MATH 1431 Chapter : 5 1

Document Summary

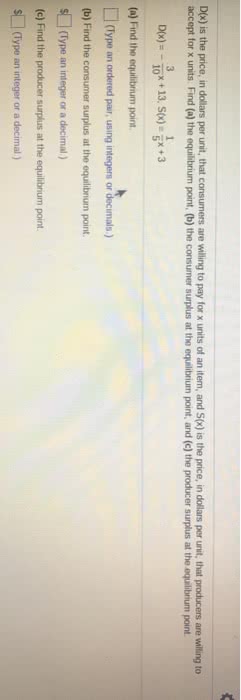

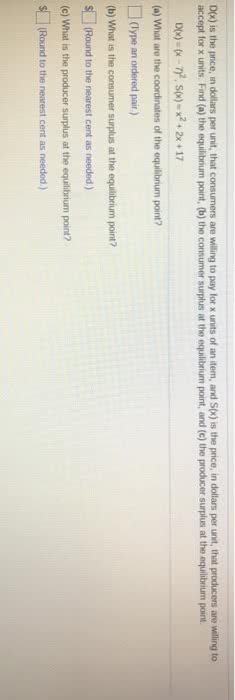

5. 1 an economics application: consumer surplus and producer surplus. Up to this point when we looked at supply and demand curves, we considered the demand and supply curves as functions of the price. Typically, however, in economics, the demand and supply curves are written in terms of the quantity sold. Normally, the demand for an object is higher at lower prices, and the supply of an object increases at higher prices. In a competitive market with elastic pricing, the equilibrium point (or market price) is the intersection of the demand and supply curves. < x < 7 be the price, in dollars per unit, that consumers are willing to pay for x for 0 x. 2 be the price, in dollars per unit, that producers are willing to accept for x units. Utility is defined as the amount of pleasure derived from purchasing x units of a product.