AFM101 Chapter Notes - Chapter 8: Write-Off, High Tech, Perpetual Inventory

30 Dec 2016

School

Department

Course

Professor

30

AFM101 Full Course Notes

Verified Note

30 documents

Document Summary

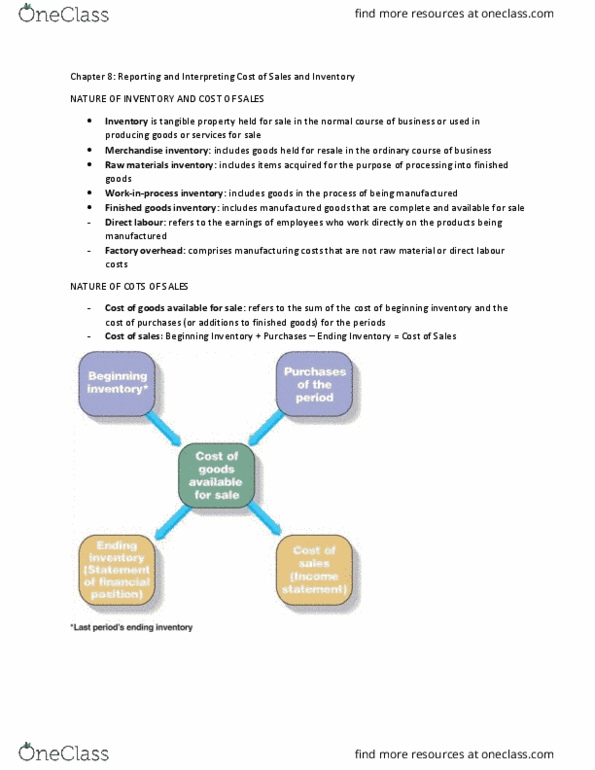

Chapter 8: reporting & interpreting cost of sales and inventory. Inventory a tangible property held for sale in the normal course of business or used in producing goods/services for sale current asset. Merchandise inventory goods held for resale in the normal course of business held by merchandisers. Manufacturing businesses hold the following types of inventory: raw materials inventory items acquired purchase, growth, or extraction for processing into finished goods. Goods in inventory are recorded in conformity with the cost principle. Cash-equivalent inventory cost includes the sum of the applicable expenditures and charges directly or indirectly incurred in bringing an article to a usable or saleable condition and location. Accumulating purchases costs should stop either when the raw materials are ready for use or when merchandise inventory is ready for shipment to customers. Direct labour cost that represents the earnings of employees who work directly on the products being manufactured this doesn"t apply to a factory supervisor.