MGT223H5 Chapter Notes - Chapter 6: Fixed Cost, Variable Cost, Dependent And Independent Variables

Document Summary

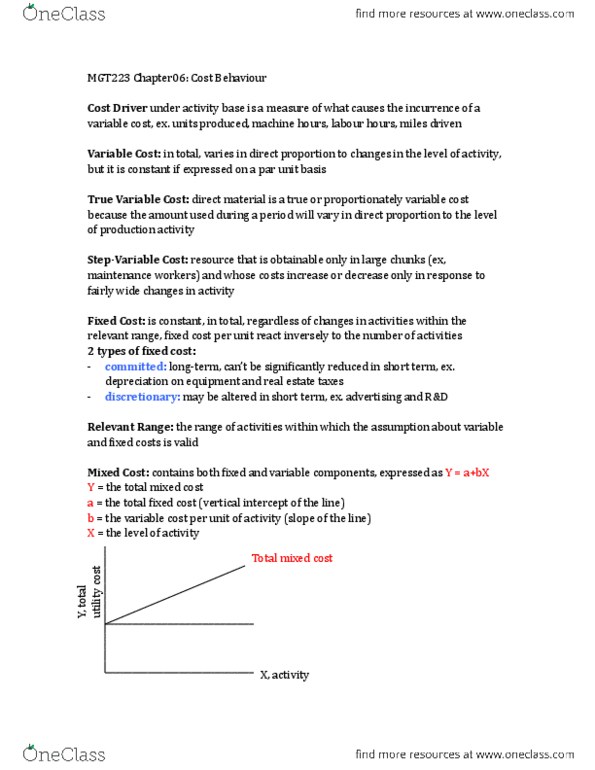

Cost behaviour: how a cost will react/ change as changes take place in level of business activity. Contribution format: which costs are organized by behaviour rather than by traditional functions of production. Cost structure: relative proportion of fixed, and mixed costs found in organization. Variable cost remains constant if expressed on per unit basis varies w/ activity level. Extent of variable costs - # and type of variable costs present in organization will depend in large part on organization"s structure and purpose. True variable costs- dm = true or proportionately variable cost b/c amount used during period will vary in direct proportion to level of production activity. Curvilinear costs: relationship b/w cost and activity that is curve rather than straight line. Relevant range: range of activity within which assumptions made about cost behaviour are valid. Managers should always keep in mind that a particular assumption made about cost behaviour may be invalid if activity falls outside of relevant range.