MGT120H5 Chapter Notes - Chapter 4: Internal Control, Earnings Management, Financial Statement

12

MGT120H5 Full Course Notes

Verified Note

12 documents

Document Summary

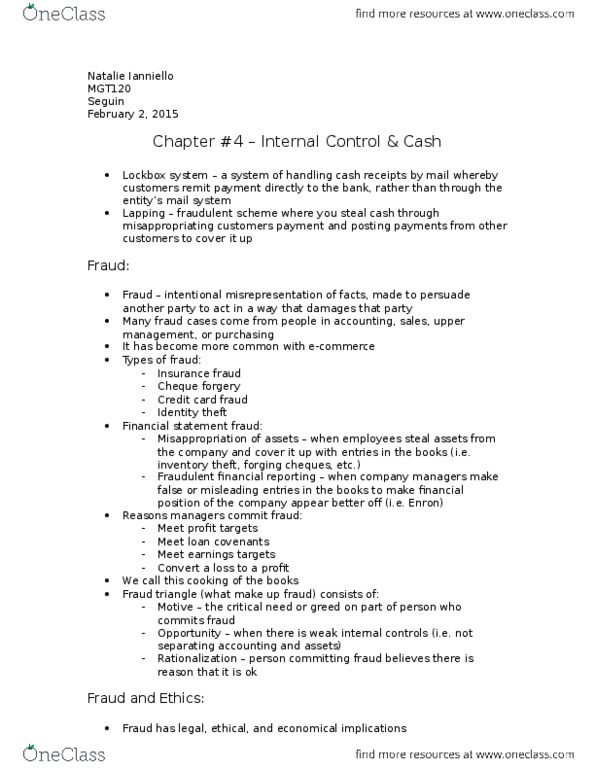

Lockbox system - to receive cheques by mail and then deposited to bank immediately. Fraud is an intentional misrepresentation of facts, made for the purpose of persuading another party to act in a way that causes injury or damage to that party. Types of fraud: misappropriation of assets: this type of fraud is committed by employees of an entity who steal money from the company and cover it up through erroneous entries in the books. Fraudulent financial reporting: committed by company managers who make false and misleading entries in the books, making financial results of the company appear to be better than they actually are. The purpose of this is deceive investors and creditors into investing or loaning money to the company: most common form of fraudulent financial reporting is earnings management. For example, the company"s earnings are . 12 a share, but analysts predicted . 18 a share.