ACCT-240 Study Guide - Midterm Guide: Gross Profit, Inventory Turnover, Net Income

31 Oct 2016

School

Department

Course

Professor

Document Summary

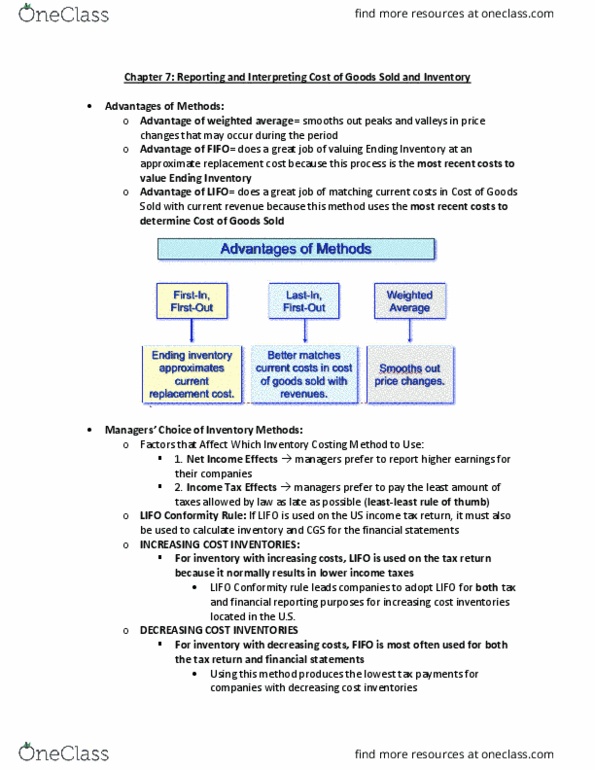

Two kinds : tangible: bland, property, natural resources. Cost of goods sold (cgs) = beginning inventory (bi) + purchase (p) - ending inventory (ei) When costs are increasing, effects of different methods are follows - When costs are decreasing, effects of different methods are follows - Inventory costs > lifo on tax return < income tax. Inventory costs < fifo on tax return & financial statement < income tax. In such circumstances, the fifo method, in which the oldest, most expensive goods become cost of goods sold, produces the highest cost of goods sold, the lowest pretax earnings, and thus the lowest income tax liability. Manufacturing company (a) raw material (b) work-in-process inventory (c) finished goods inventory. Service companies: (a) services to the end users. Ending inventory (inventory sold) (expense in the income statement) Cost of goods sold (inventory not sold) (asset in the balance sheet) Perpetual inventory system : the inventory account is updated for each transaction.