COMM101 Study Guide - Stakeholder Management, Double Taxation, Universal Health Care

9 Dec 2013

School

Department

Course

Professor

Document Summary

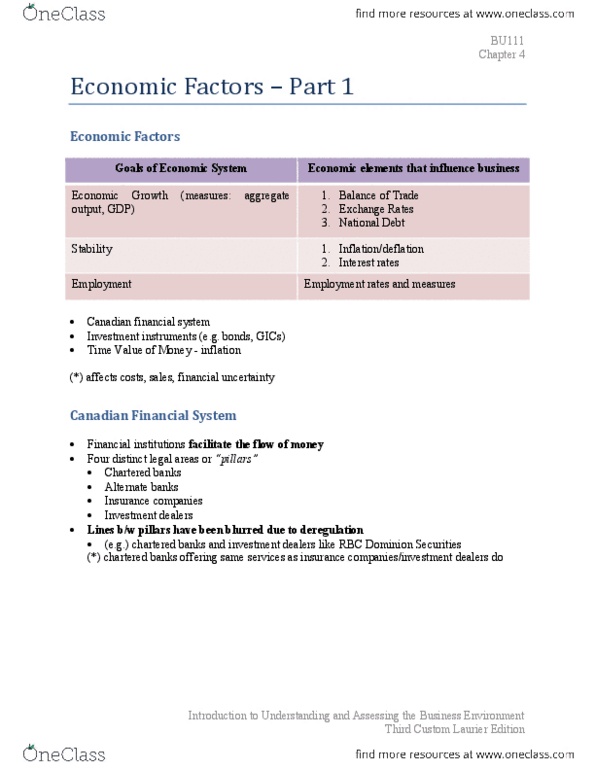

Financial system: financial ins)tu)ons facilitate ow of money. Montreal) - publicly traded, pro t seeking companies. Largest and most important ins)tu)on. Concentrated and highly regulated industry. Five largest account for 90% of total bank assets. Determines what banks can or cannot do) roles/functions. Serve individuals, business, and others. Major source of short- term loans for business. Secured loans: when you go to the bank and take out the loan, you give them the right to sell your personal belongings if you do not pay them back lower interest than unsecured. Unsecured loans: backed only by the borrower"s promise to repay it. Only the most credit- worthy borrowers can get unsecured loans. Trust companies & credit unions. A trust company safeguards property (funds and estates) entrusted to it. It may also serve as trustee, transfer agent, and registrar for corpora)ons and provide other services. Expand money supply through deposit expansion. Smaller versions of banks.