ACCT 2230- Final Exam Guide - Comprehensive Notes for the exam ( 32 pages long!)

29 Mar 2018

School

Department

Course

Professor

Document Summary

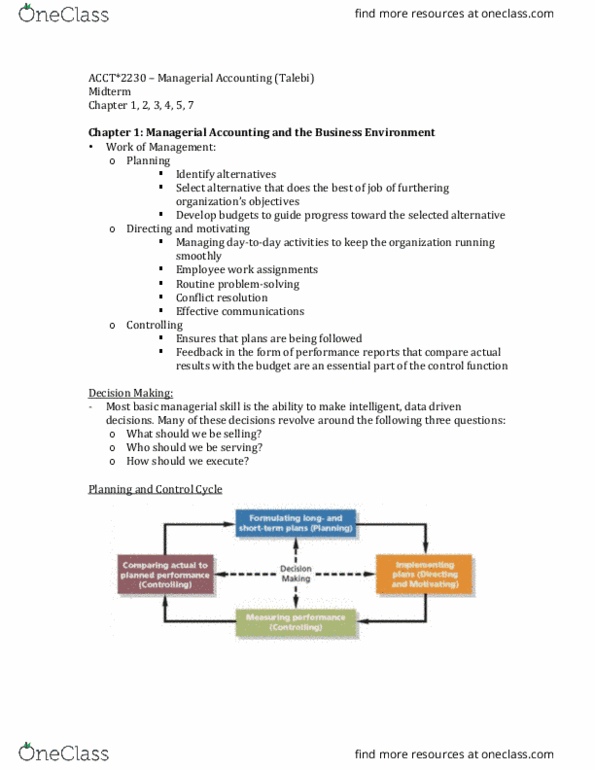

Chapter 1 managerial accounting and the business environment. Every organization has managers who perform several major activities such as: planning. Identify alternatives: select the best job, develop budgets, controlling, ensures that plans are followed, provides performance reports that compares results with the budget, directing and motivating, managing day-to-day activities. Implementing plans (directing and motivating: formulating long and short term plans (planning, measuring performance (controlling, comparing actual to planned performance (controlling) Strategy a game plan that enables a company to attract customer needs by distinguishing itself from competitors. Customer intimacy strategy understand and respond to individual customer needs. Operational excellence strategy deliver products and services faster, more conveniently, and at lower prices. Product leadership strategy offer higher quality products. Managerial accounting: mangers who plan and control and organization, focuses on the future, emphasis on relevance, emphasis on timelines, focus on segment groups, not bound by gaap/aspe/ifrs, not mandatory for extremal reports.