ECON 1B03 Chapter 3: Demand, Supply, and Equilibrium

10 Dec 2018

School

Department

Course

Professor

46

ECON 1B03 Full Course Notes

Verified Note

46 documents

Document Summary

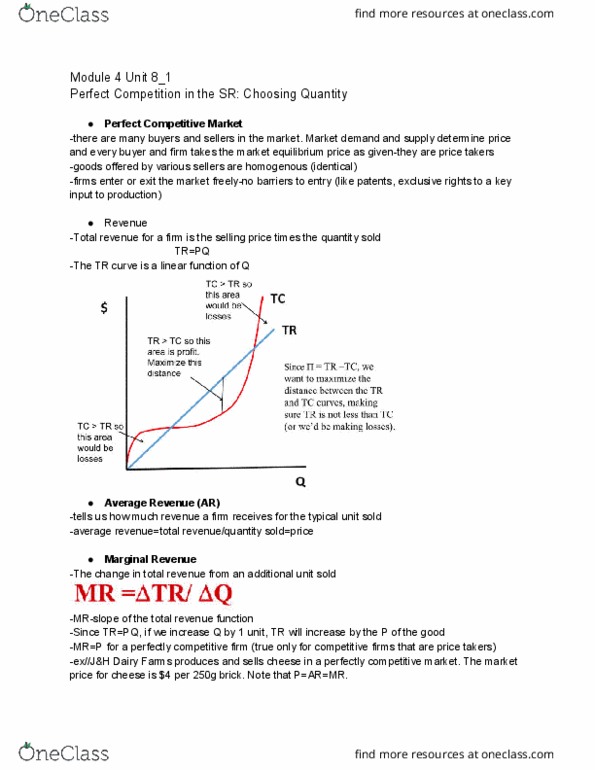

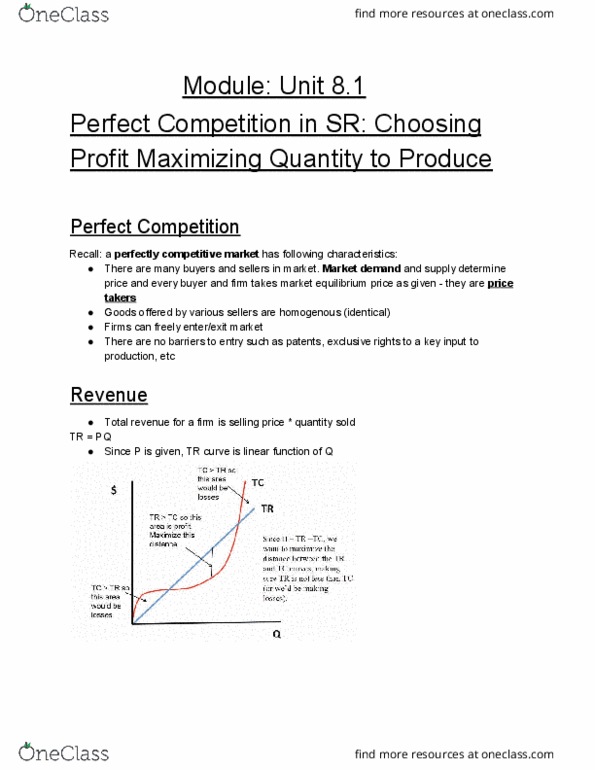

Recall a market: a group of buyers and sellers of a good or service. And nothing can force firms to stay in an industry as resources are perfectly mobile. Since there are so many buyers/sellers, no single individual or firm can influence the market. So no one can affect the price at which a good sells. In perfect competition, consumers/firms are price takers: buyers know the price they have to pay and sellers know what price they"ll get. Market price: when market demand meets up with market supply, a price will be established that makes buyers/sellers the best off they can be. Quantity demanded (qd): the amount of a good consumers (buyers) are willing to buy at every given price, p. Law of demand: as p increases, qd will decrease. Sam would buy chocolate for 3, and carly would buy it for 2. Say that there are 2 buyers in the market for candy bars.