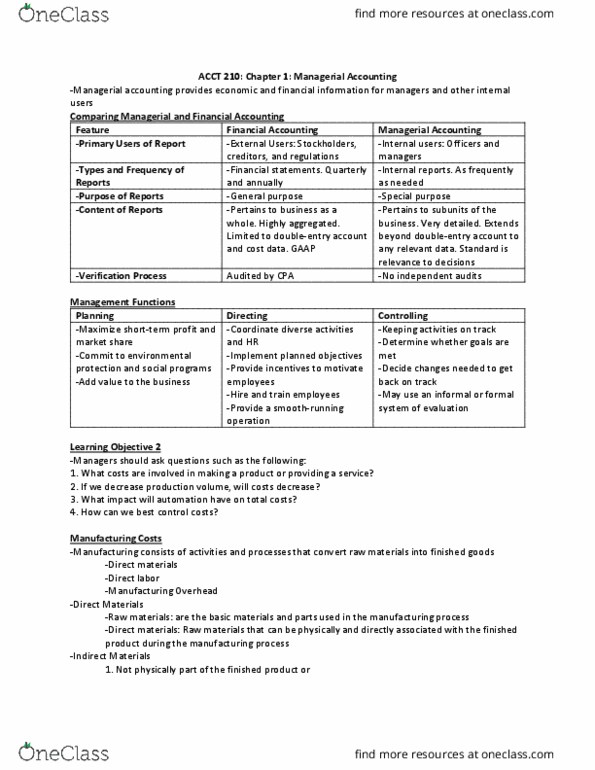

ACCT 210 Study Guide - Quiz Guide: Direct Labor Cost, Indian Railways, Interest Expense

Document Summary

Get access

Related Documents

Related Questions

Cook Farm Supply Company manufactures and sells a pesticidecalled Snare. The following data are available for preparingbudgets for Snare for the first 2 quarters of 2017.

| 1. | Sales: quarter 1, 29,400 bags; quarter 2, 42,500 bags. Sellingprice is $63 per bag. | |

| 2. | Direct materials: each bag of Snare requires 4 pounds of Gummat a cost of $3.8 per pound and 6 pounds of Tarr at $1.75 perpound. | |

| 3. | Desired inventory levels: |

Type of Inventory

January 1

April 1

July 1

Snare (bags)8,10012,20018,100Gumm (pounds)9,50010,10013,200Tarr(pounds)14,20020,50025,400

| 4. | Direct labor: direct labor time is 15 minutes per bag at anhourly rate of $14 per hour. | |

| 5. | Selling and administrative expenses are expected to be 15% ofsales plus $179,000 per quarter. | |

| 6. | Interest expense is $100,000. | |

| 7. | Income taxes are expected to be 30% of income before incometaxes. |

Your assistant has prepared two budgets: (1) the manufacturingoverhead budget shows expected costs to be 125% of direct laborcost, and (2) the direct materials budget for Tarr shows the costof Tarr purchases to be $301,000 in quarter 1 and $426,500 inquarter 2.

a) Prepare the budgeted multiple-step income statement for thefirst 6 months.

***Please answer question 14. Thank you.

Your company produces a basic potato chip. There are three mainprocesses used in the chips. The first process washes and peels thepotatoes. The second process slices and fries the potatoes. Thethird process seasons and packages the chips. The potato chips aresold in 12 oz bags (1 bag is a unit)

Information on the direct materials is listed in table 1.Consider this information the standard.

Direct labor information given in Table 2. Consider thisinformation the standard.

Annual overhead information is given in Table 3. Overhead isallocated based direct labor hours. Estimated annual direct laborhours are 12,500. Calculate a predetermined OH rate (round to twodecimal places if needed). Use this rate when you need to applyOH.

Table 4 gives you the information for the last two months on theoverhead cost. Use this information to determine the fixed andvariable portions of the cost. (You will need this information tocomplete Table 5). Machine hours have been determined as the bestcost driver for separating mixed cost into their fixed and variableportions. It takes approximately 12 minutes of total machine timefor each bag of chips (or 1/5 a machine hour per bag of chips).

Table 5 is where you will list all your production cost,separated into their fixed and variable components.

Cost-Volume-Profit (CVP) Relationships

Selling Price: You sell a bag of chips for $5.14

Breakeven point: Calculate the breakeven point. Be sure toinclude the fixed component of mixed cost in your fixed costs andthe variable component in the variable cost.Show your breakeven in Sales units and in Sales Dollars

Profit Planning: Determine the number of units you must sell tomake an annual pre-tax profit using 3 assumptions concerning yournet income (profit), both in sales units and sales dollars.

Aggressive Profit ($100,000)

Conservative Profit ($25,000)

Average Profit ($60,425)

Budgeting:

Create a sales budget using the information for earning anaverage profit for the year. You will break the budget down intothe four quarters for the year. (Sales tend to be consistent eachquarter, you can only sale a whole unit so round-up if necessary)Use table 6 to complete the sales budget.

Create a production budget for each quarter of the year (keep itin quarters; you do not need to break it down by month). You desireto keep 10% of next quarterâs sales in ending inventory. Sales forQtr 1 the following year are expected to be 30,000 bags of chips.There is not any beginning finished goods inventory for quarterone. Use table 7 to complete the production budget.

Running quarter one -- Weighted-average process costing. Table 8presents the information for the packaging department. Complete thequestions under table 8.

Actuals are in for quarter one. You sold 25% more units than youbudgeted for, but price per unit was only $5.00.

Calculate revenue

Compute the cost of goods sold (total and per unit) beforeadjusting for actual OH cost

Actual potato usage for quarter one was 69,500 pounds at a priceof $0.54 per pound. Actual equivalent units of production (bags ofchips) completed through the first process (where the potatoes areadded) was 29,520. Calculate the direct materials variances for thepotatoes (price, usage, and total) and indicate if these variancesare favorable or unfavorable.

Actual direct labor hours for the quarter were 5,120 at anaverage rate of $12.05 per hour. For actual production you expectedto use 4,800 direct labor hours. Calculate the direct laborvariances (rate, efficiency and total) and indicate if thesevariances are favorable or unfavorable.

For next quarter you have been asked to supply a special orderof you potato chips. The non-profit organization requesting thisorder would like a special bag that will cost $0.28 instead of thenormal $0.25 per bag. The request is for 10,000 bags of chips.Based on your projections you have the capacity for this order.What is the minimum price per unit and total price you would bewilling to accept on this order? (You cannot afford to take thisoffer at a loss, but you are fine with accepting it at cost).

***14) Determine over- or under-applied overhead and close tocost of goods sold. Actual OH cost are given in table 14 (look at#12 for actual DL hours used to apply OH). Determine the new costof goods sold amount.

Table 1: Direct Materials

Material | Quantity per unit | Cost | Total per unit |

potatoes | 1.5 lbs | $0.60 | $0.90 |

seasoning | 1 ounce | 0.05 | 0.05 |

packaging | 1 bag | 0.25 | 0.25 |

1/12 box | 0.6 | 0.05 | |

Total cost | $1.25 |

Table 2: Direct Labor

Job description | Hours per bag | Rate | Total cost |

Potato washer & peeler | 0.1 | $11.50 | $1.15 |

Slicer & Fryer | 0.04 | 11.50 | 0.46 |

Packager | 0.06 | 11.50 | 0.69 |

Total cost | $2.30 |

Table 3: YEARLY OVERHEAD COSTS

Cost description | Amount |

Indirect material | $6,500 |

Indirect labor | 61,450 |

Machine Maintenance | 4,120 |

Electricity | 3,570 |

Depreciation | 6,340 |

Quality testing | 10,520 |

Total | 92,500 |

Predetermined OH rate:

Table 4 â Actual Overhead cost for the last two months

Month 1 | Month 2 | |

Indirect Material (F) | $530 | $530 |

Indirect Labor (F) | 5,250 | 5,250 |

Machine Maintenance | 370 | 445 |

Electricity | 180 | 225 |

Depreciation (F) | 625 | 625 |

Quality testing | 510 | 600 |

Machine Hours * | 1,200 | 1,500 |

*12 minutes of machine time per bag of chips (1/5 hour = 1unit)

Complete any calculations here:

Table 5: Variable and Fixed Costs

COSTS Description VARIABLE Cost perunit FIXED Cost perYear

TOTAL |

If a cost is mixed, put the fixed amount in the fixed column andthe variable amount in the variable column.

CVP Calculations:

Table 6 â Sales Budget

Qtr 1 | Qtr 2 | Qtr 3 | Qtr 4 | Total | |

Table 7 â Production Budget

Qtr 1 | Qtr 2 | Qtr 3 | Qtr 4 | |

Process Costing â Packaging Department

Direct materials are added 70% at the beginning of the processand the remaining 30% are added when the chips are 50% completewith the packaging process. Direct labor and overhead are addedevenly throughout the process.

Table 8 â Unit and cost information

Cost | |||||

Physical Units | Transferred-in | Direct Materials | Direct Labor | Overhead | |

Beg WIP | 1,000 (40% complete) | $6,500 | $112.40 | $1,948.85 | $1,788.35 |

Transferred In | 30,000 | $63,250 | |||

End WIP | 2,200 (30% complete) | ||||

Added during Qtr 1:

Direct Materials -- $5045.40

Direct Labor â 1,580 hrs @ $12.05 per hour

Overhead â OH is applied based on predetermined OH rate andactual DL hours

1. Determine the number of unitscompleted during quarter 1.

2. Compute the equivalent units usingthe weighted average method

3. Compute the cost per equivalentunit using the weighted average method

4. Compute the cost of goodstransferred to finished goods inventory

5. Compute the ending balance in WIP,Packaging

Table 10 â Actual Results (calculaterevenue and COGS)

Units sold | Sales Price | Revenue |

Units sold | Cost per unit | COGS |

Table 11 â DM Variances (potatoesonly)

Price Variance | |

Usage Variance | |

Total Variance |

Calculations:

Table 12 â Direct Labor Variances

Rate Variance | |

Efficiency Variance | |

Total Variance |

Calculations:

#13 Calculations (Minimum price onspecial order)

Table 14 â Actual OH cost for Quarter1

Description | Cost |

Indirect Materials | $2,190 |

Indirect Labor | $18,250 |

Machine Maintenance | $1,825 |

Electricity | $1,720 |

Depreciation | $1,585 |

Quality Testing | $5,940 |

Amount of applied OH:

Amount of actual OH:

Under or Over- Applied Amount:

New COGS amount: