Accounting ACCT 2620 Study Guide - Quiz Guide: Direct Labor Cost, Cost Driver, Batch Production

Heidi Nassos

Quiz 1 Review

Ch. 2, 3, 7

Term

Definition

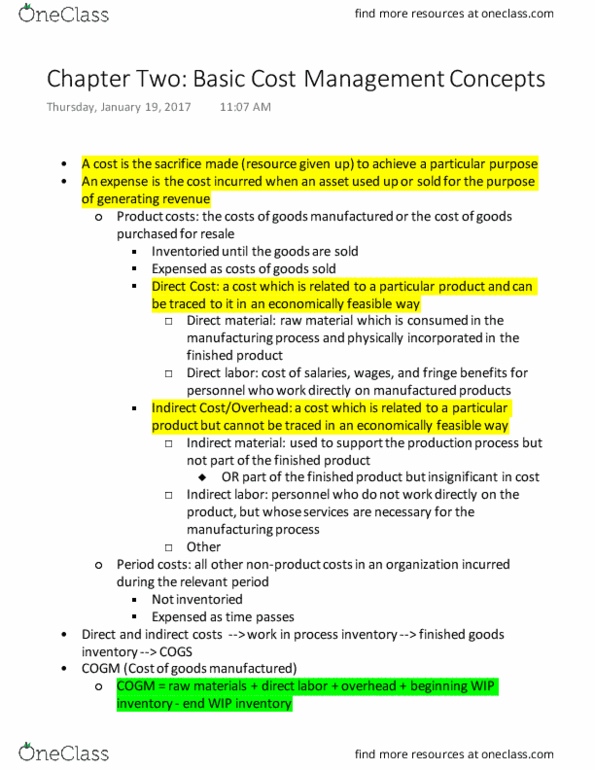

Cost

Sacrifice made, usually measured by the resources given up, to achieve a particular purpose

Expense

Cost incurred when an asset is used up or sold for the purpose of generating revenue; recognition of a cost on the financial

statement once good/service is provided

Product Cost

Cost assigned to goods that were either purchased or manufactured for resale

Cost of Goods Sold

Product costs recognized as an expense

Inventoriable Cost

Product cost is stored as the cost of inventory until the goods are sold

Period Costs

All costs that are not product costs; identified with period of time in which they are incurred rather than with units of

purchased/produced goods (ex. R&D, SG&A)

Operating Expenses

Treated as period costs and expensed during the period in which they are incurred (ex. Employee wages, fuel, machine

maintenance)

Raw-material Inventory

All materials before they are placed into production

Work-in-process Inventory

Manufactured products that are only partially completed at the date when the balance sheet is prepared

Finished Goods

Manufactured goods that are complete and ready for sale

Direct Material

Raw material that is consumed in the manufacturing process, is physically incorporated in the finished product, and can be traced to

products relatively easily

Direct Labor

Cost of salaries, wages, and fringe benefits for personnel who work directly on the manufactured products

Manufacturing Overhead

All other costs of manufacturing, including indirect material, indirect labor, and other manufacturing costs

Indirect Material

Cost of materials required for production process but do not become an integral part of the finished product (ex. Glue, paint, drill

bits)

Indirect Labor

Costs of personnel who do not work directly on the product, but whose services are necessary for the manufacturing process

Other Manufacturing Costs

Depreciation, property taxes, insurance, utilities, service departments, overtime premiums, idle time

Cost of Goods

Manufactured

Total cost of direct material, direct labor, and manufacturing overhead transferred from work-in-process inventory to finished-

goods inventory

Activity

Measure of the organization's output of products or services

Cost Driver

Characteristic of an activity or event that causes costs to be incurred by that activity or event (ex. Machine hours, # pieces

inspected, purchase orders)

Variable Costs

Changes in total in direct proportion to a change in the level of activity

Fixed Costs

Remains unchanged in total as the level of activity (or cost driver) varies

Cost Object

Entity, such as a particular product, service, or department, to which a cost is assigned

Direct Cost

A cost that can be traced to a particular cost object

Indirect Cost

Cost that is not directly traceable to a particular cost object

Opportunity Cost

Benefit that is sacrificed when the choice of one action precludes taking an alternative course of action

Sunk Cost

Costs that have been incurred in the past. Do not affect future costs and cannot be changed by any current or future action

Differential Cost

Amount by which the cost differs under two alternative actions

Incremental Cost

Increase in cost from one alternative to another

Marginal Cost

Extra cost incurred when one additional unit is produced (because efficiency of production changes with output)

Average Cost

Total cost / number of units produced

find more resources at oneclass.com

find more resources at oneclass.com

Document Summary

Sacrifice made, usually measured by the resources given up, to achieve a particular purpose. Cost incurred when an asset is used up or sold for the purpose of generating revenue; recognition of a cost on the financial statement once good/service is provided. Cost assigned to goods that were either purchased or manufactured for resale. Product cost is stored as the cost of inventory until the goods are sold. All costs that are not product costs; identified with period of time in which they are incurred rather than with units of purchased/produced goods (ex. Treated as period costs and expensed during the period in which they are incurred (ex. All materials before they are placed into production. Work-in-process inventory manufactured products that are only partially completed at the date when the balance sheet is prepared. Manufactured goods that are complete and ready for sale.