MGT220H5 Study Guide - Midterm Guide: Effective Interest Rate, Gross Profit, Accounts Receivable

13 May 2017

School

Department

Course

Professor

Document Summary

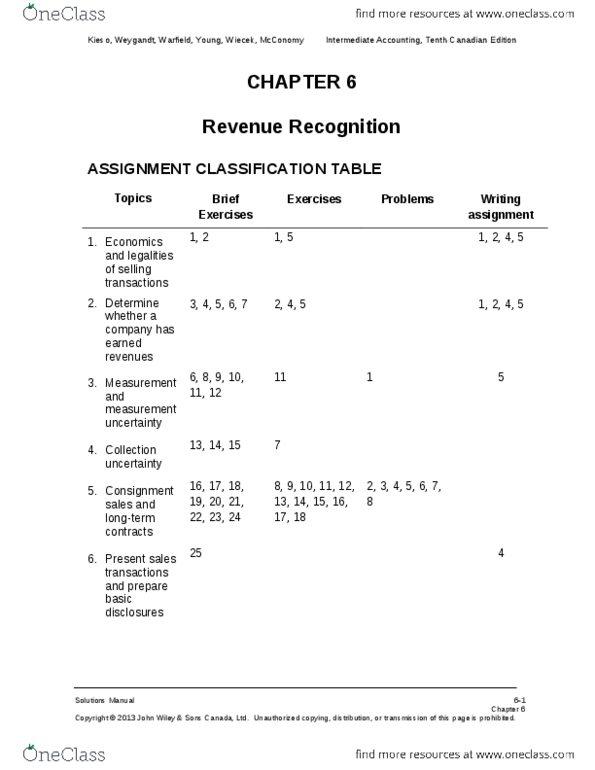

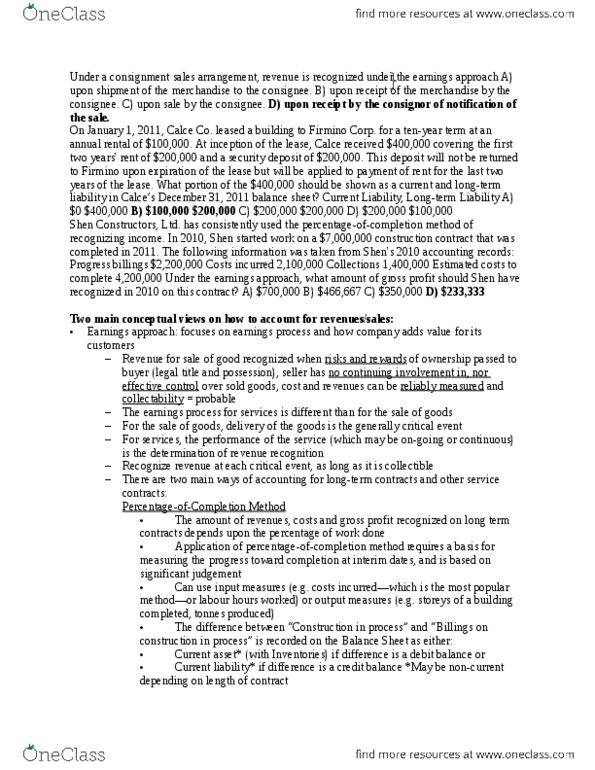

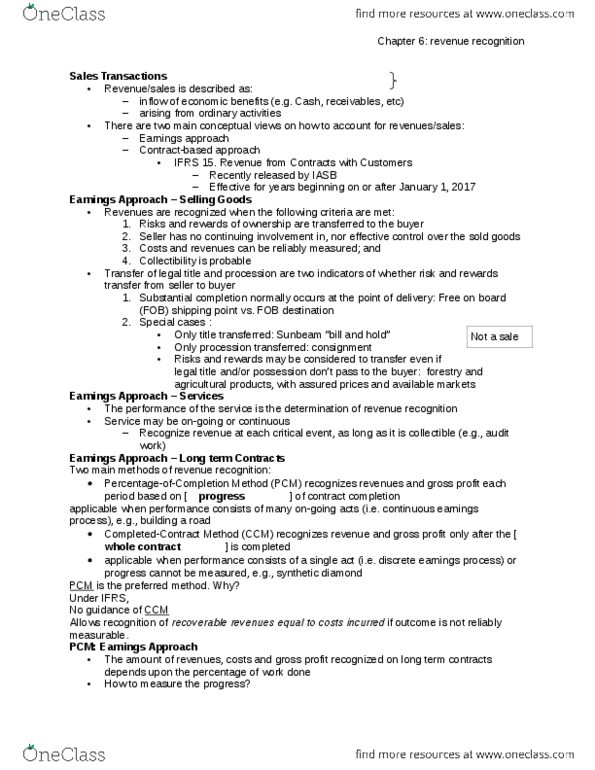

Example of gross method: ,000 sales on credit (terms 2/10, n/30) 10,000: customer pays account within discount period. Example of net method: ,000 sales on credit (terms 2/10, n/30) 9,800: customer pays account after discount period. Mix of procedures: example: dockrill corp. reports the following balances for its first year of operations (2014): ,000: the company estimates bad debts at 2% of net credit sales, determine estimated bad debts expense for 2014. Balance sheet presentation: short-term accounts receivable are shown at their net realizable value as follows: Allowance method: writing off accounts receivable: when a specific customer"s account is determined to be uncollectible, the following entry is made: Accounts receivable(cid:367)specific customer x (for the amount to be written off) If payment is received after write-off of account, the account is reinstated and payment is recorded: If uncollectible amounts are highly immaterial, the allowance method is not required: record bad debt expense only when specific account is determined to be.