BUS-2003 Study Guide - Final Guide: Earnings Before Interest And Taxes, Transfer Pricing, Fixed Cost

6 Oct 2011

School

Department

Course

Professor

Document Summary

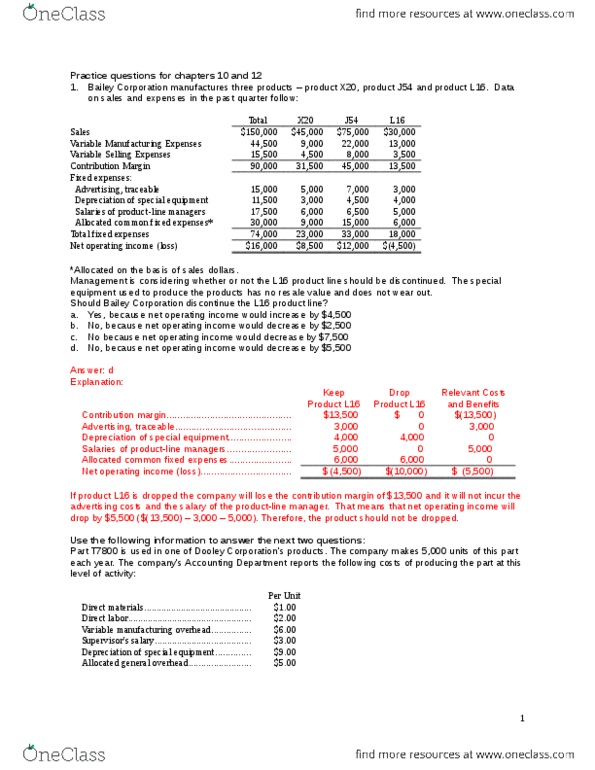

These questions are representative of the types of questions you may find on the final exam, but in total are longer than the actual final exam. Bellow division of sound corporation is currently operating at a loss. Bellow makes radios that are sold to retail stores. The senior management of sound corporation is considering closing the. Bellow"s statement of operations for the last year follows: Recently, sound corporation acquired the boom speaker company which manufactures speakers that are sold to radio manufacturers. In an effort to save the division from closing, the manager of the bellow division has asked that the new boom speaker division supply it with 80,000 speakers. The bellow division currently purchases the speakers from outside suppliers for each. Boom speaker produces and externally sells 400,000 speakers per year which represents 80% of its operating capacity. At this production level the standard cost to produce one speaker is as follows: