ACCT10002 Chapter Notes - Chapter 7: Cash Register, Bank Reconciliation, Cheque

22 May 2018

School

Department

Course

Professor

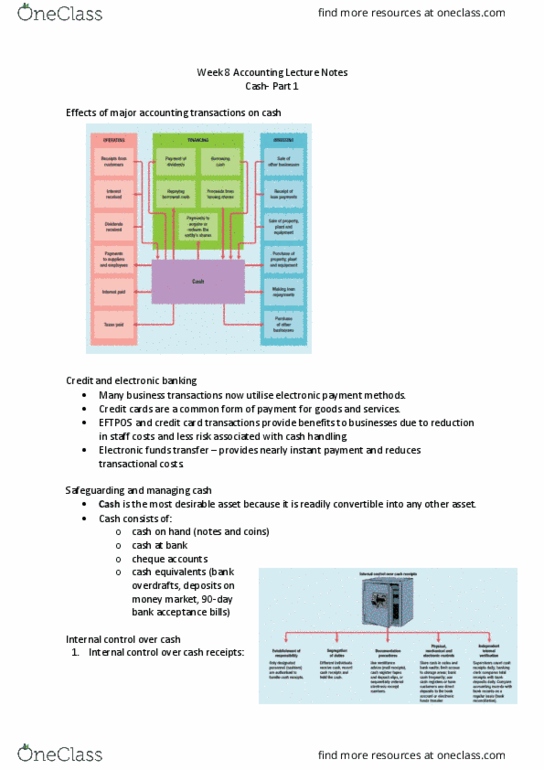

Cash on hand (coin and paper money)

-

Cash at bank (cheque account)

-

Cash equivalents (highly liquid investments such as bank overdrafts, deposits on the money

market and 90

-

day bank acceptance bills)

-

Duplicates of credit card and electronic funds transfer at point of sale (EFTPOS) sales

-

Cash includes:

Revenue from cash sales of goods and services

-

Collection of cash from credit sales

-

Cash proceeds from divestment of assets

-

Cash received from business owners through issuance of shares

-

Cash received from borrowings

-

Transactions with inflows of cash include:

Cash payment for purchases of inventory

-

Cash payment for investment in assets such as PPE

-

Cash payment for business expenses such as payroll and rent

-

Payment to business owners in the form of dividend or return of capital

-

Interest and loan payment to financial institution

-

Transactions that cause outflows of cash include:

Cash and credit transactions

Saturday, 26 August 2017 3:13 PM

IFA Page 1

Saving in staffing cost as there is less handling of cash required

-

Reduces the possibility of mishandling cash

-

For business owners, accepting payments electronically has several benefits:

Electronic banking speeds up the transfer of money and reduces the transactional cost (less

documentation of writing cheques and deposit slips and less labour is required)

Credit and electronic banking

Saturday, 26 August 2017 3:14 PM

IFA Page 2

Cash is readily convertible into any other type of asset, easily concealed and transported, and highly

desired

Numerous errors may occur in executing and recording cash transactions so it is essential to have an

effective mechanism in place to safeguard cash assets

Eg. performing a bank reconciliation regularly

Internal control over cash receipts:

Cash received from cash sales, on EFTPOS or on credit cards should be rung up on a cash register

located in a position that permits the customer to see the amount recorded

1.

The register prints a receipt that is given to the customer

2.

Registers are usually linked directly to computers used by the accounting department or have a

locked

-

in tape on which each cash sale is recorded

3.

The cash in the register plus EFTPOS and credit card slips are counted and recorded on a

preprinted form that is sent to the accounting department

4.

The cash and slips are forwarded to the cashier for deposit and the tape is sent to the accounting

department for preparing accounting entries

5.

Procedures for the control of cash receipts from cash sales are based on the principle of segregation of

duties for record keeping and custodianship

The employee who opens the mail should prepare a list of the amounts received

1.

One copy is sent to the cashier along with the cash amounts, which are combined with those from

the cash registers

2.

Another copy of the list is forwarded to the accounting departments for preparing entries in the

cash receipts journal and in customers' accounts

3.

Procedures for the control of cash received in the mail are based on the principle of segregation of

duties for record keeping and custodianship

Neither the cash register, the mail clerk nor the cashier should have access to the accounting records

Likewise, the accounting staff should not have access to cash

Internal control over cash payments:

Pay for cash purchases

-

Pay suppliers for goods and services bought on credit

-

Pay for expenses and liabilities

-

Purchase assets

-

Cash is disbursed for a variety of reasons

Internal control over cash payments is more effect when payments are made by using a bank account

Staff designated to approve invoices for payments should have no responsibility for preparing cheques

or other payment instruments

Employees responsible for signing cheques or approving EFTs should have no invoice approval or

accounting responsibilities

Approved invoices, copies of the cheques and approved electronic transfers are send to the accounting

department

Petty cash fund:

A petty cash fund is a cash fund used to pay relatively small amounts

Often used to handle small payments (postage fees, employees' working lunches, taxi fares) while

maintaining satisfactory control

Safeguarding and managing cash

Saturday, 26 August 2017 3:14 PM

IFA Page 3

Document Summary

Cash equivalents (highly liquid investments such as bank overdrafts, deposits on the money market and 90-day bank acceptance bills) Duplicates of credit card and electronic funds transfer at point of sale (eftpos) sales. Revenue from cash sales of goods and services. Cash received from business owners through issuance of shares. Cash payment for investment in assets such as ppe. Cash payment for business expenses such as payroll and rent. Payment to business owners in the form of dividend or return of capital. Saving in staffing cost as there is less handling of cash required. For business owners, accepting payments electronically has several benefits: Electronic banking speeds up the transfer of money and reduces the transactional cost (less documentation of writing cheques and deposit slips and less labour is required) Cash is readily convertible into any other type of asset, easily concealed and transported, and highly desired.