AFM101 Chapter Notes - Chapter 4: General Ledger, Trial Balance, Retained Earnings

7 Jun 2018

School

Department

Course

Professor

AFM 101 - Chapter 4 Notes

ADJUSTING REVENUES AND EXPENSES

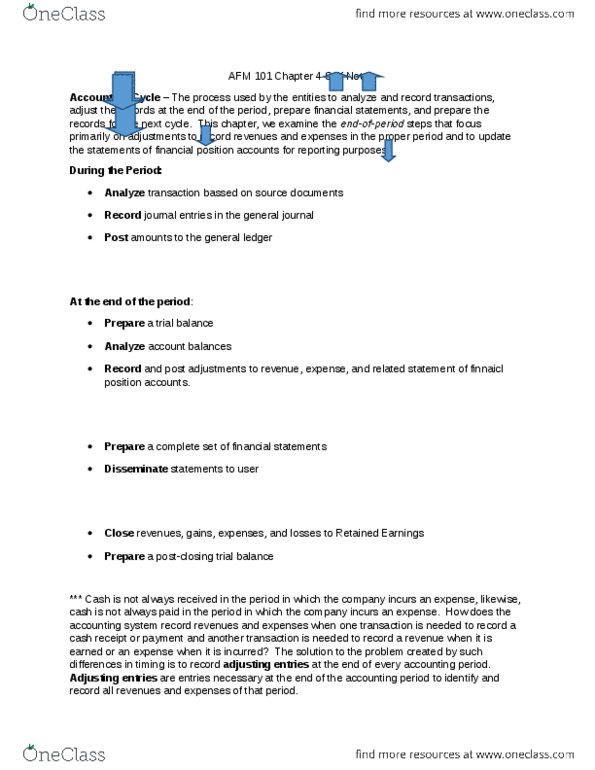

Accounting Cycle

• = the process used by entities to analyze and record transactions, adjust the records at the end

of the period, prepare financial statements, and prepare the records for the next cycle

• During the period: analyze transactions, record journal entries in the general ledger, post

amounts to the general ledger;

Purpose of Adjustments

• Adjusting entries = entries necessary at the end of the accounting period to identify and record

all revenues (revenue principle) and expenses (matching process) of that period

• Companies wait until the end of the accounting period to adjust their accounts because

adjusting it daily would be very costly and time-consuming

• Adjusting journal entries involves one account on the statement of financial position and one

account on the statement of earnings

• Cash is never adjusted

Types of Adjustments

• There are 4 types of adjustments (2 in which cash was already received or paid and 2 which cash

WILL be received or paid). Each of these adjustments involve two entries:

o One entry to record the cash receipt or payment during the period

o One entry to record the revenue or expense in the proper period through an adjusting

entry prepared at the end of the period

DURING THE PERIOD:

• Analyze transactions

• Record journal entries in the GL

• Post amounts to the GL

AT THE END OF THE PERIOD:

• Prepare a trial balance

• Analyze account balances

• Record and post adjustments to

revenue, expense, and related

statement of financial position accounts

• Prepare an adjusted trial balance

• Close revenues, gains,

expenses, and losses to

Retained Earnings

• Prepare a post-closing

trial balance

• Prepare a complete set of

financial statements

• Disseminate (spread)

statements to users

find more resources at oneclass.com

find more resources at oneclass.com

30

AFM101 Full Course Notes

Verified Note

30 documents

Document Summary

During the period: analyze transactions, record journal entries in the gl. Post amounts to the gl: close revenues, gains, expenses, and losses to. Retained earnings: prepare a post-closing trial balance. Prepare a trial balance: analyze account balances, record and post adjustments to revenue, expense, and related statement of financial position accounts. Prepare an adjusted trial balance: prepare a complete set of financial statements, disseminate (spread) statements to users. Types of adjustments: there are 4 types of adjustments (2 in which cash was already received or paid and 2 which cash. Adjusting entries that increase revenues: deferred revenues: previously recorded liabilities created when cash was received in advance, must be reduced to the actual amount of revenue earned during the period, ex. Deferred ticket revenue: during the period, cash (+a) Deferred fee revenue (+l: end of period, deferred fee revenue (-l)