BUS 214 Chapter Notes - Chapter 2: Accounting Equation, Deferral, Accounts Payable

Document Summary

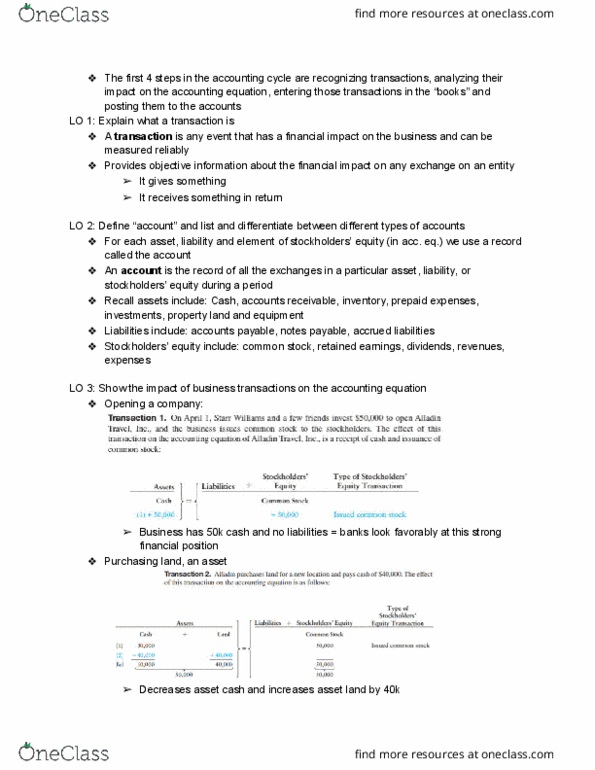

Transaction: any event that has a financial impact on the business and can be measured reliably. Transactions provide objective information about the financial impact of an exchange on an entity: Account: the record of all the changes in a particular asset, liability, or sto(cid:272)kholde(cid:396)s" e(cid:395)uit(cid:455) du(cid:396)i(cid:374)g a pe(cid:396)iod. Cash, accounts receivable (a promise for future collection of cash), inventory, prepaid expenses, investments, property, etc. Accounts payable (promise to pay a debt), notes payable (aka borrowings; notes promising to pay a future amount), accrued liabilities (a liability for an expense you have not yet paid. Co(cid:373)(cid:373)o(cid:374) to(cid:272)k (cid:894)o(cid:449)(cid:374)e(cid:396)s" i(cid:374)(cid:448)est(cid:373)e(cid:374)t i(cid:374) the (cid:272)o(cid:396)po(cid:396)atio(cid:374)(cid:895), retained earnings, dividends, revenues, expenses. E(cid:448)e(cid:396)(cid:455) t(cid:396)a(cid:374)sa(cid:272)tio(cid:374)"s (cid:374)et a(cid:373)ou(cid:374)t o(cid:374) the left side of the a(cid:272)(cid:272)ou(cid:374)ti(cid:374)g equation must equal the net amount on the right side. Every transaction affects the financial statements of the business and financial statements can be prepared after any number of transactions.