EC 201 Study Guide - Midterm Guide: Demand Curve, Tax Incidence, Price Ceiling

Document Summary

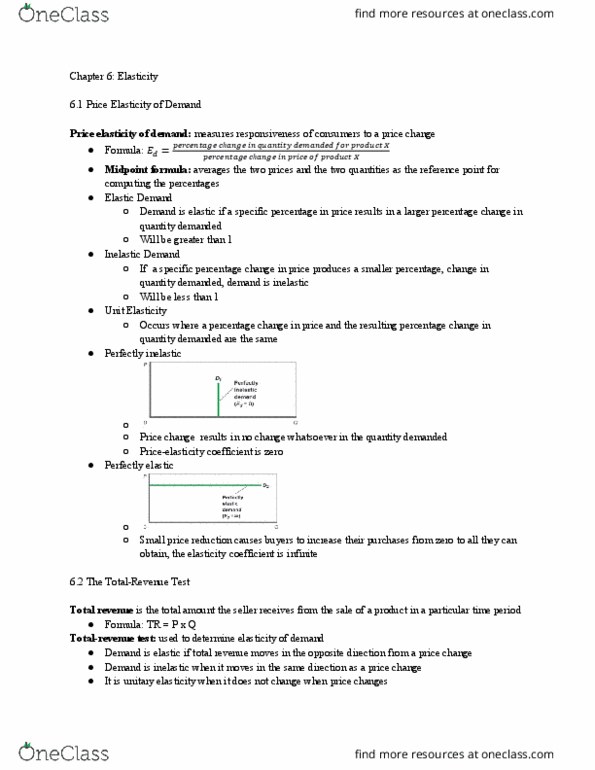

Elasticity is a measure of the responsiveness of quantity demanded or quantity supplied to a change in one of its determinants. Demand for a good is said to be elastic if the quantity demanded responds substantially to changes in the price. Demand is said to be inelastic if the quantity demanded responds only slightly to changes in the price. The price elasticity of demand for any good measures how willing consumers are to buy less of the good as its price rises. Necessities tend to have inelastic demands, whereas luxuries have elastic demands. Goods tend to have more elastic demand over longer time horizons. Price elasticity of demand = percentage change in quantity demanded/ percentage change in price. Demand = elastic when elasticity is greater than 1. Demand = inelastic when elasticity is less than 1. If elasticity is exactly 1, the percentage change in quantity equals the percentage change in price, and demand is said to have unit elasticity.