BUS 420 Chapter Notes - Chapter 11: Growth Stock, Tax Rate, Indonesian Rupiah

20 Jul 2020

School

Department

Course

Professor

Document Summary

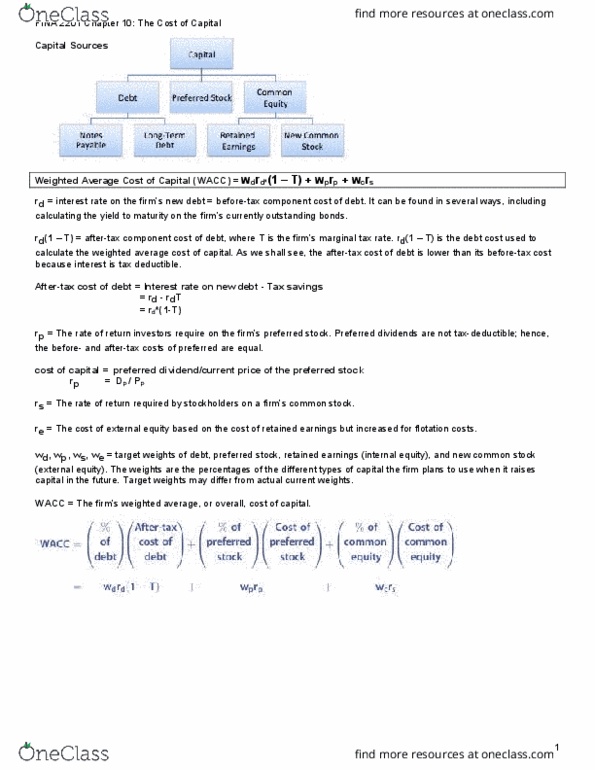

Chapter 11 - determining the cost of capital. Capital components are sources of funding that come from investors. Accounts payable, accruals, and deferred taxes are not sources of funding that come from investors, so they are not included in the calculation of the cost of capital. We do adjust for these items when calculating the cash flows of a project, but not when calculating the cost of capital. Tax effects in the cost of capital. Method 3: yield on the company"s debt. A 15-year, 12% semiannual bond sells for ,153. 72. Interest is tax deductible, so the after tax (at) cost of debt is: rd at = rd bt(1 - t) Rd at = 10%(1 - 0. 40) = 6%. The component cost of debt is the after-tax cost of new debt. It is found by multiplying the interest rate paid on new debt by 1 t, where t is the firm"s marginal tax rate: rd(1-