BUAD 203 Study Guide - Final Guide: Debenture, Preferred Stock, Financial Instrument

26 Apr 2017

School

Department

Course

Professor

Document Summary

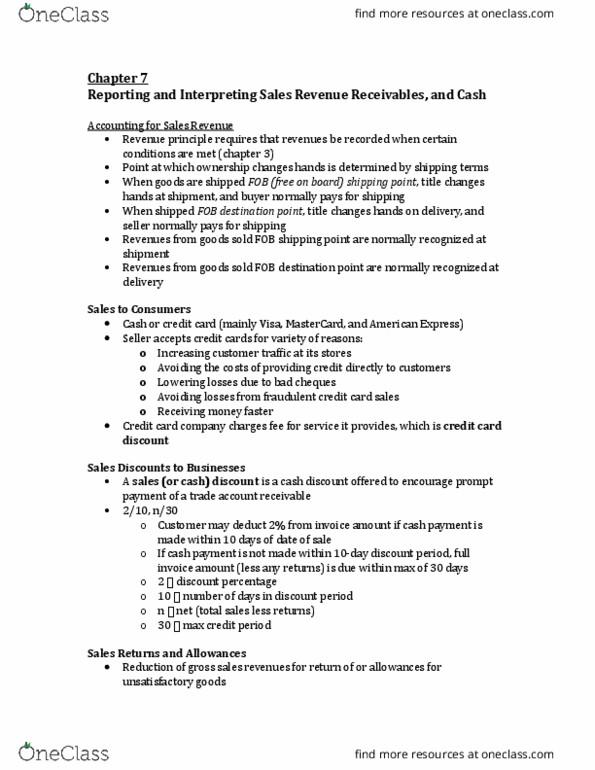

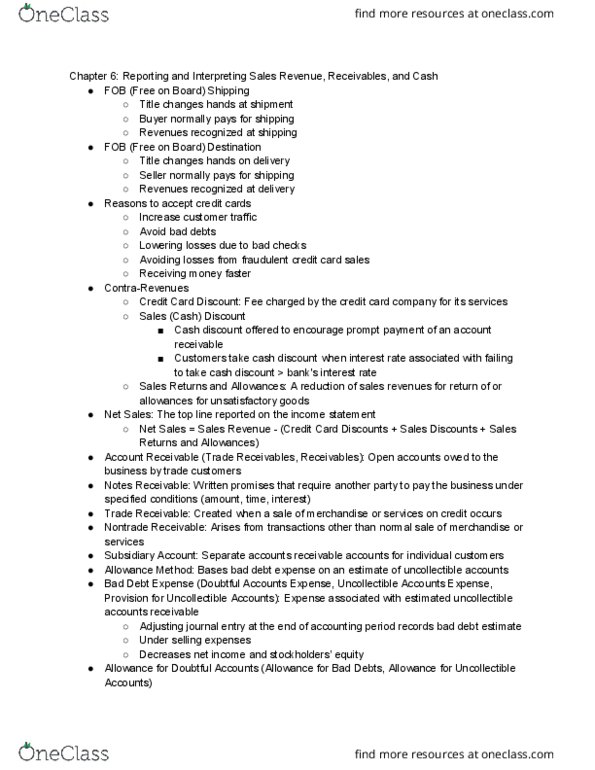

Principles of accounting study guide (only on modules 2-4) General concepts: accounting measurements tend to be based on historical cost determined by reference to an exchange transaction with another party. Revenues: inflows and enhancements from delivery of goods and services that constitute central ongoing operations. Gains/losses: like revenues/expenses, but from peripheral transactions or events. Periodicity assumption: is made that business activity can be divided into measurement intervals (months, quarters, years). Fiscal years attempt to follow natural business year cycles. Accrual-basis accounting: accrue means to come about as a natural growth or increase. Revenue recognition: normally occurs at the time services are rendered or when goods are sold and delivered. Reflective of measuring revenues as earned and expenses as incurred: an exchange transaction, the earnings process being complete. 2: determine the transaction price, allocate the transaction price to the performance obligations in the contract, recognize revenue when (or as) the entity satisfies a performance obligation.