benefit pension plan for its employees. A combination adjusting entry should be made to correctly account for this type of pension | ||||||||

| plan given the following items of information for the 2014 plan year, including the recording of pension expense and the employer's contribution to the pension plan in 2014. | |||||||||

| Note: Use the summary entry method as demonstrated and discussed in the chapter lectures on pension accounting to prepare the adjusting entry. | |||||||||

| Pension asset/liability (January 1) | $0 | ||||||||

| Actual return on plan assets | $40,000 | ||||||||

| Expected return on plan assets | $20,000 | ||||||||

| Contributions (funding) in 2014 | $37,000 | ||||||||

| Fair value of plan assets (December 31) | $75,000 | ||||||||

| Settlement rate | 10% | ||||||||

| Projected benefit obligation (January 1) | $0 | ||||||||

| Service cost | $60,000 | ||||||||

| Benefits paid in 2014 | $0 | ||||||||

| *For purposes of financial statement presentation, consider Pension Expense as an operating item and any resulting Pension Asset/Liability as long-term in nature. | |||||||||

| 16 | On December 31, 2014, ABC Corporation issued 1,000 shares of restricted stock to its Chief Financial Officer. ABC stock had a fair value (closing market price) of | ||||||||

| $10 per share on December 31, 2014. Additional information is as follows: | |||||||||

| a. The service period related to the restricted stock is 2 years. | |||||||||

| b. Vesting occurs if the CFO stays with the company for a two-year period. | |||||||||

| c. The par value of the common stock is $3 per share. | |||||||||

| Make the appropriate accounting entry as of the grant date, 12/31/14. Note: use the alternative method as described in your textbook for deferred compensation. | |||||||||

| Do this step after preparing the Income Statement except for the Income taxes line: (You need to calculate Income Before Income Taxes in order to calcualte total Income Tax Expense) | |||||||||

| 17 | Corporate taxes are due in four estimated quarterly payments on April 15, June 15, September 15, and December 15. | ||||||||

| However, for the purposes of this ABC illustration, we will assume that estimates are not paid, and that the tax is paid in full | |||||||||

| on the return's March 15, 2015 due date. | |||||||||

| ABC's income tax rate is 40%. The entire year's income tax expense was estimated at the beginning of 2014 to be $69,600, | |||||||||

| so January through November income tax expense recognized amounts to $63,800 (11/12 months). | |||||||||

| Since we are assuming estimates are not made during the year, the balance in Income taxes payable represents | |||||||||

| tax accrued for January through November. Assume no deferred tax assets or deferred tax liabilities. | |||||||||

| Based on the income before income taxes figure from the income statement, record December's income tax expense | |||||||||

| so that the entire year's total tax expense is correct. | |||||||||