ACCT 305 Study Guide - Final Guide: Finance Lease, Effective Interest Rate, Interest Expense

Document Summary

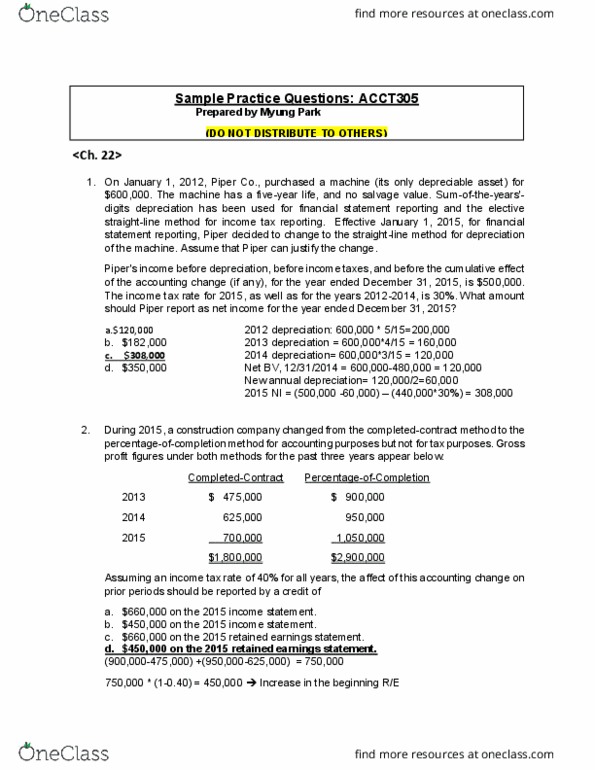

Sample practice questions: acct305 (do not distribute to others) Use the following information for questions 1 and 2. On january 1, 2018, ogleby corporation signed a five-year noncancelable lease for equipment. The terms of the lease called for ogleby to make annual payments of ,000 at the beginning of each year for five years with title passing to ogleby at the end of this period. The equipment has an estimated useful life of 7 years and no salvage value. Ogleby uses the straight-line method of depreciation for all of its fixed assets. Ogleby accordingly accounts for this lease transaction as a finance lease. The present value of annual lease payments was ,578 at an effective interest rate of 10%. On january 1, 2020, ogleby should record: rent expense of ,000, interest expense of sh and lease liability of ,578, interest expense of ,764 and lease liability of ,400. interest expense of ,058 and lease liability of ,636.