AFM351 Study Guide - Final Guide: Financial Statement, Audit Risk, Audit Evidence

15 Jul 2018

School

Department

Course

Professor

Document Summary

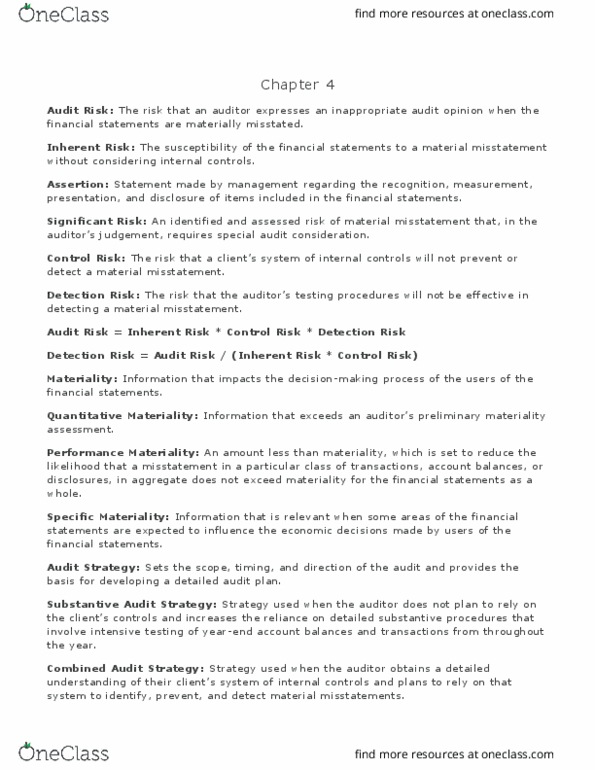

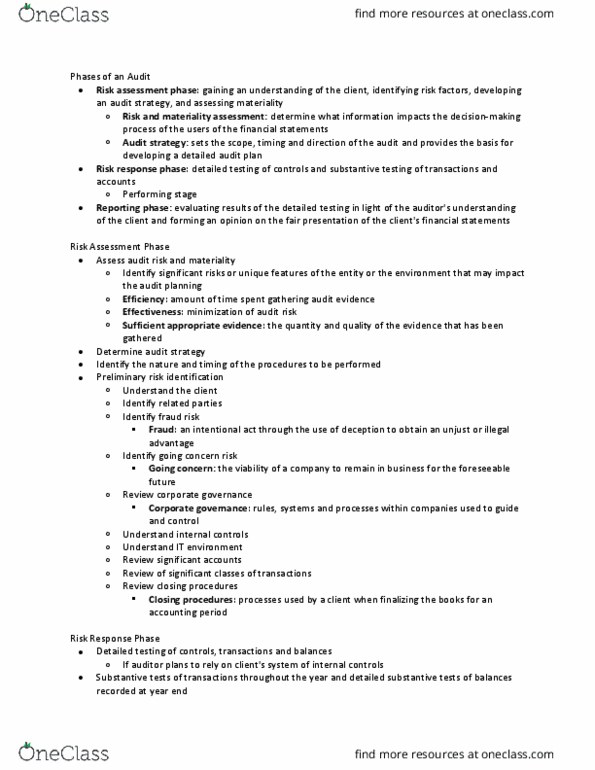

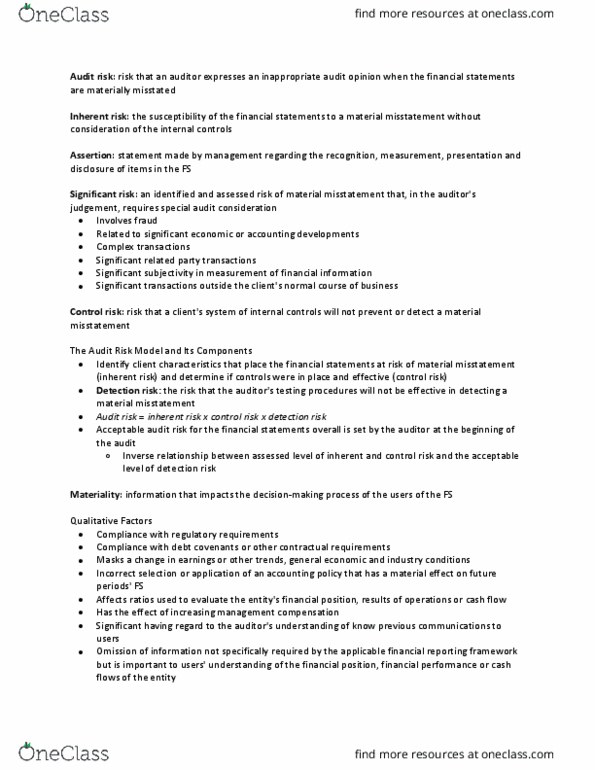

Setting materiality (5th step in planning stage of audit process) The concept of materiality recognizes that transactions, amounts, or certain types of errors, either individually or in the aggregate, directly influence the relevance and reliability of information for decision-making purposes. Planning - determine balances/transactions to focus procedures on; assist in deciding which audit procedures to perform. Execution - evaluate errors and determine extent of additional audit procedures required. Reporting - evaluate aggregate of uncorrected errors that"ve been identified throughout audit. If errors > overall materiality or specific materiality and client will not correct, opinion may be affected. Professional judgement is required as both quantitative and qualitative factors need to be taken into consideration. Step 1: identify the users of the financial statements. Try to come up with at least two for each user. Cas 320 materiality in planning and performing an audit does not provide specific guidance on which bases should be chosen; the practitioner must use professional judgment.