AFM101 Chapter Notes - Chapter 13: Inventory Turnover

26 Jun 2018

School

Department

Course

Professor

AFSA Education

10. Receivables Turnover Ratio: short-term liquidity and operating efficiency

= Net Credit Sales / Average Net Trade Receivables

- Collective cash from customers so it does not tie up funds in unproductive assets

- Turnover reflects how many times trade receivables was recorded and collected

- Reflects company granting and collecting activities

- Receivables turnover ratio is often converted to a time basis known as the average age

of trade receivables

Average Age of Receivables = Days in a Year / Receivables Turnover Ratio

11. Inventory Turnover Ratio: measures both liquidity and operating efficiency

= Cost of Sales / Average Inventory

- Reflects relationship between inventory to the volume of sales during the period

- Increase in ratio is usually favourable

- If ratio is too high, indication that sales were lost because items were not in stock

- Vary significantly between industries

- Inventory turnover ratio is often converted to a time basis called average days’ supply in

inventory

- Average day’s supply in inventory = days in a year / inventory turnover ratio

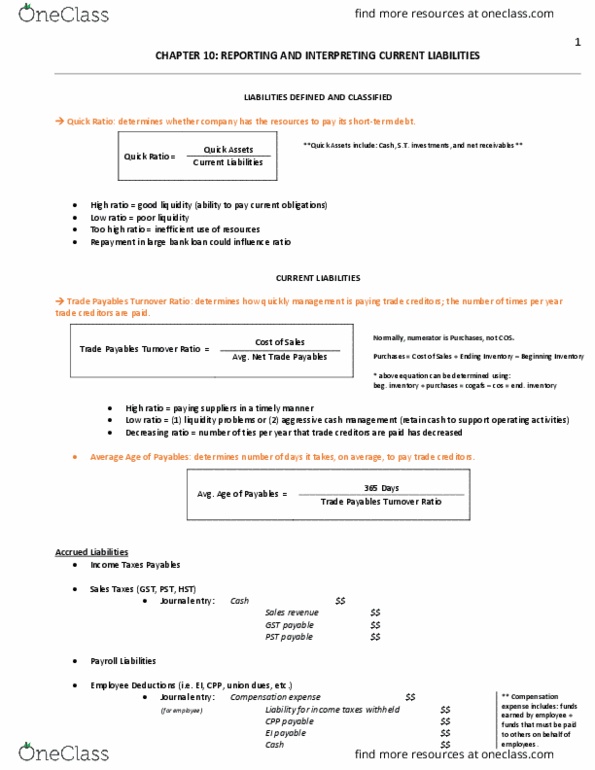

12. Trade Payables Turnover Ratio: evaluates the company’s effectiveness in managing

payables to trade creditors

= Cost of Sales / Average Net Trade Payables

- In reality numerator should be net credit purchases, not cost of sales

- We use cost of sales as approximation, assuming all purchases are made on credit

- Purchases = Cost of Sales + Ending Inventory – Beginning Inventory

- Converted to a time basis known as the average age of payables

- Average Age of Payables = Days in a Year / Trade Payables Turnover Ratio

Using Ratios to Analyze the Operating Cycle

- Operating cycle 3 phases: acquisition of inventory, sale of inventory, collection of cash

from customers

- 3 ratios tot analyze operations: trade payables turnover, inventory turnover, receivables

turnover

- each ratio measures the number of days it takes to complete an operating activity

Tests of Solvency

- tests of solvency: ratios that measure a company’s ability to meet its long-term

obligations

13. Times Interest Earned Ratio: shows if the company is able to pay its interest payments

= (Net Earnings + Interest Expense + Income Tax Expense) / Interest Expense

30

AFM101 Full Course Notes

Verified Note

30 documents

Document Summary

Afsa education: receivables turnover ratio: short-term liquidity and operating efficiency. = net credit sales / average net trade receivables. Collective cash from customers so it does not tie up funds in unproductive assets. Turnover reflects how many times trade receivables was recorded and collected. Receivables turnover ratio is often converted to a time basis known as the average age of trade receivables. Average age of receivables = days in a year / receivables turnover ratio: inventory turnover ratio: measures both liquidity and operating efficiency. Reflects relationship between inventory to the volume of sales during the period. If ratio is too high, indication that sales were lost because items were not in stock. Inventory turnover ratio is often converted to a time basis called average days" supply in inventory. Average day"s supply in inventory = days in a year / inventory turnover ratio: trade payables turnover ratio: evaluates the company"s effectiveness in managing payables to trade creditors.