HUMS 202 Study Guide - Quiz Guide: Debit Card, Savings Account, Financial Institution

26 Apr 2018

School

Department

Course

Professor

● “Pay Yourself First”: when you get a paycheck, tax refund, cash gift, or other money,

you should put some of that money in a savings account before you pay your bills

○ Save money toward goals you have identified

○ Improve your standard of living

○ Learn to manage money better

○ Have money for emergencies

○ Major expenses people save for:

■ Costly/unplanned expenses: car repair, medical bills

■ loss/reduction in income

■ Down payment for house, car, or other large purchase

■ Education

■ Retirement

■ Vacation

● Saving Tips:

○ Differentiate between spending for needs and wants

■ Cut back on unnecessary spending

○ Pay bills on time to avoid late fees

○ Shop around, including for financial services

○ Monitor your bank account to avoid fees

■ Keep track; don’t forget to record debit card purchases

○ Have part of your paycheck direct-deposited into a savings account or ask your

bank how to establish auto-transfer savings

○ Keep making monthly payments to yourself once you have completed payment

on a loan

○ Save at least part of any cash gift, bonus, or raise

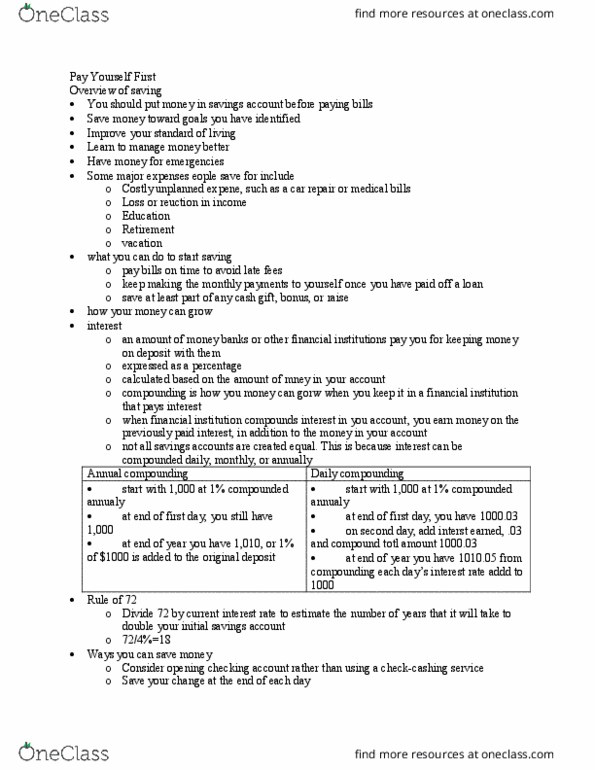

● How your money can grow:

○ Interest:

■ An amount of money banks or other financial institutions pay you for

keeping money on deposit with them

■ Expressed as a percentage

■ Calculated based on the amount of money in your account

○ Compounding: how your money can grow when you keep it in a financial

institution that pays interest

■ Earn money on previously paid interest, in addition to money in your

account

■ Can be compounded daily, monthly, or annually

■ The more frequently interest compounds, the faster it grows

○ Rule of 72: a formula that lets you estimate how long it will take for your savings

to double in value (assuming interest rate remains the same over time)

■ Divide 72 by the current interest rate to estimate the number of years that

it will take to double your initial savings amount

● Ex. if you invest $50 in a savings account at a 4% interest rate, it

will take about 18 years for your initial savings to double

○ 72/4 = 18 years

find more resources at oneclass.com

find more resources at oneclass.com

● Savings Options:

○ Bank Deposit accounts:

■ Insured by the FDIC

■ Make money by earning interest

■ Easy and quick access to your funds

■ Savings Products:

● Savings Account: an easy and safe place to save money

● Certificate of Deposit (CD): you agree to keep the money in an

account for a set term-- a few weeks or several years. Bank

agrees to pay higher interest rate than you would receive from

checking or savings account

○ If you need money earlier, it can be arranged but you may

be penalized with an early withdrawal fee

● Money Market Deposit Account: like a basic savings account,

but often required to keep a higher balance in order to earn a

higher rate of interest

○ Non-deposit investment accounts:

■ Not federally insured

■ Investment: long-term savings option that you purchase for future income

of financial benefit

■ Greater risk of loss (might lose entire amount)

■ Opportunity to earn more money

● Good tool to grow money for long-term

■ Protect your money from inflation: $10 buys more today than it will in ten

years because prices might rise

■ Types of investment products:

● U.S. Treasury Securities (offered by federal government)

○ I Savings Bonds: purchased at face value (amt. Printed

on bond); interest is composed of a fixed rate plus an

inflation rate-- added to bond monthly and paid when bond

is cashed

○ EE Savings Bonds: purchased at ½ face value (unless

bought online for face value); earn fixed rate of interest

that is set

○ ******* SAVINGS BONDS must be held for one year

before they can be cashed; if you redeem a bond

before it is 5 yrs old, you will lose three months of

accrued interest

○ Treasury Bills (T-Bills): sold at a discount from face value

and range days-year; difference between purchase price

and face value is interest

○ Treasury Notes (T-Notes): pay interest every six months

find more resources at oneclass.com

find more resources at oneclass.com

Document Summary

Pay yourself first : when you get a paycheck, tax refund, cash gift, or other money, you should put some of that money in a savings account before you pay your bills. Save money toward goals you have identified. Major expenses people save for: loss/reduction in income. Down payment for house, car, or other large purchase. Differentiate between spending for needs and wants. Pay bills on time to avoid late fees. Monitor your bank account to avoid fees. Keep track; don"t forget to record debit card purchases. Have part of your paycheck direct-deposited into a savings account or ask your bank how to establish auto-transfer savings. Keep making monthly payments to yourself once you have completed payment on a loan. Save at least part of any cash gift, bonus, or raise. An amount of money banks or other financial institutions pay you for keeping money on deposit with them. Calculated based on the amount of money in your account.