AFM101 Chapter Notes - Chapter 4: Book Value, Debits And Credits, Deferral

7 Jun 2018

School

Department

Course

Professor

Adjusting Entries that Increase Expenses:

• Deferred Expenses: previously recorded assets (ex. Prepaid rent, supplies, equipment) that

were created when cash was paid in advance and must be reduced to the actual amount of

expense incurred

o Ex. Supplies, prepayments (e.g. rent, insurance), buildings and equipment

o During the period:

▪ Prepaid Insurance (+A)

Cash (-A)

o End of period:

▪ Insurance expense (+E, -SE)

Prepaid Insurance (-A)

• Accrued Expenses: expense that have been incurred but not yet recorded because cash will be

paid after the g or s are used

o Interest payable, wages payable, property taxes payable

o End of period:

▪ Wages Expense (+E, -SE)

Wages Payable (+L)

o Next period:

▪ Wages Payable (-L)

Cash (-A)

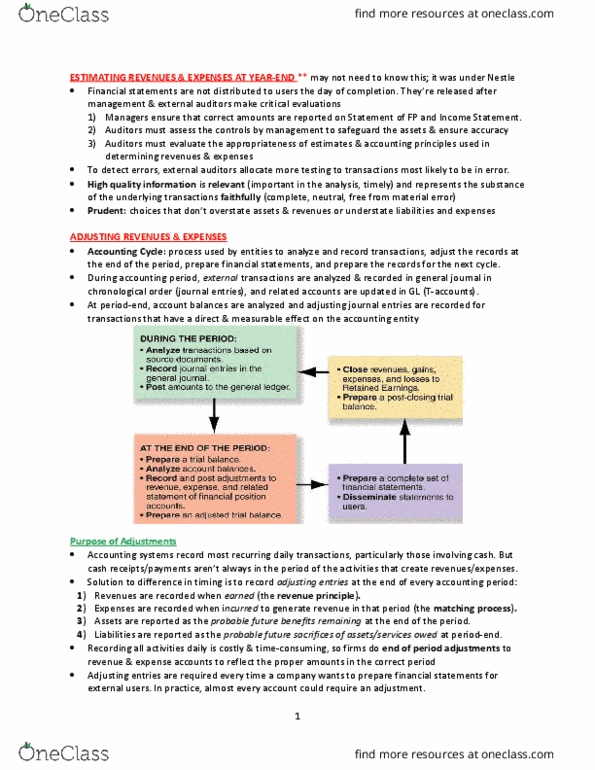

Adjustment Process

• Three steps to analyzing adjustments at the end of period:

o 1) Ask: Was revenue earned or an expense incurred that has not yet been recorded?

o 2) Ask: Was the related cash received or paid in the past or will it be received or paid in

the future?

o 3) Compute the amount of revenue earned or expense incurred, and record the

adjusting entry

Unadjusted Trial Balance

• Trial balance = a list of all accounts with their balances that provides a check on the equality of

the debits and credits

o *See pg. 169 to see an example*

Deferred Revenues

• Deferred Service Revenue – Ex. Sun-Rype provided additional services in January for $10 to new

clients that had previously paid initial fees to Sun-Rype

o Was revenue earned that is not yet recorded? YES

o Was the related cash received in the past or will it be received in the future? Sun-Rype

received cash in the past and recorded it in the deferred service revenue liability

account. This account must be reduced by $10 at January 31, because Sun-Rype

performed the services during the current period

find more resources at oneclass.com

find more resources at oneclass.com

30

AFM101 Full Course Notes

Verified Note

30 documents

Document Summary

Adjusting entries that increase expenses: deferred expenses: previously recorded assets (ex. Prepaid rent, supplies, equipment) that were created when cash was paid in advance and must be reduced to the actual amount of expense incurred: ex. Supplies, prepayments (e. g. rent, insurance), buildings and equipment: during the period, prepaid insurance (+a) Prepaid insurance (-a: accrued expenses: expense that have been incurred but not yet recorded because cash will be paid after the g or s are used. Interest payable, wages payable, property taxes payable: end of period, wages expense (+e, -se) Wages payable (+l: next period, wages payable (-l) Unadjusted trial balance: trial balance = a list of all accounts with their balances that provides a check on the equality of the debits and credits, *see pg. Deferred revenues: deferred service revenue ex. Sun-rype received cash in the past and recorded it in the deferred service revenue liability account.