SOC 3714 Study Guide - Midterm Guide: Individual Retirement Account, Household Debt, Collegehumor

19 May 2018

School

Department

Course

Professor

ECONOMICS OF AGING

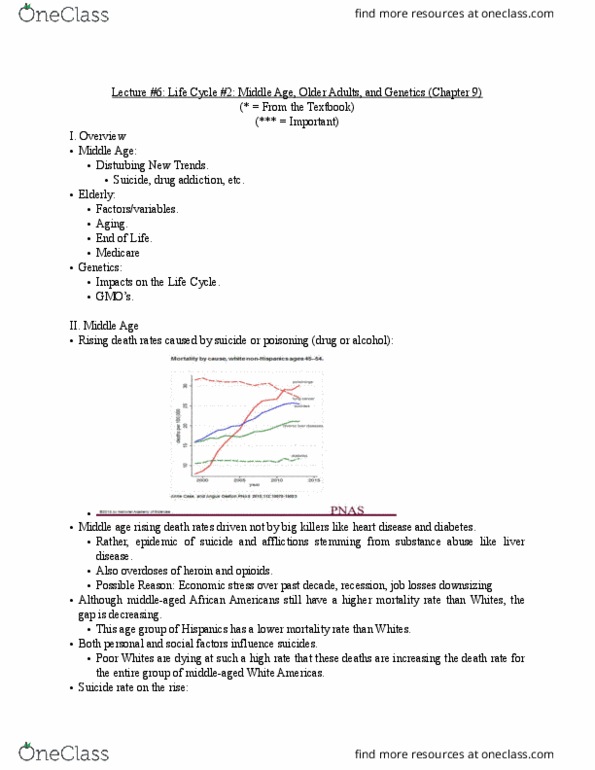

ECONOMIC CRISIS ON 2008

Average family’s net worth:

•2007 $126,400•2010 $77,300

•Most of the loss is due to housing prices

Median family income:

•2007 $49,600•2010 $45,800

•Have long-term repercussions across the life course

•Could lead to lower retirement savings and less wealth to draw upon during retirement

60 YEARS AGO

•Elderly least privileged group in the United States

•Older people had lower incomes than younger people and were more at risk of being poor.

•Since 1960s, large improvement in economic position of aged•By 2014, lowest poverty rates of any

age group:

•9% for aged 65 and above; 14% for aged 18 – 64; 22% for children

AGED TODAY

Each year since 1970, those turning 65 have had:

•Higher levels of education

•More stable job histories

•Higher preretirement incomes

They have benefited from:

•A lifetime of improving opportunities

•Stable family life

•Upward mobility

•Increases in Social Security benefits

●Benefited from rising prosperity after WWII

•From 1945-1974, average standard of living improved substantially for all, even those with little edu

•Median increases

•From 1949-1959 42%

•From 1959-1969 38%

•Fewer people in economy so jobs were plentiful.

REASONS WHY THE AGED OF THE FUTURE MAY HAVE LESS ECONOMIC SECURITY

1.Fewer people are saving for retirement

2.Increase in average household debt

3.Fewer people have adequate retirement savings due to the decline in housing prices.

4.Barely half of 30-year-olds earn more than their parents. In 1970s, nearly all adult children outpaced

their parents.

STUDENT DEBT

•Overall student loan debt

•2003 $.2 trillion

•2015 $1.2 trillion

•Accounts for one-third of all non-mortgage household debt and is now greater than credit card debt

•Average recent college graduate leaves school owing $31,000 with some owing more, especially if

they obtain an advanced degree

find more resources at oneclass.com

find more resources at oneclass.com

•Who has student loans? 55% of individuals aged 21-29 ; 40% of individuals aged 31-39

Reasons for increase in student debt

•Tuition increases

•More people going to college

•Many parents have taken on college loans so student loan debt can burden whole family

Long-term consequences

•Harder to purchase home since cannot make down payment or bank rejects loans

•Decline in home ownership decreases income security in old age

•If buy home when older, may be less likely to pay off mortgage before retiring

•May make it harder to contribute to IRA or 401K

SOCIAL SECURITY

•By 2033, revenue coming into the trust fund for Social Security will fall below the level of benefits

being paid out.

•Income at that point will only pay about 75% of benefits.

•Why?

•Aging of Baby Boomers

•Population growth slowed after 1960 as fertility declined

•People living longer in old age

•Number of workers for every single retiree:5 in 1960; 2.2 in 2025

RAISE RETIREMENT AGE

•1935 eligible age was 65

•1956 women allowed to retire at age 62 with a 20% cut in benefits

•1962 men allowed to retire at age 62 with a 20% cut in benefits

•1972 increased benefits for people who claim benefits beyond full retirement age for each year until

age 70

•1983 raised full retirement age from 65 to 67 and increased the penalty for early retirement from 20%

to 30%

Rationale for increasing age

•Average life expectancy has increased.

•Older people today are more affluent, healthier, and better educated than their counterparts

in 1935.

Problems

•Lower money for those who lose jobs or income in early 60s

•May make job market more competitive by reducing retirements

•Could increase racial-ethnic inequalities; racial-ethnic minorities are more likely to retire

earlier, mainly due to poorer health

REDUCING BENEFITS

•Lengthening years of work needed for full benefits OR

•Decreasing what wealthier people receive OR

•Reduce cost-of-living increase so benefits remain the same but do not keep up with inflation

INCREASING REVENUES

•Increase present pay roll tax

•Currently workers contribute 6.2% and employers 6.2%

•Increase by 1% over 20 years

find more resources at oneclass.com

find more resources at oneclass.com

•Would have little burden on individuals if done gradually; adds 5¢ more per week for those who earn

$50,000

•Popular solution supported by 83%

•Equally popular option is to eliminate the tax cap on earnings•In 2016, must pay payroll taxes on first

$118,500 and then nothing after that

MEANS TESTING

•Eliminate benefits for retirees with high incomes

•One proposal: $110,000 single person; $165,000 couple

•Problems:

•Concern would discourage savings

•People who saved would be penalized over people who spent their earnings during their

working years, since they would receive no Social Security benefits once they retired.

•Also would encourage fraud with people trying to hide their income and/or savings

•Majority regardless of political party oppose it

PRIVATIZATION

•Make people more responsible for retirement income and the government less responsible

•One plan would place Social Security benefits entirely into private individual savings accounts

•The biggest problem would be that there is more risk to savings for several reasons:

•People may be more likely to withdraw it and spend it.

•People may not be savvy in investing their funds or make risky investments.

•People may be more likely to lose it with economic downturns in the stock market.

DEFINED BENEFIT PLAN (These are typically called “pensions.”)

• pay monthly benefits at retirement and amount is based on years of service and prior earnings

•Companies have become reluctant to establish new defined benefit plans.

•From 1990 to 2008, the percent of workplaces offering these plans declined from 35% to 20%.

PROBLEMS

•Access: not available in many jobs

•Vesting rules: length of time workers must be employed to be eligible; those who lost jobs or

took other jobs lost their pensions

•No cost-of-living increases so pension value declines with years

•Insufficient funds to cover promised benefit

DEFINED CONTRIBUTION PLANS

•A savings plan with some tax advantages

•Worker & employer or worker alone pays a fixed amount into account that is invested for the worker.

•Most common is 401K plan.

•Benefits based upon contributions and results of investments•Have become much more common in

recent years due to a shift in responsibilities from employers to workers

PROBLEMS

•Workers may withdraw funds.

•Participation is voluntary. Only about half of eligible workers choose to participate, and many

wait until older to contribute.

•Vulnerable to big fluctuations in the stock market

•Some workers are encouraged or required to put all or some of their contributions into

company stock.

find more resources at oneclass.com

find more resources at oneclass.com

Document Summary

Average family"s net worth: 2007 ,400 2010 ,300, most of the loss is due to housing prices. Median family income: 2007 ,600 2010 ,800, have long-term repercussions across the life course, could lead to lower retirement savings and less wealth to draw upon during retirement. Each year since 1970, those turning 65 have had: higher levels of education, more stable job histories, higher preretirement incomes. They have benefited from: a lifetime of improving opportunities, stable family life, upward mobility, increases in social security benefits. Benefited from rising prosperity after wwii: from 1945-1974, average standard of living improved substantially for all, even those with little edu, median increases, from 1949-1959 42, from 1959-1969 38, fewer people in economy so jobs were plentiful. Reasons why the aged of the future may have less economic security. 3. fewer people have adequate retirement savings due to the decline in housing prices. 4. barely half of 30-year-olds earn more than their parents.