ACCT2331 Chapter Notes - Chapter 12: Withholding Tax

Document Summary

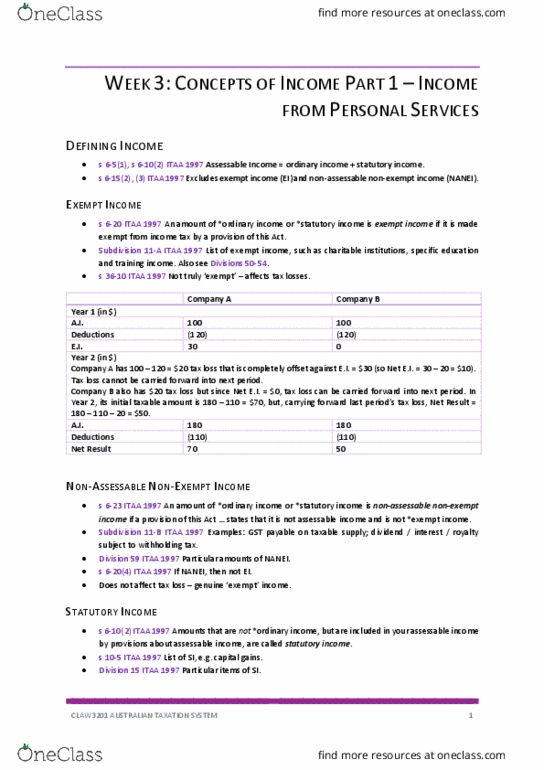

Chapter 12 exempt income and non-assessable non exempt. 12. 1 introduction [p319: tax exemptions are used by government to indirectly support the bodies they wish. Important to determine whether amounts are exempt income or non- assessable non-exempt income because: Both are not included in assessable income (hence not taxed) [s6-15. Losses/outgoings incurred to gain/produce both incomes are generally not deductible [s8-1(2) itaa97] Only exempt income is taken into account in working out the amount of a tax loss [36-10 itaa97] 12. 2 exempt income: ordinary or statutory income is exempt income if it is made exempt by a provision in the itaa36 or itaa97 or another commonwealth law, checklist in subdiv 11-a itaa97. Income of certain kinds of entities (p320 for corresponding legislation section) Sports, musical and art societies and clubs: many of these entities are also required to satisfy special condition in. Second class of exempt income: certain kinds of income. Non-cash business benefits that do not exceed .