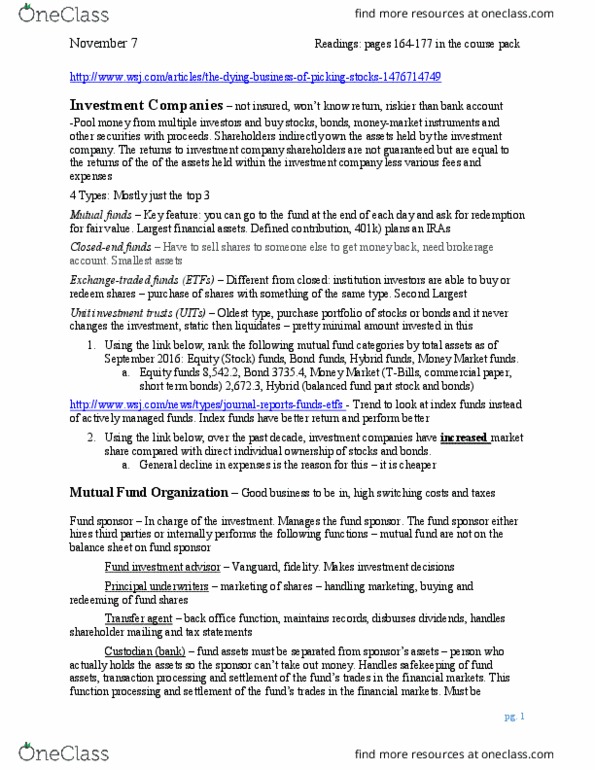

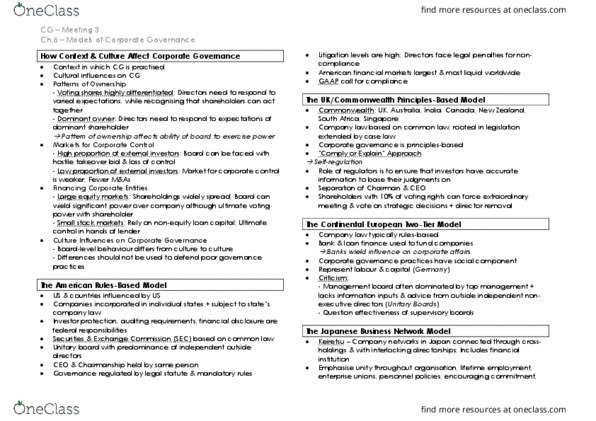

FI 413 Study Guide - Final Guide: Financial Institution, Customer Satisfaction, Form 10-Q

Document Summary

Get access

Related Documents

Related Questions

The Stone Meat Corporation is a mediumâsized agricultural products company headquartered in Ogden, Utah. Its primary products are beef, pork and poultry and include packaged deli meats to half animals sold directly to in-store butcher markets in the retail grocery stores. They also supply their own butcher packs to various retail outlets including grocery stores, big box stores, and restaurants. In addition, they have their own factory store. The firm's products are well recognized within the markets in terms of quality and food safety. During the 2000's and the early 2010's sales and earnings had grown rapidly. Sales in 2002 were approximately $60 million, but had reached $180 million by 2012. Per share earnings and dividends more than kept pace. The relevant figures are contained in Exhibit 1. In order to support the firm's expansion, substantial expenditures on plant and equipment were required during the period indicated. The majority of funds came from retained earnings and the private placement of debentures with insurance companies. In 2004, however, the company was forced to sell additional common stock because it felt that the debt level, which would ensue from trying to borrow the money to keep up its expansion program, would be excessive. In particular, possible adverse effects in its stock price were feared since, at the time, the firm's ratio of debt to total capitalization was already somewhat above the industry average of 30 percent. The firm's balance sheet as of December 31, 2012 is shown in Exhibit 1. Originally, the company's Board of Directors had established a policy of paying out half its annual earnings as dividends. The actual percentage varied from year to year because an attempt was made to stabilize the dividends despite fluctuating profit. By the late 2000's, this policy had been revised to set oneâthird of earnings as the target payâout ratio due to the continuing need for capital. At their last annual meeting, the Directors announced that the 2012 dividend would be 60 cents per share, payable quarterly in 15 cent installments. The company's stock is listed on the AMEX and trades actively. The range of yearly stock prices is included in Exhibit 1. The closing price on June 30, 2012 was $24. Market data indicated that Stone was somewhat less risky than the market as a whole with a beta of .80. Returns on the market were averaging approximately 12% and risk free borrowing was still low following the financial meltdown of 2008. These rates averaged 3.5%. Preferred stock, which had been issued many years ago as a part of a financial deal, was selling at $90 per share. Tax rates had averaged 30% over the last few years. Early in 2012, the treasurer of Stone was reviewing its investment and financing strategies with an eye toward improving both. The question as to an appropriate cutâoff ratio of return on new investments was of special concern. The treasurer was of the opinion that many capital expenditures had been made in the past without proper analysis. He wanted a figure he could justify to the firm's managers as a cost of capital in order to achieve a more accurate capital budgeting procedure throughout the organization. He felt this was an especially timely move in view of an article he had just read in the WSJ and which is reproduced in Exhibit Ill. Stone's own longârange planning group had earlier forecast a trend not unlike that indicated in the Journal. The treasurer was well aware that financing did not come free and that the costs of issuance of preferred stock would cost 8%, bonds would cost 4% and equity 12%. He thought it important to determine how such costs would inflate the costs of any proposed projects the company might pursue in the futures. Thus he wanted to determine what the total cost of a $1,000,000 investment would be after considering any financing costs

Exhibit 1

Year Sales eps dps Stock Price

|

|

|

|

| |||||||||||||||||||||||||||||||||||||||||||||||||||||||

Exhibit II

Balance Sheet As of 12/31/2012 (figures in Millions)

Cash 20 Accounts Receivable 10 Inventories 30 Plant and Equipment, net 60 Total Assets 120 Accounts Payable 20 Misc Accruals 10 Preferred Stock (5%) 10 Long term Debt 24 Common Stock (2.5 million shares) 12 Capital Surplus 4 Retained Earnings 40 Total Liabilities and Equity 120 The firm's bonds carried a 6% coupon, a 12/31/2022 maturity and were selling for $960 as of 6/30/2012.

What is the cost of preferred stock?

I need help find the Weighted Average Cost of Capital as well as the Weighted Average Flotation Costs

COST OF CAPITAL EXERCISE

The Stone Meat Corporation is a mediumâsized agricultural products company headquartered in Ogden, Utah. Its primary products are beef, pork and poultry and include packaged deli meats to half animals sold directly to in-store butcher markets in the retail grocery stores. They also supply their own butcher packs to various retail outlets including grocery stores, big box stores, and restaurants. In addition, they have their own factory store. The firm's products are well recognized within the markets in terms of quality and food safety.

During the 2000's and the early 2010's sales and earnings had grown rapidly. Sales in 2002 were approximately $60 million, but had reached $180 million by 2012. Per share earnings and dividends more than kept pace. The relevant figures are contained in Exhibit 1.

In order to support the firm's expansion, substantial expenditures on plant and equipment were required during the period indicated. The majority of funds came from retained earnings and the private placement of debentures with insurance companies. In 2004, however, the company was forced to sell additional common stock because it felt that the debt level, which would ensue from trying to borrow the money to keep up its expansion program, would be excessive. In particular, possible adverse effects in its stock price were feared since, at the time, the firm's ratio of debt to total capitalization was already somewhat above the industry average of 30 percent. The firm's balance sheet as of December 31, 2012 is shown in Exhibit 1.

Originally, the company's Board of Directors had established a policy of paying out half its annual earnings as dividends. The actual percentage varied from year to year because an attempt was made to stabilize the dividends despite fluctuating profit. By the late 2000's, this policy had been revised to set oneâthird of earnings as the target payâout ratio due to the continuing need for capital. At their last annual meeting, the Directors announced that the 2012 dividend would be 60 cents per share, payable quarterly in 15 cent installments. The company's stock is listed on the AMEX and trades actively. The range of yearly stock prices is included in Exhibit 1. The closing price on June 30, 2012 was $24.

Market data indicated that Stone was somewhat less risky than the market as a whole with a beta of .80. Returns on the market were averaging approximately 12% and risk free borrowing was still low following the financial meltdown of 2008. These rates averaged 3.5%. Preferred stock, which had been issued many years ago as a part of a financial deal, was selling at $90 per share. Tax rates had averaged 30% over the last few years.

Early in 2012, the treasurer of Stone was reviewing its investment and financing strategies with an eye toward improving both. The question as to an appropriate cutâoff ratio of return on new investments was of special concern. The treasurer was of the opinion that many capital expenditures had been made in the past without proper analysis. He wanted a figure he could justify to the firm's managers as a cost of capital in order to achieve a more accurate capital budgeting procedure throughout the organization. He felt this was an especially timely move in view of an article he had just read in the WSJ and which is reproduced in Exhibit Ill. Stone's own longârange planning group had earlier forecast a trend not unlike that indicated in the Journal.

The treasurer was well aware that financing did not come free and that the costs of issuance of preferred stock would cost 8%, bonds would cost 4% and equity 12%. He thought it important to determine how such costs would inflate the costs of any proposed projects the company might pursue in the futures. Thus he wanted to determine what the total cost of a $1,000,000 investment would be after considering any financing costs.

| Year | Sales in MillionsOf Dollars | EPS | DPS | Stock Price Range |

| 2002 | 60 | 0.560 | 0.30 | 6-10 |

| 2003 | 63 | 0.500 | 0.30 | 5-9 |

| 2004 | 68 | 0.710 | 0.35 | 5-10 |

| 2005 | 85 | 0.880 | 0.40 | 8-12 |

| 2006 | 97 | 0.820 | 0.45 | 9-14 |

| 2007 | 119 | 0.940 | 0.45 | 12-20 |

| 2008 | 130 | 1.110 | 0.45 | 11-18 |

| 2009 | 145 | 1.350 | 0.45 | 15-24 |

| 2010 | 164 | 1.300 | 0.50 | 17-27 |

| 2011 | 173 | 1.600 | 0.50 | 20-30 |

| 2012 | 180 | 1.750 | 0.60 | 24-32 |

| Exhibit II | |

| Balance Sheet As of 12/31/2012 (figures in millions) | |

| Cash | 20 |

| Accounts Receivable | 10 |

| Inventories | 30 |

| Plant and Equipment, net | 60 |

| Total Assets | 120 |

| Accounts Payable | 20 |

| Misc Accruals | 10 |

| Preferred Stock (5%) | 10 |

| Long term Debt | 24 |

| Common Stock (2.5 million shares) | 12 |

| Capital Surplus | 4 |

| Retained Earnings | 40 |

| Total Liabilities and Equity | 120 |

| The firm's bonds carried a 6% coupon, (paid semi- | |

| annually) a 12/31/2022 maturity and were selling for | |

| $960 as of 6/30/2012. | |

EXHIBIT III

Article taken form the February 7, 2012 issue of the Wall Street Journal.

Meat Processing Industry To Be Hurt by Increasing Prices?

Decimated Life stock Herds Also Contribute to Price Increases.

Kansas (AP) â The ConAgra Corporation, in a recent annual meeting announcement, forecast a trailing off of sales in its meat processing division. That division, which had been growing at a rate equivalent to three times the CPI growth rate throughout the 2000's and early 2010's, may be hit by decreases in household expenditures as the effects of the most recent financial crisis are still lingering for the decimated middle class. Retail outlets such as restaurants and grocery stores are reporting that sales of beef and pork products are declining in response to price pressures. Disease that swept through beef and pork herds, are also having a telling effect. Other sources close to the industry confirm the ConAgra prognosis. They estimate the best forecasts that their economists can come up with indicate a decline of about five percent in the growth rate which had been experienced in the last 12 to 15 years. ConAgra is curtailing several plant expansions in its meat processing division which were on the drawing board for the midâ2010's." We are moderately pessimistic," a company spokesman indicated, "and are going to adopt a wait and see attitude for the next year or so."

Hints

Create the Cost of Capital

Number of shares can be determined by taking the book value and dividing by the par value of the securities.

Market value is shares X price.

Average the two possible ways to calculate the cost of equity

Remember the tax rate.

Assume the bonds are semi - annual

The term to maturity is from 6/30/2012 to 12/31/2022 or 10.5 years. This info is in the footnote to Exhibit II

The growth rate should be determined from the EPS data and the adjustment to the growth rate is in Exhibit III

Create the Weighted Average Flotation Cost

What is the cost of equity using the dividend growth model? (Decimal answer to the fourth decimal place)

Given the $1,000,000 cost of the investment, what is the total cost of the investment including flotation costs? (Round to whole numbers)

You recently graduated from Suffolk University, and your job search led you to J&J Bagel, Inc. As you are finishing your employment paperwork, Jerry Chen, one of the co-owners of J&J Bagel, informs you about the companyâs new 401(k) plan. A 401(k) is a type of retirement plan, offered by many companies.

A 401(k) is tax deferred, which means that any deposits you make into the plan are deducted from your current income, so no current taxes are paid on these deposits. For example, if your annual salary is $30,000 and you contribute $1,500 to the 401(k) plan, you will pay taxes only on the $28,500 in income. No taxes will be due on any capital gains or plan income while you are invested in the plan, but you will pay taxes when you withdraw the money at retirement. You can contribute up to 15 percent of your salary to the plan. As is common, J&J Bagel has a 5 percent match program. This means that the company will match your contribution dollar-for-dollar up to 5 percent of your salary, but you must contribute to get the match. In other words, if you contribute 5 percent of your $30,000 salary (which is $1,500) towards the 401(k) plan, J&J Bagel will match your contribution by adding another $1,500 to your plan, so that $3,000 in total will be contributed to your 401(k) plan.

The 401(k) plan has several options for investments, most of which are mutual funds. As you know, a mutual fund is a portfolio of assets. When you purchase shares in a mutual fund, you are actually purchasing partial ownership of the fundâs assets, similar to purchasing shares of stock in a company. The return of the fund is the weighted average of the return of the assets owned by the fund, minus expenses. The largest expense is typically the management fee paid to the fund managers, who make all of the investment decisions for the fund. J&J Bagel uses Imperium Financial Services as its 401(k) plan administrator.

Jerry Chen then explains the following retirement investment options available for employees:

Company Stock. One option is stock in J&J Bagel. The company is currently privately held. The price you would pay for the stock is based on an annual appraisal, less a 20 percent discount. When you are interviewed by the owners, John Benson and Jerry Chen, they informed you that the company stock was expected to be publically sold in three to five years. If you needed to sell the stock before it became publicly traded, the company would buy it back at the then-current appraised value.

Imperium S&P 500 Index Fund. This mutual fund tracks the S&P 500 Index. Stocks in the fund are weighted exactly the same as they are in the S&P 500 Index. This means that the fundâs return is approximately the return of the S&P 500 Index, minus expenses. With an index fund, the manager is not required to research stocks and make investment decisions, so fund expenses are usually low. The Imperium S&P 500 Index Fund charges expenses of 0.20 percent of assets per year.1

Imperium Small-Cap Fund. This fund primarily invests in small capitalization stocks. As such, the returns of the fund are more volatile. The fund can also invest 10 percent of its assets in companies based outside of the U.S. This fund charges 1.7 percent of assets in expenses per year.

Imperium Large-Cap Fund. This fund invests primarily in large capitalization stocks of companies based in the U.S. The fund is managed by Jenna King and has outperformed the market in six out of the last eight years. The fund charges 1.5 percent in expenses.

Imperium Bond Fund. This fund invests in long-term corporate bonds issued by U.S. companies. The fund is restricted to investments in bonds with investment grade credit rating. This fund charges 1.4 percent in expenses.

Imperium Money Market Fund. This fund invests in short-term, high credit quality debt instruments, which include Treasury Bills. As such, the return on money market funds is only slightly higher than the return on Treasury Bills. Because of the credit quality and short-term nature of the investments, there is only a very slight risk of negative return. The fund charges 0.60 percent in expenses.

*1 The return on a mutual fund after accounting for management expenses is calculated as follows. If a fund charges 2 percent in expenses and it is expected to yield a 10 percent return before expenses, then the return on this fund after expenses will be (1 + 0.10)Ã(1 â 0.02) â 1 = 0.078 or 7.8 percent*

QUESTIONS

1. advantages/disadvantages do the mutual funds offer compared to company stock for your retirement investing?

2. One can assess investment risk by looking forward to how assets are expected to react to a particular set of circumstances or âstates of economyâ. Use the following set of assumptions for the coming year to compute the expected rates of return (before expenses) and the standard deviations for the mutual funds described above.

| Probability | S&P 500 index fund | Small-cap fund | large-cap fund | Bondfund | moneymarketfund | |

|---|---|---|---|---|---|---|

| Recession | 20% | -12% | -30% | -10% | 18% | 2% |

| Near Recession | 10% | -8% | -20% | -6% | 14% | 3% |

| Normal | 30% | 12% | 22% | 12% | 8% | 4% |

| Near Boom | 20% | 22% | 38% | 15% | -1% | 5% |

| Boom | 20% | 26% | 54% | 20% | -6% | 6% |

3. Given the expected returns calculated for each of the mutual funds above, estimate the betas of these funds. Assume a risk-free rate of 4 percent and the expected market return equal to the expected return on the S&P 500 Index.

4. If you decide to invest your money equally in the Small-Cap and Bond funds, what would your portfolioâs expected return and risk level (standard deviation and beta) be? (Hint: Adjust mutual fund returns for management expenses as explained in footnote 1.

5. What would happen if you were to put 70 percent of your portfolio in the Small-Cap fund and 30 percent in the S&P 500 Index fund? Would this combination be better for you?

6. The returns of the Imperium Small-Cap Fund are the most volatile of all the mutual funds offered in the 401(k) plan. Why would you ever want to invest in this fund? When you examine the expenses of the mutual funds, you will notice that this fund also has the highest expenses. Will this affect your decision to invest in this fund?