ECO101H1 Study Guide - Quiz Guide: Sunk Costs, Marginal Product, Marginal Cost

98

ECO101H1 Full Course Notes

Verified Note

98 documents

Document Summary

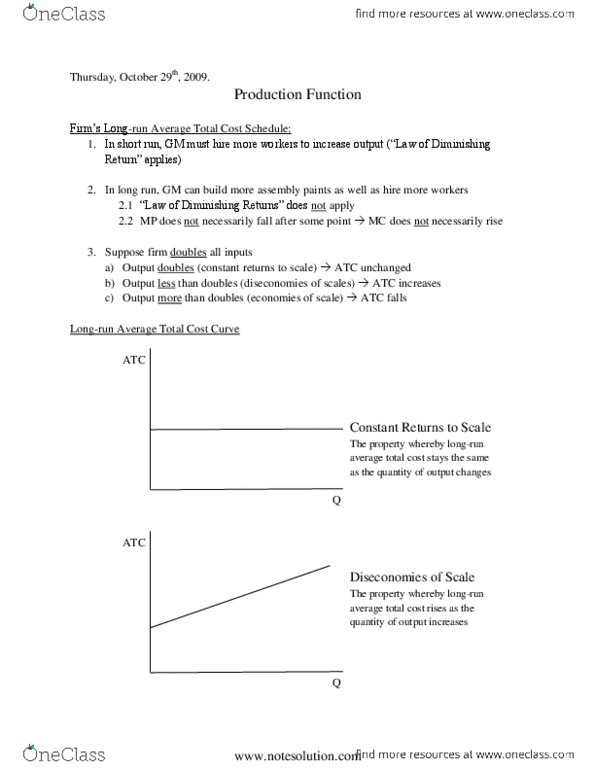

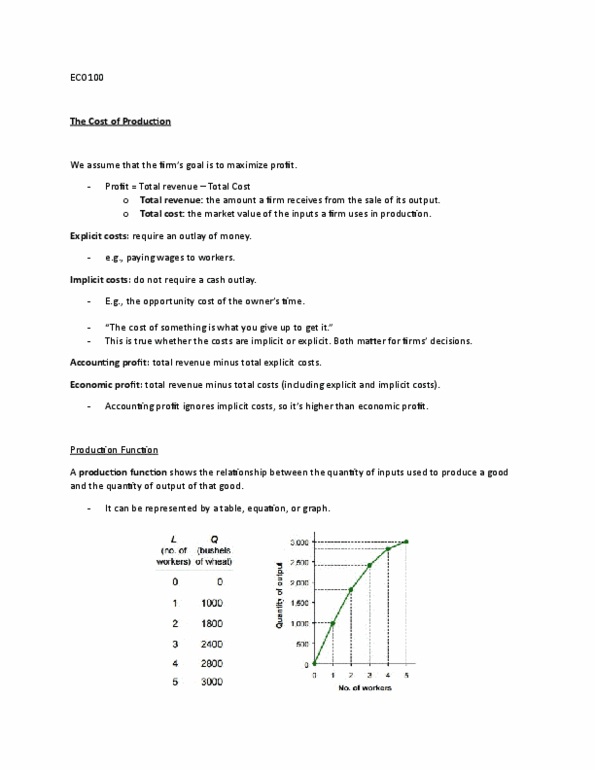

Explicit costs- input costs that require an outlay of money by the firm. Implicit costs- input costs that do not require an outlay of money by the firm. Economic profit- total revenue minus total cost, including both explicit and implicit costs. Accounting profit- total revenue minus total explicit cost. Production function- the relationship between quantity of inputs used to make a good and the quantity of output of that good. Marginal product- the increase in output that arises from an additional unit of input. Diminishing marginal product- the property whereby the marginal product of an input declines as the quantity of the input increases. Efficient scale- the quantity of output that minimizes average total cost (global min of atc) Economies of scale- the property whereby long-run average total cost falls as the quantity of output increases. Diseconomies of scale- the property whereby long-run average total cost rises as the quantity of output increases.