AFM131 Chapter Notes - Chapter 16: International Financial Reporting Standards, Financial Statement, Bookkeeping

14 Jun 2018

School

Department

Course

Professor

Chapter 16:

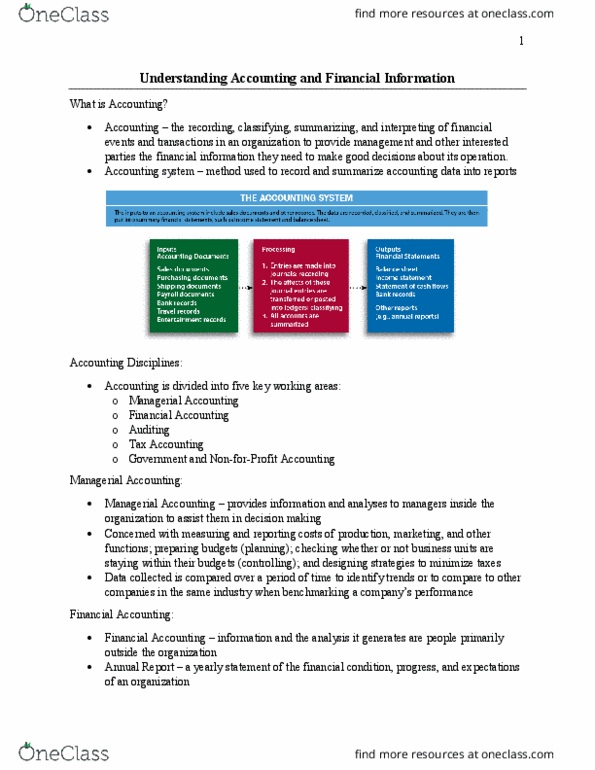

Accounting: The recording, classifying, summarizing, and interpreting of financial

events and transactions in an organization to provide management and other

interested parties the financial information they need to make good decisions.

Five key working areas:

- Managerial Accounting

- Financial Accounting

- Auditing

- Tax Accounting

- Government and not-for-profit accounting

Managerial Accounting: Accounting used to provide information and analyses to

managers inside the organization to assist them in decision making.

Financial Accounting: Accounting information and analyses prepared for people

outside the organization.

Annual Report: A yearly statement of the financial condition, progress, and

expectations of an organization.

Private Accountant: An accountant who works for a single firm, government

agency, or not-for-profit organization.

Public Accountant: An accountant who provides his or her accounting services to

individuals or businesses on a fee basis.

International Financial Reporting Standards (IFRS): The common set of

accounting principles, standards, and procedures that accountants and companies

use to compile financial statements.

find more resources at oneclass.com

find more resources at oneclass.com

Auditing: The job of reviewing and evaluating the records used to prepare a

opa’s fiaial stateets.

Independent Audit: An evaluation and unbiased opinion about the accuracy of a

opa’s fiaial stateets.

Forensic Accounting: A relatively new area of accounting that focuses its

attention on fraudulent activity.

Tax Accountant: An accountant trained in tax law and responsible for preparing

tax returns or developing tax strategies.

Government and not-for-profit accounting: Accounting system for organizations

whose purpose is not generating a profit but rather serving ratepayers, taxpayers,

and others according to a duly approved budget.

Chartered Professional Accountant (CPA) designation: The internationally

recognized Canadian accounting designation.

Accounting Cycle: A six-step procedure that results in the preparation and

analysis of the major financial statements.

Bookkeeping: The recording of business transactions.

Journal: The record book where accounting data are first entered.

Double-entry Bookkeeping: The concept of every business transaction affecting

at least two accounts.

Ledger: A specialized accounting book in which information from accounting

journals is accumulated into accounts and posted so that managers can find all of

the information about a specific account in one place.

find more resources at oneclass.com

find more resources at oneclass.com

22

AFM131 Full Course Notes

Verified Note

22 documents

Document Summary

Accounting: the recording, classifying, summarizing, and interpreting of financial events and transactions in an organization to provide management and other interested parties the financial information they need to make good decisions. Managerial accounting: accounting used to provide information and analyses to managers inside the organization to assist them in decision making. Financial accounting: accounting information and analyses prepared for people outside the organization. Annual report: a yearly statement of the financial condition, progress, and expectations of an organization. Private accountant: an accountant who works for a single firm, government agency, or not-for-profit organization. Public accountant: an accountant who provides his or her accounting services to individuals or businesses on a fee basis. International financial reporting standards (ifrs): the common set of accounting principles, standards, and procedures that accountants and companies use to compile financial statements. Auditing: the job of reviewing and evaluating the records used to prepare a (cid:272)o(cid:373)pa(cid:374)(cid:455)"s fi(cid:374)a(cid:374)(cid:272)ial state(cid:373)e(cid:374)ts.