ACCT1501 Chapter Notes - Chapter 5: Accrual, Cash Flow, Accounts Receivable

12 Nov 2020

School

Department

Course

Professor

Document Summary

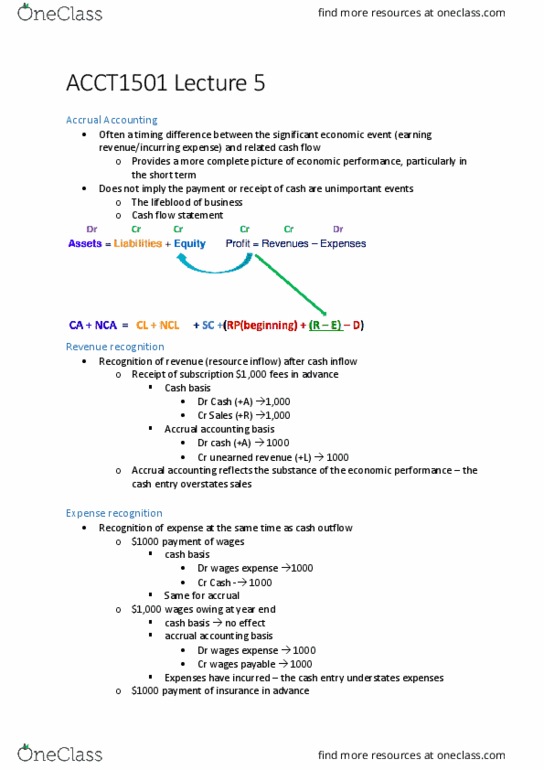

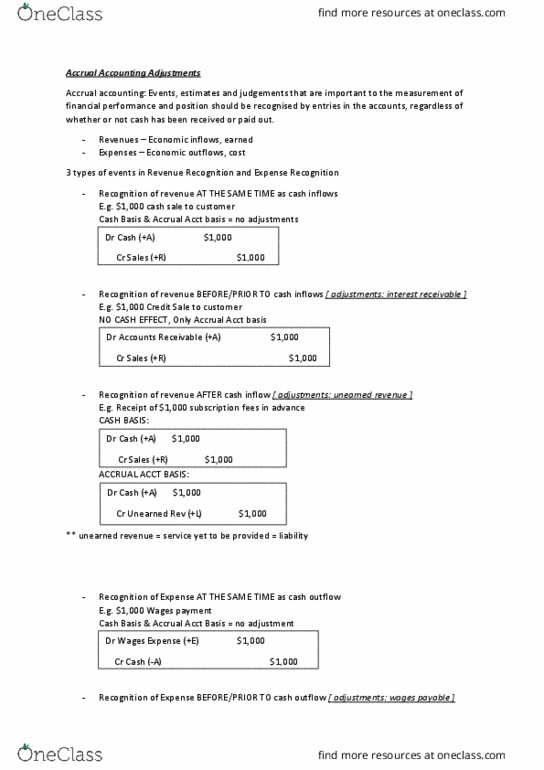

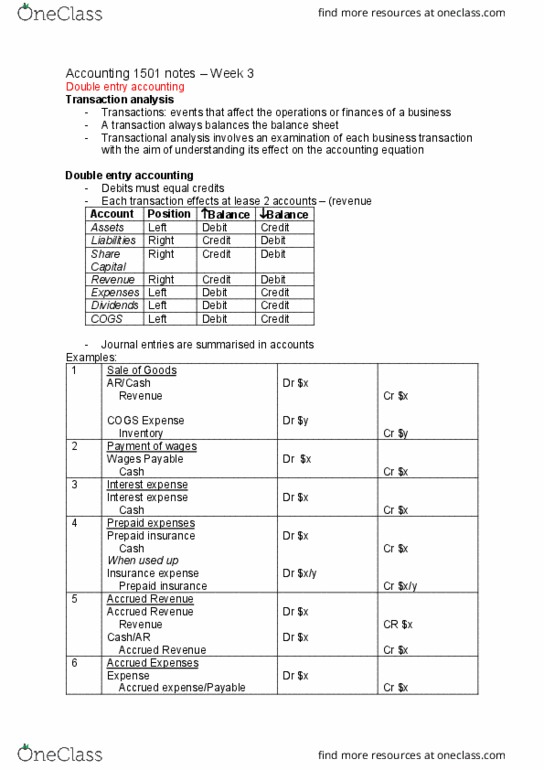

This article is a topic within the subject accounting 1a. Trotman, k. & gibbins, m. , 2009 financial accounting: an integrated approach, 4th edition, melbourne: In accrual accounting (different to cash accounting), events, estimates and judgements are crucial to the measurement of financial position and financial performance. A downside of this is that accrual accounting can be manipulated. Revenues and expenses can be recognised: before cash changes hand (credit sale) at the same time as cash changes hand (cash sale) or, after cash changes hand (unearned revenues or prepayments) When a company pays expenses in advance of recognising the expense it is known as an "expiration of asset" adjustment. Initially the firm will debit a prepaid insurance account (increase it), and credit cash. After each month, the firm will debit insurance expense (1/12th of the total cash paid) and credit prepaid insurance (as it must be decreased as the benefits are used up)