AFM102 Chapter Notes - Chapter 3: Fixed Cost, Variable Cost, Income Statement

16 Jun 2018

School

Department

Course

Professor

Chapter 3

Cost Structure: The relative proportion of fixed, variable, and mixed costs found

in an organization.

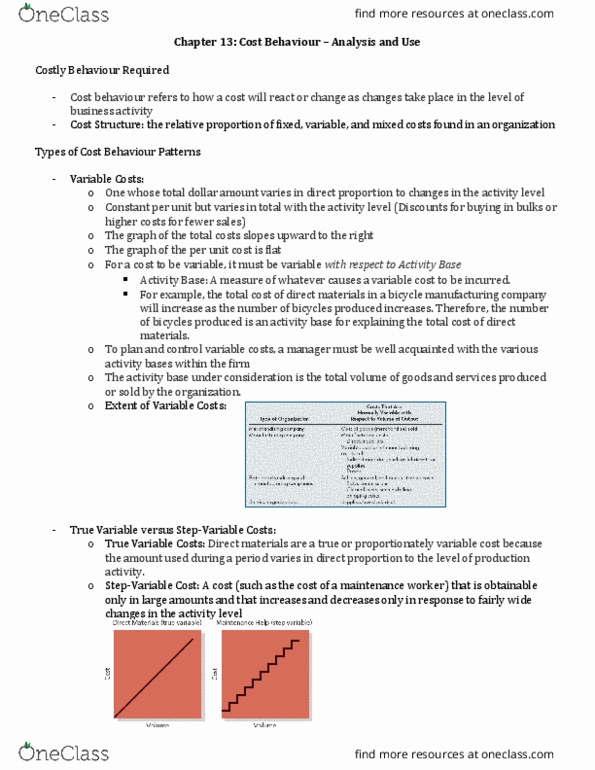

Activity Base: A measure of whatever causes a variable cost to be incurred. For

example, the total cost of direct materials in a bicycle manufacturing company

will increase as the number of bicycles produced increases. Therefore, the

number of bicycles produced is an activity base for explaining the total cost of

direct materials.

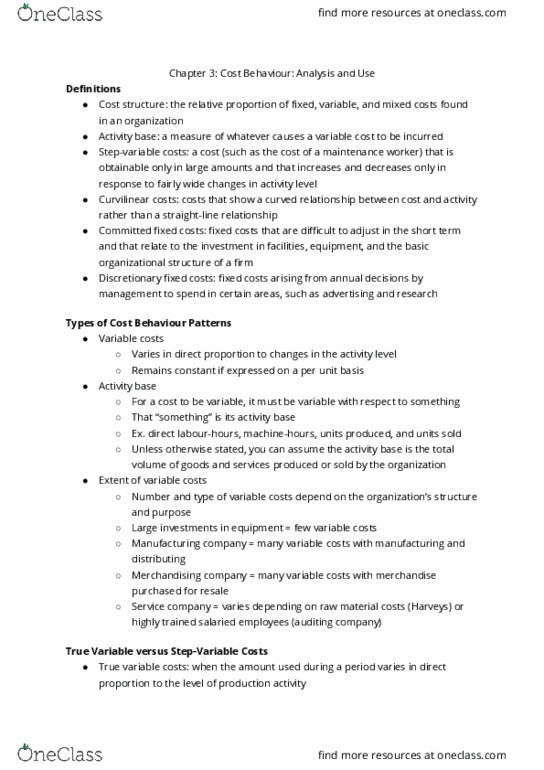

Step-Variable Cost: A cost (such as the cost of a maintenance worker) that is

obtainable only in large amounts and that increases and decreases only in

response to fairly wide changes in the activity level.

Curvilinear Costs: Costs that show a curved relationship between cost and activity

rather than a straight-line relationship.

Committed Fixed Costs: Fixed costs that are difficult to adjust in the short term

and that relate to the investment in facilities, equipment, and the basic

organizational structure of a firm.

Discretionary Fixed Costs: Fixed costs arising from annual decisions by

management to spend in certain areas, such as advertising and research.

Account Analysis: A method for analyzing cost behaviour in which each account

under consideration is classified as either variable or fixed based on the analyst’s

prior knowledge of how the cost in the account behaves.

Engineering Approach: A detailed analysis of cost behaviour based on an

industial enginee’s evaluation of the inputs euied to cay out a paticula

activity and of the prices of those inputs.

find more resources at oneclass.com

find more resources at oneclass.com

Document Summary

Cost structure: the relative proportion of fixed, variable, and mixed costs found in an organization. Activity base: a measure of whatever causes a variable cost to be incurred. For example, the total cost of direct materials in a bicycle manufacturing company will increase as the number of bicycles produced increases. Therefore, the number of bicycles produced is an activity base for explaining the total cost of direct materials. Step-variable cost: a cost (such as the cost of a maintenance worker) that is obtainable only in large amounts and that increases and decreases only in response to fairly wide changes in the activity level. Curvilinear costs: costs that show a curved relationship between cost and activity rather than a straight-line relationship. Committed fixed costs: fixed costs that are difficult to adjust in the short term and that relate to the investment in facilities, equipment, and the basic organizational structure of a firm.