ACTG 2300 Midterm: Exam 1 In-Class Review

127 views5 pages

7 Feb 2017

School

Department

Course

Professor

Document Summary

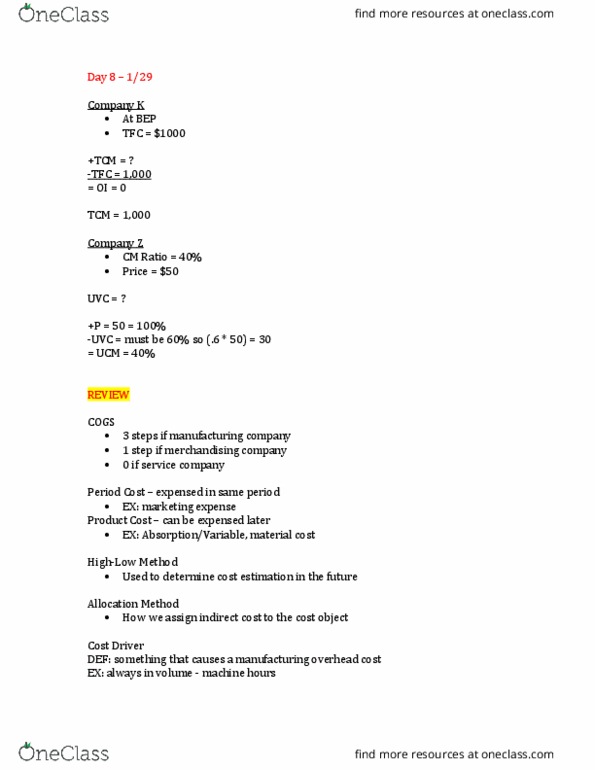

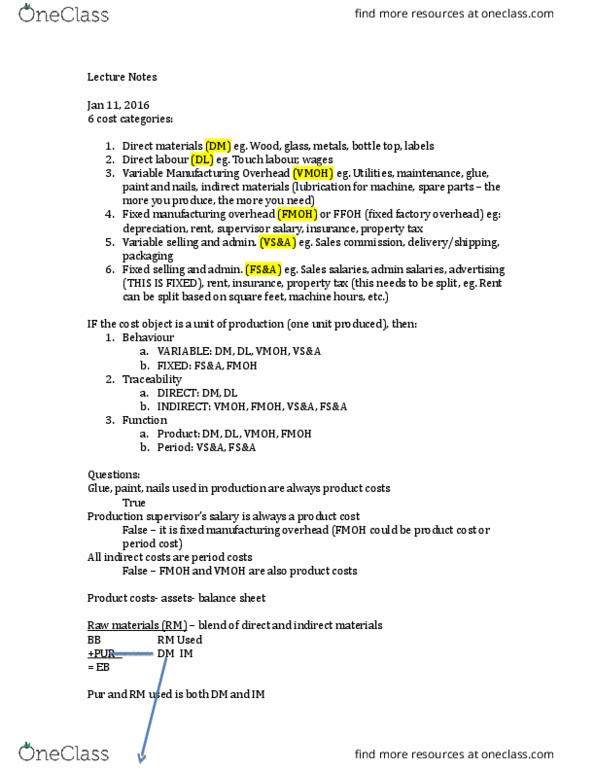

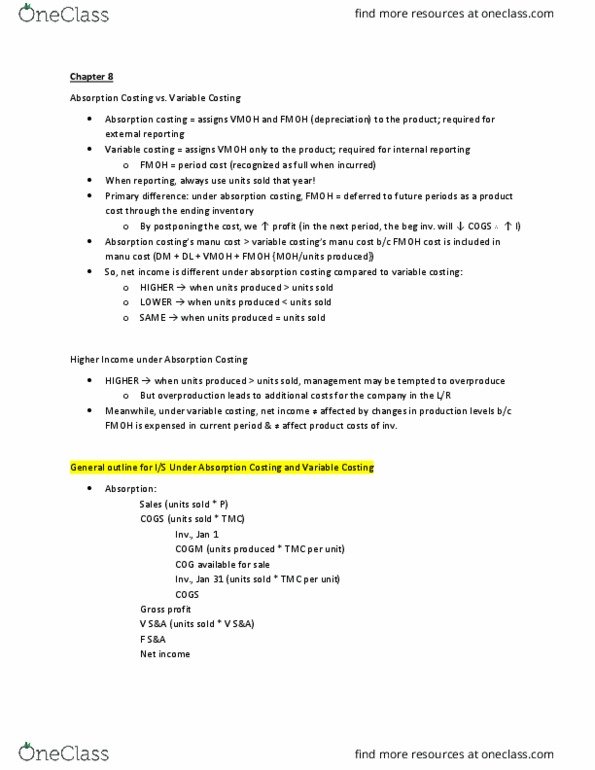

Vmoh = 40: don"t include var s&a. Fmoh = 60,000 / 250 = 240. Variable cost is always avoidable, so it is always relevant. Sunk cost: def: a cost that has already been incurred and does not change. Indirect cost: we can never say whether a cost is direct or indirect if we do not know what the cost object is. If we use the dish, it is indirect. If we use location, the cost can be directly traced. Product cost: def: can be expensed and incurred in different periods can sit in the balance sheet until we incur it. Period cost: def: expensed (reported in the income statement) and incurred in the same period. Use past to estimate the future: if we assume normal conditions in future. Every unit we sell, we incur . 4 in sales. Every unit we sell, we incur . 4 in sales: total cost. S&a and cost of sales fixed costs.

Get access

Grade+20% off

$8 USD/m$10 USD/m

Billed $96 USD annually

Homework Help

Study Guides

Textbook Solutions

Class Notes

Textbook Notes

Booster Class

40 Verified Answers

Related Documents

Related Questions

| FILL IN THE CORRECT TERMINOLOGIES IN THE BLANK SPACES | ||

| _____ 1. | a. A method of internal (managerial accounting) reporting that emphasizes the distinction between variable and fixed costs. | |

| _____ 2. | b. A discounted cash flow approach to capital budgeting that computes the present value of all future cash flows. | |

| _____ 3. | c. Determination of the maximum cost a company can spend to make a product given a set volume, selling price and desired operating profit. | |

| _____ 4. | d. An analysis of the additional costs and benefits of a proposed alternative compared with the current situation. | |

| _____ 5. | e. A historical cost that the company has already incurred which is irrelevant to the decision making process. | |

| _____ 6. | f. Costs that will not continue if an ongoing operation is changed or deleted. | |

| _____ 7. | g. An already owned production site that is not currently in use. | |

| _____ 8. | h. The maximum available benefit foregone by using a resource for a particular purpose. | |

| _____ 9. | i. The predicted future costs and revenues that will differ among alternative courses of action. | |

| _____ 10. | J. The time it will take to recoup, in the form of cash inflows from operations, the initial dollars invested in a project | |

| _____ 11. | k. Those costs of facilities and services that are shared by users | |

| _____ 12. | l. The juncture of manufacturing where separate products developed in the same process become individually identifiable. | |

| _____ 13. | m. A costing approach that considers all indirect manufacturing costs (both variable and fixed) to be product (inventoriable) costs. | |

| _____ 14. | n. Purchasing products or services from a supplier outside the company. | |

| _____ 15. | o. Capital budgeting models that focus on cash inflows and ouflows while taking into account the time value of money | |

| _____ 16. | p. Calculation of a selling price sufficient to cover the cost of producing a product as well as desired operating income | |

| _____ 17 | q. The long-term planning for investment commitments with returns spread over multiple years | |

| _____ 18. | r. A decision process that compares the differential revenues and costs of alternatives. | |

| _____ 19. | s. Costs that will continue even if a company discontinues one of its current operations | |

| _____ 20. | t. The increase in expected average annual operating income divided by the original required investment | |