COMM 103 Chapter Notes - Chapter 12: Marketing Effectiveness, Price Skimming, Fixed Cost

26 Aug 2013

School

Department

Course

Professor

Document Summary

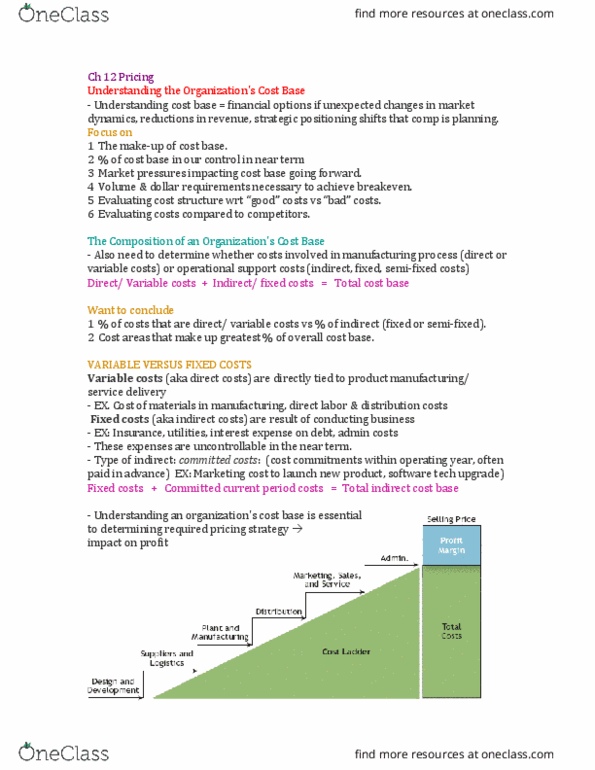

Managers must understand the configuration of the cost base of the org for which they are developing strategies, making decisions, and determining how the firm will compete. Key element of process is to identify the costs which will be faced, the percentage impact which key costs areas have on total cost base & degree of control managers have on costs. With a good understanding of the cost base, managers will better assess their financial options in the event of unexpected changes in market dynamics, unanticipated reductions in revenue, and strategic positioning shifts which the organization is planning. An org"s cost base is made up of the total costs associated with delivering the org"s products and/or services to the marketplace. Also have to determine whether these costs are directly involved with the manufacturing process (direct/variable) or whether the costs are operational support costs (indirect/fixed: direct/variable costs + indirect/fixed costs = an org"s total cost base.