MGMT 30B Study Guide - Quiz Guide: Accounts Receivable, Contribution Margin, Total Absorption Costing

8 Jun 2016

School

Department

Course

Professor

Document Summary

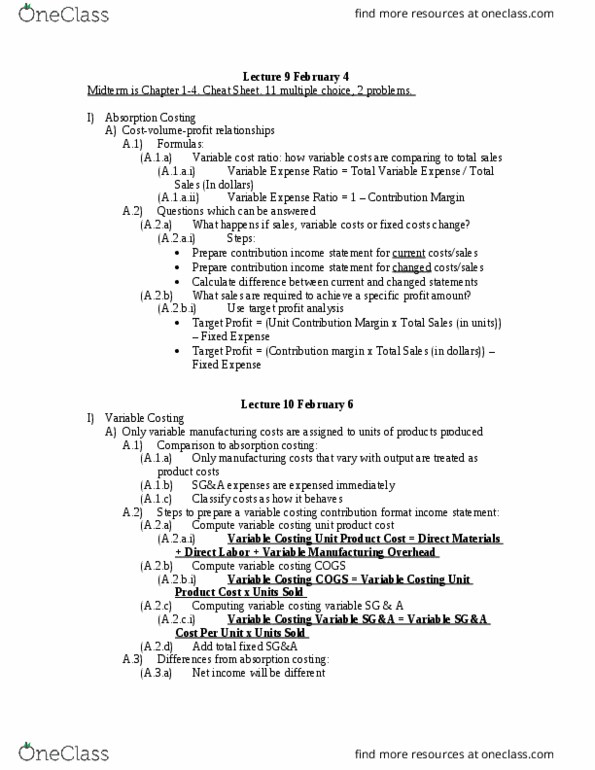

Unit contribution margin = sales price per unit - variable expenses per unit. Helps manager determine if the product is covering its own manufacturing costs. Expenses (ii) break even point = fixed expenses / unit contribution margin (iii) Helps figure out how many units of product we need to sell to cover our costs. Prepare contribution income statement for current costs/sales. Prepare contribution income statement for changed costs/sales. Calculate difference between current and changed statements (b) what sales are required to achieve a specific profit amount? (i) use target profit analysis. Target profit = (unit contribution margin x total sales (in units)) fixed expense. Target profit = (contribution margin x total sales (in dollars)) fixed expense. People down below have a better idea of the numbers: developing a planning budget, components: (a) sales budget: budgeted unit sales x unit sales price (b) prepare schedule of cash collections (i) steps: