MGM101H5 Study Guide - Cash Flow Statement, Financial Statement, Financial Accounting

25

MGM101H5 Full Course Notes

Verified Note

25 documents

Document Summary

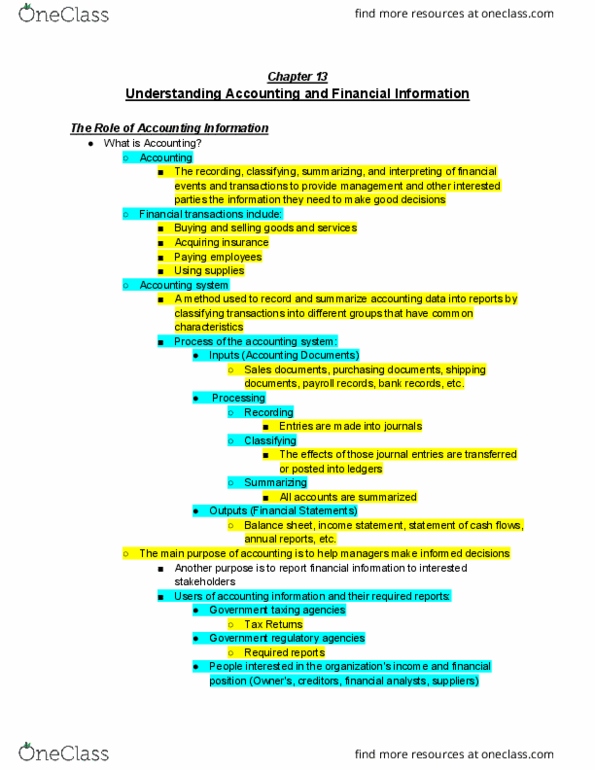

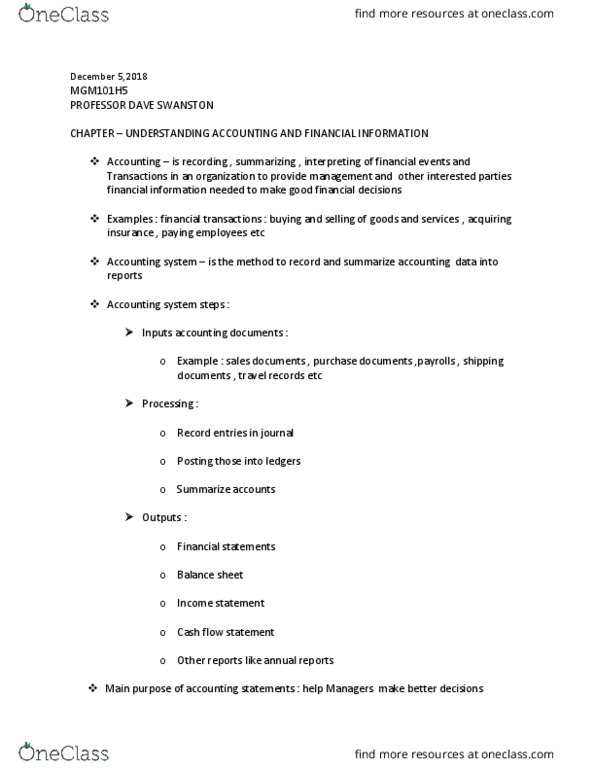

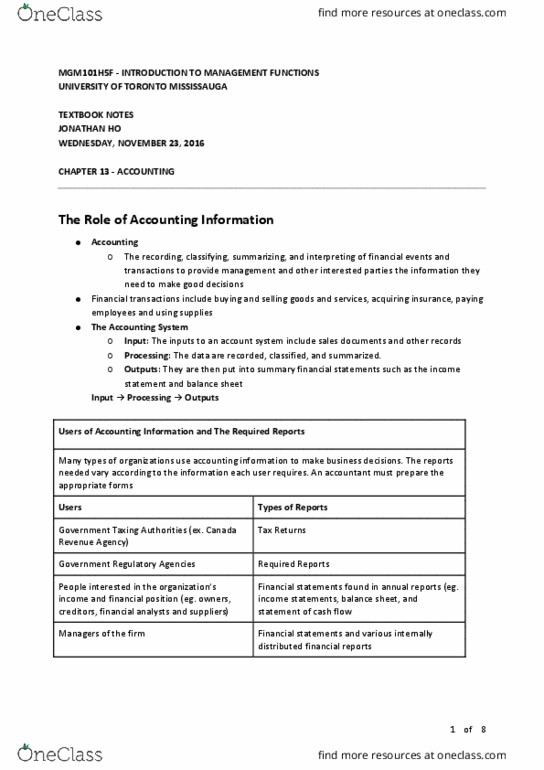

Textbook notes chapter 8- understanding accounting and financial. Financial information: financial information is the heartbeat of competitive businesses and accounting information keeps the heartbeat stable. Impossible to run a business without being able to read, understand, and analyze accounting reports and financial statements. Help managers evaluate the financial condition and the operating performance of the firm so that they can make well informed decisions. Report financial information to people outside the firm (owners, creditors, suppliers) Areas of accounting: accounting profession is divided into five key working areas, all of which are important and create career opportunities. Compared with plans to see if the results are achieving the targets set for the period. Compared with those of the particular industry to see that they are in line with, or better than, the results in competing firms. Trends of resents are examined to ensure that good trends are continued and unfavourable ones are reversed.