ECON 101 Study Guide - Quiz Guide: Opportunity Cost, Marginal Revenue, Market Power

78

ECON 101 Full Course Notes

Verified Note

78 documents

Document Summary

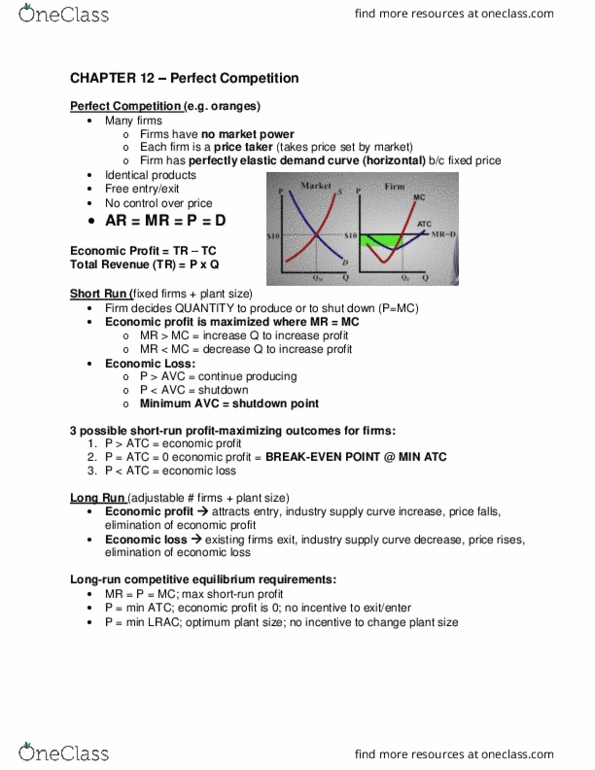

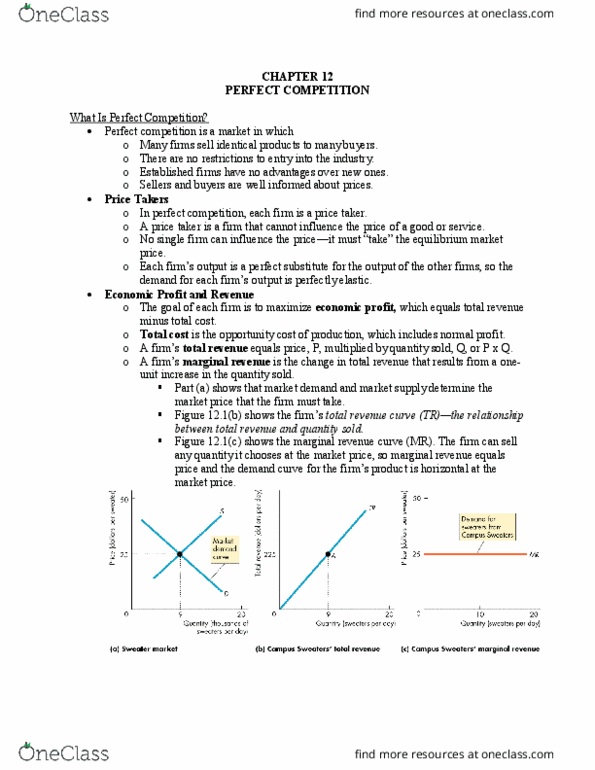

Minimum efficient scale: the smallest quantity of output at which the long run average cost reaches its lowest level. By the law of demand: if the firm sells more (q increases), then the price goes down (p goes down) In perfect competition, each firm is a price taker. A price taker is a firm that can"t influence the market price of a good or service. If they sell the same product, then they are price takers, because they take each other. The goal of each firm is to maximize economic profit. Total cost is he opportunity cost of production, which includes normal profit. A firm"s total revenue equals price, p, multiplied by quantity sold, q, or p x q. A firm"s marginal revenue is the change in total price. The firm"s total revenue curve (tr) = the relationship between total revenue and quantity sold.