MGT223H5 Study Guide - Midterm Guide: Enterprise Risk Management, Six Sigma, Dmaic

Document Summary

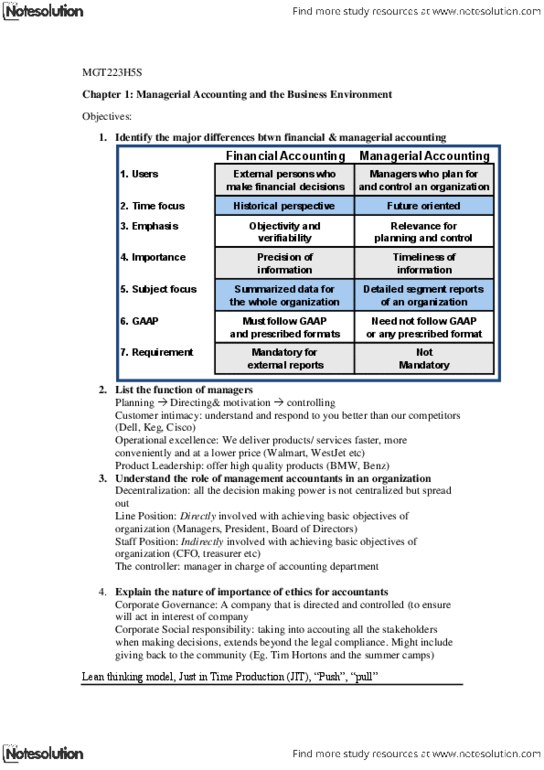

Chapter 1: managerial accounting and the business environment. Functions of managers: planning, directing & motivating, controlling. Financial accounting: follows gaap, limited set of documents, for external use by stakeholders of a company. Managerial accounting: does not follow gaap, for internal use by managers to assist in planning, controlling and for decision-making. Role of management accountants: delegation, line & staff relationships, controller. Lean production: 5-step, pulls units through in response to customer orders. Six sigma: process improvement method, relies on customer feedback and fact-based gathering and analysis techniques to drive process improvement. Risk management: process used by a company to proactively identify and manage risks. Managerial accounting phase of accounting concerned with providing info to managers for use in planning and controlling operations and for decision- making. Managers who plan for and control an organization. Detailed segment reports about departments, products, customers and employees are prepared. Need not follow gaap or any prescribed format.